U.K. Election Is One Pit Stop in Long Brexit Road for Pound, Markets

U.K. Election Is One Pit Stop in Long Brexit Road for Pound, Markets

(Bloomberg) --

Sterling’s rally will be limited even if U.K. Prime Minister Boris Johnson wins a parliamentary majority in the general election and finds a way to pass the withdrawal bill by Jan. 31. That’s because the clock is ticking on a trade agreement in a transition period that runs out at the end of 2020. Any longer-term economic and Brexit uncertainty can increase the chance of a Bank of England rate cut next year, which would weigh on the currency and prop up gilts.

Markets Live strategists and writers explore some of the many potential outcomes of the Dec. 12 vote, and how they would play out for U.K. assets:

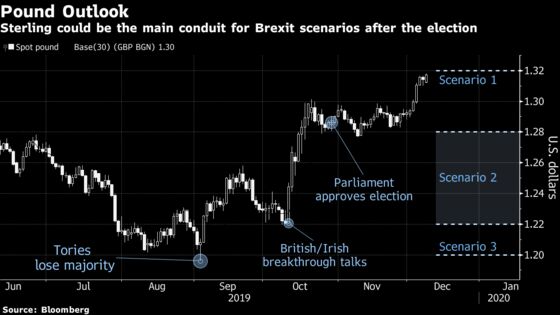

Scenario 1: Conservative Majority

Result: Boris Johnson’s Conservatives get more than 325 seats in Parliament

- Under this base case, cable struggles for further upside beyond 1.32 and EUR/GBP has a tough time making headway down toward the 0.83 handle. Gilts initially sell off, with 10-year fair value about 0.9%

- Short-term sterling gains to sustain declines in the export-heavy FTSE 100, but its trajectory is also determined by U.S.-China trade talks and commodities. Smaller, domestic U.K. companies may be some of the biggest beneficiaries

- But this initial reaction is buffeted by the threat of a no-deal exit amid concerns over reaching a trade agreement next year, especially if the government takes a hard-nosed approach

- Pound options are pricing 1.2815 downside risk, with a 68% certainty factor; this is also likely if the Tories win a wafer-thin majority. Further repricing of Brexit risks would send cable back to the 1.24-1.28 range that prevailed in 2Q/3Q 2019

- Front-end rates will likely keep pricing of 50% odds of a 2020 rate cut. With a cliff-edge Brexit not out of the question and weak economic conditions, the Bank of England stays cautious

Scenario 2: Little Change

Result: Another hung Parliament as Tories fall just short of a majority

- This outcome likely prolongs political and economic uncertainty that has crippled the pound since June 2016 and undermines passage of the withdrawal bill

- Cable quickly falls to the 1.22-1.28 range seen before the withdrawal pact was agreed with the EU. Options suggest cable around 1.25

- Short-end implied yields drop, and a BOE rate cut could easily be priced for as soon as Jan. 30, especially if no U.S.-China phase-one trade deal is passed

- Gilts rally, with the 10- and 30-year segments driving gains and flattening the yield curve. Inflation breakevens rise, with the five-year climbing toward 3%

- Domestic stocks such as banks, homebuilders and real estate take a hit from Brexit uncertainty

Scenario 3: Yes Prime Minister ... Corbyn?

Result: Conservatives win fewer than 300 seats and Labour loses some seats as well. While Labour may be able to form a government with support from other parties, a condition from the coalition could be a prime minister other than Jeremy Corbyn

- Government seeks another Brexit extension to hold a second referendum

- This is the worst-case scenario as investors would demand higher risk premiums for fear that the government will nationalize everything from railroads to utilities and telecoms. Ambitious spending plans roil the pound, spur long-end yields higher and breakeven rates also climb

- Cable tests 2019 lows near 1.22, a figure also supported by options pricing, and 1.20 a worst-case scenario. The wild card is a pound rally on hopes of Brexit being revoked

- Short-end rates mirror the scenario where the Tories couldn’t assure passage of the withdrawal bill. Expect a BOE rate cut to be priced for early 2020

- U.K. utilities and stocks such as Royal Mail are likely to plunge on nationalization concerns

To contact the reporters on this story: Heather Burke in London at hburke2@bloomberg.net;Laura Cooper in London at lcooper59@bloomberg.net;Richard Jones in Berlin at rjones207@bloomberg.net;Ven Ram in London at vram1@bloomberg.net;Eddie van der Walt in London at evanderwalt@bloomberg.net

To contact the editors responsible for this story: Kristine Aquino at kaquino1@bloomberg.net, Heather Burke, Stephen Kirkland

©2019 Bloomberg L.P.