U.K. Taxpayers’ Pandemic-Loan Losses Could Hit 80% in Worst Case

U.K. Taxpayers’ Pandemic-Loan Losses Could Hit 80% in Worst Case

(Bloomberg) -- Amid a punishing recession, defaults and fraud, U.K. taxpayers might face losses of 80% from the coronavirus lending program supporting small business.

In the most detailed assessment to date of Chancellor of the Exchequer Rishi Sunak’s Bounce Back Loan Scheme, the National Audit Office said Wednesday that the worst-case loss estimate had increased from 60%, stoked by the potential for the Covid-19 crisis to last longer and take a greater toll on the economy.

The state watchdog compiled figures from various arms of the U.K. government and assumed smaller businesses will have borrowed about 43 billion pounds ($56 billion) -- the midpoint of a range of estimates -- through the program by its Nov. 30 deadline. An 80% loss, accounting for both defaults and fraud, on those loans -- made overwhelmingly through Britain’s Big Five banks -- would equal 34 billion pounds, or about $44 billion.

The NAO report shows the downside of governments’ attempts to save their economies by getting cash out the door quickly. Sunak introduced Bounce Back, whose loans are fully guaranteed by the state and are intended for small business, after a previous program known as CBILS forced banks to take on 20% of the risk and was criticized for its slow pace.

Estimates remain varied and uncertain, and the NAO’s range shows the steepest potential losses of any assessment so far. Last week’s annual report from the Department for Business, Energy & Industrial Strategy -- which assumed a smaller total outlay of loans -- had calculated that taxpayers could lose as much as 23 billion pounds from various state-backed programs.

The auditing firm PwC has previously warned the risk of fraud from borrowers faking documents and submitting duplicate applications was “very high,” and infiltration by organized crime was also a possibility.

“We targeted this support to help those who need it most as quickly as possible, and we won’t apologize for this,” Sunak’s department said in a statement. “We’ve looked to minimize fraud -- with lenders implementing a range of protections including anti-money laundering and customer checks, as well as transaction monitoring controls. Fraudulent applications can be criminally prosecuted for which penalties include imprisonment or a fine or both.”

The NAO used an estimate from the British Business Bank, which administers the program, and was made Sept. 9, two weeks before Sunak added extra flexibility to the loans, allowing for payment holidays and extending repayments to 10 years from six.

Bounce Back borrowers were subject to less stringent credit checks than banks would impose on those seeking conventional loans. As a result, fraud rates could be “significantly above” above the typical range of 0.5% to 5% for public programs, the NAO said.

The government guarantee “reduces the lenders’ incentives to recover money from borrowers,” the audit office said.

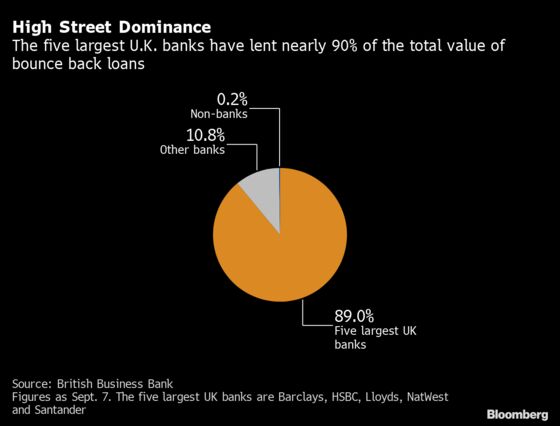

Lloyds Banking Group Plc, HSBC Holdings Plc, Barclays Plc, NatWest Group Plc and the British arm of Banco Santander SA have lent 89% of the value of all loans made under the Bounce Back program. They lent 31.3 billion pounds as of Sept. 7, while the remaining lenders provided about 3.9 billion pounds.

“Hard work remains over the coming months and years to ensure that the risks to value for money are minimized,” the British Business Bank said.

©2020 Bloomberg L.P.