U.K.’s Favorite Pizza Set to Survive Debt Restructuring

U.K.’s Favorite Pizza Set to Survive $1.4 Billion Debt Overhaul

(Bloomberg) -- Twitter users following the #savepizzaexpress hashtag this week will probably get what they want, at least in part.

Creditors to troubled casual-dining group PizzaExpress Ltd., which has around $1.4 billion of debts, expect to see much of their money returned and the brand survive, according to analyst Helen Rodriguez at CreditSights in London.

“There’s a brand and a business for PizzaExpress, it just has the wrong balance sheet and needs to reduce its debt,” she said. “If it were to restructure, someone would certainly want to start again with the business.”

That will come as a relief to many in the U.K., for whom the chain is something of a national icon. When Bloomberg reported on Oct. 4 that the company had hired advisers for talks with its creditors, it triggered an outpouring of emotion on social media from Britons who had grown up with the brand and feared its demise.

A representative for PizzaExpress declined to comment.

Bondholders are considering a company voluntary arrangement to close unprofitable restaurants, the Sunday Telegraph reported, citing a person it didn’t identify. Lenders fear about 40% of PizzaExpress’s 470 U.K. outlets don’t make money, putting more than 150 restaurants and about 3,300 jobs at risk, the newspaper said.

“I refuse to believe that anyone growing up in the U.K. can have passed through life without experiencing the marble table tops, blue glass vases and dough balls that define PizzaExpress,” fashion magazine Grazia wrote in a “love letter” to the chain on Oct. 7.

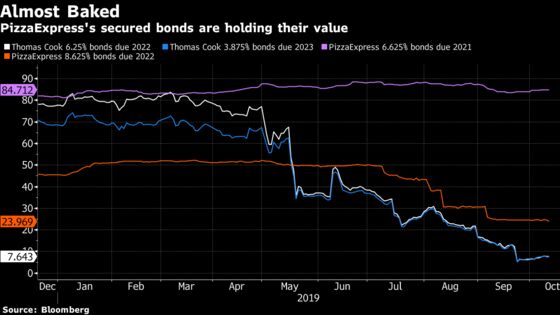

Bond investors don’t believe it either. The most senior debt issued by the group that will be paid back first if the company flounders, is trading above 80% of face value. Even the junior bonds first in line for losses are still quoted at more than 20 pence on the pound, according to data compiled by Bloomberg.

That means investors think debt-restructuring talks are likely to yield a solution where lenders get some or even most of their money back.

A common outcome in restructurings is to pay off debt by converting it into shares, handing control of the company to creditors. Holders of PizzaExpress’s secured bonds will be in the driver’s seat when talks kick off, according to CreditSights’ Rodriguez.

This group has included investment funds like Cyrus Capital Partners Europe LLP, HIG Capital LLC and Marathon Asset Management LP. Hedge fund Beach Point Capital Management is among a separate group of unsecured creditors also preparing for debt talks, according to people familiar with the matter who asked not to be identified discussing private information.

A representative of Cyrus declined to comment. Officials at HIG, Marathon and Beach Point didn’t immediately respond to requests for comment.

That outcome, where PizzaExpress survives under new owners and creditors get a large portion of their money back, would contrast with the fate of Thomas Cook Group. The travel firm, also a common fixture in British town centers, collapsed last month with lenders set to lose most of their investments, if not all.

PizzaExpress’s troubles stem from a broader malaise afflicting Britain’s shopping streets that’s hit retailers and eateries alike. Its competitor Prezzo shut down 94 of its restaurants last year, while celebrity chef Jamie Oliver’s dining chain filed for insolvency in May.

Fashion chain New Look is now owned by its lenders after the company restructured its 1.35 billion pounds ($1.7 billion) of debt earlier this year. Department store Debenhams is also controlled by creditors after shareholders including retail tycoon Mike Ashley were wiped out in debt talks in April.

Negotiations between PizzaExpress and its creditors will need to take into account the company’s next debt payments. The company is due to pay 24 million pounds in bond interest in February and has a 20 million-pound bank facility maturing in August.

Chinese investment firm Hony Capital Ltd. bought the company from Cinven in 2014 in a 900 million-pound leveraged deal that left the company laden with debt. On top of 665 million pounds of bonds, the company also has a shareholder loan amounting to 467 million pounds, according to filings.

“Although the company is highly leveraged, it doesn’t seem it’s running out of cash,” said Joanna Ford, an insolvency and restructuring partner at law firm Cripps Pemberton Greenish. “A debt-for-equity swap might be a way to promptly fix its capital structure, provided the creditors see a future for the brand, which I can personally see as still quite strong.”

--With assistance from Luca Casiraghi and Heather Burke.

To contact the reporters on this story: Katie Linsell in London at klinsell@bloomberg.net;Antonio Vanuzzo in London at avanuzzo@bloomberg.net;Laura Benitez in London at lbenitez1@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Amanda Jordan

©2019 Bloomberg L.P.