Two Words That Sent the Oil Market Plunging: Negative Gamma

Two Words That Sent the Oil Market Plunging: Negative Gamma

(Bloomberg) -- As oil suffered its biggest one-day slump in three years, it wasn’t OPEC or President Donald Trump that was shaking the market. Instead, trading desks were abuzz with chatter of “negative gamma.”

So what is it?

This obscure concept starts out on the options desks of Wall Street. There’s a lucrative business for banks that facilitate trades allowing crude producers -- individual companies, or sometimes entire countries -- to reduce their exposure to volatile markets by locking in a price for their future production.

Say the government of a large exporter needs $60 a barrel to balance its budget and wants to avoid running a deficit in the event that prices slump. For a fee it can acquire the right to sell its production for $60 guaranteed, otherwise known as a put option.

If prices stay above that level, the contract is never exercised and the producer’s counterparty -- often a bank -- keeps the fee. If crude is below $60, the country uses the option and still gets to balance its budget.

This seemingly sensible approach to risk management can suddenly boost volatility when price swings are large enough that buyers of those contracts start to earn big profits. As the options become increasingly valuable, banks have to sell more and more futures contracts to try and contain their losses.

This can become a vicious cycle: Traders frenetically sell futures to manage their options exposure; that drives down prices and brings more options into the danger zone; dealers are then forced to sell even more crude contracts.

That’s the negative gamma effect -- so called because options traders use Greek letters to gauge how sensitive options contracts are to price moves in the underlying asset.

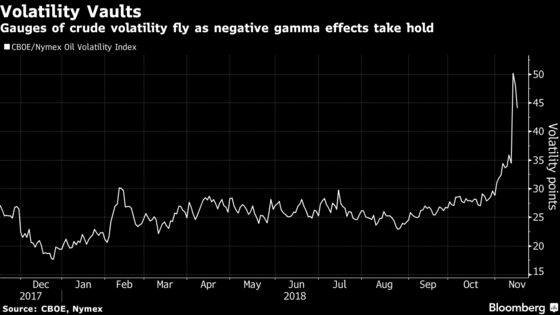

Its impact on Tuesday, when West Texas Intermediate crude slumped $4.24 to $55.69 a barrel, was exacerbated by the large number of options involved. The December options contract, which expired that same day, had more than 33 million barrels of puts at $60 and 31 million barrels of $55 puts outstanding. Over the next 12 months, the most held WTI contracts are $60 puts, $55 puts and $50 puts. The CBOE/Nymex Oil Volatility index remained near a two-year high at around 45 points on Thursday.

“These large ‘negative gamma’ effects have become important in the current price environment as producers had already sold a large amount of forward production on the way up,” Goldman Sachs Group Inc. analysts including Jeff Currie wrote in a report this week.

While many of those contracts are locked in by commercial producers, Mexico’s national oil hedge is the thing that really looms over the market. In 2008 and 2009, banks who had sold Mexico put options were forced to sell oil futures to cover their position in an already falling market, further contributing to the decline. The country has spent about $1.2 billion to lock in crude prices for 2019.

Know Your Greek

| Letter | What’s it used for? |

|---|---|

| Delta | To judge the impact of oil price changes on options |

| Gamma | Measures how quickly the delta changes as prices move |

| Theta | The sensitivity of an option’s value to the change in time until expiration |

| Vega | The impact of changes in volatility on an option’s value |

--With assistance from Javier Blas, Jack Farchy, Amanda Jordan and Fred Pals.

To contact the reporter on this story: Alex Longley in London at alongley@bloomberg.net

To contact the editors responsible for this story: Alaric Nightingale at anightingal1@bloomberg.net, James Herron, John Deane

©2018 Bloomberg L.P.