Two Shots Fired May Break This Rally Wide Open: Taking Stock

Two Shots Fired May Break This Rally Wide Open: Taking Stock

(Bloomberg) -- Today’s equities action can’t ignore China -- even with potential developments from Salesforce.com, Amazon and crude prices hovering.

It’s been on investors’ minds for months now, and it’s clear that each potential new development is desperate to be believed despite incessant disappointment. Think about all the times we’ve heard "a deal is near," or "we’re making great progress." Though all of these things may be true, the only technical issue is what your definition of "near" and "progress" happens to be. But there’s some reason to be more optimistic today, and that comes from two developments on the Chinese side of the equation (I guess the investment community is now at a point where we place more credence on China than the U.S.?). But I digress.

Bloomberg reporting over the weekend, as mentioned above, was that the U.S. and China are close to a trade deal that could lift most or all U.S. tariffs as long as Beijing follows through on pledges. That builds upon some of the earlier developments late last week, and was then confirmed when China followed up on those same reports by indicating that there was substantial progress made, including on a foreign investment law that would strengthen IP protection, which does bode well (they also are said to be planning new stimulus measures to boost a slowing economy, which can’t hurt sentiment). IP is thought to be one of the main sticking points in the talks, so any needle movement there is crucial. And given where we are on the S&P (just points from the November highs if the futures hold, up nearly 10 handles as of writing), real developments are required to push upwards.

But for Today

The real estate and foods segments will need to process what happened Friday -- mainly the Amazon.com bombshell that it was seeking to open lower cost grocery stores (a company blamed for the death of retail is expanding in retail -- what symmetry!). Without that news, it’s likely the staples sector would not have fared that terribly (WMT and KR were among the largest drags in the segment). The respective grocers are indicated to open higher this morning, likely with the greater market, but clearly a sign that impending doom is far from around the corner.

The silver lining as I see it is that the newfound investment could boost the health of some of the lagging malls in America that lack decent anchors. Bloomberg Intelligence REIT analyst Lindsay Dutch said Friday that from the report it wasn’t quite clear where the stores would be going (strip malls or otherwise), but that it would likely "increase demand for retail real estate."

The only other major issue to watch is Salesforce.com, which is due to report later today. The software-as-a-service giant extended its rally streak to seven days on Friday, setting yet another all-time high. As mentioned Friday, JPMorgan analysts called the upcoming fourth quarter results a “celestial event” with "tough" comps for bookings and billings, despite the company ecosystem’s “remarkable health and resilience.” Piper Jaffray expects to see a "solid demand environment" and analysts are bullish on the long-term prospects for the firm that, despite its rally, still trades at a "relative discount to peers." Their checks indicated that the quarter "largely met expectations," and so we’ll see if its largely priced in or not.

Bring Up the Energy Level

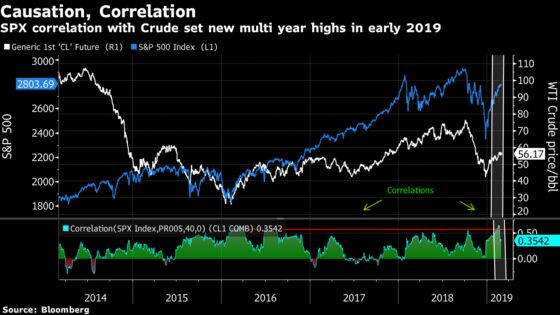

In addition to the Salesforce.com results, analyst days for two of the largest integrated oil names will be coming this week. It will be especially interesting to hear the outlook from the majors given the correlation we’ve seen between oil and the S&P as shown in the below graphic.

Cowen analyst Jason Gabelman last week wrote that they expected CAPEX forecasts to remain stable for Exxon (prior multi year views were to exceed $30 billion), while Bloomberg avg ests. for 2019 are $25 billion, 2020 at $26 billion. Gabelman was expecting a reiteration on strategy for Guyana, Permian, PNG LNG, Mozambique and Carcara, so with any adjustment there, we may see some price action. It will be interesting to hear if there are any comments on the unrest seen in Mozambique that resulted with an armed gunman attack at an Anadarko site in late February.

Ultimately though, crude prices will remain the driver. The energy sector has been the worst performing sector group over the past 6 months (though among the top performers in 2019), and that is part of the thesis to consider ownership in the segment, at least according to Morgan Stanley strategists. Some of the biggest bears on the street as far as their overall 2019 forecasts for the S&P, they did advocate last week to be "overweight a mix of cyclicals with depressed multiples (Financials & Energy)" along with some defensives.

Your 63-Hour ICYMI

Vijah Singh narrowly missed out on becoming the oldest player ever to win on the PGA tour at the Honda Classic; Gene therapy names were mentioned positively in Barron’s, as potential targets for larger pharmaceutical players -- stocks mentioned included SRPT, VYGR, BOLD, BMRN, QURE, MGTX; Todd Gurley of the LA Rams reportedly has arthritis in his injured knee; Elon Musk’s SpaceX docked an unmanned vehicle with the International Space Station; Jon Jones defeated Anthony Smith for the light heavyweight title despite an illegal kick that cost him two points; Square co-founder Tristan O’Tierney died, aged 35. He had left the company in 2013; Roger Federer won his 100th singles title, with only Jimmy Connors now having more, at 109; Some Vale executives have stepped aside after the dam disaster; LeBron James’ Lakers lost to the last place Phoenix Suns, putting playoff hopes (if there were any left) in jeopardy; Safe dividend stocks identified in Barron’s included ABBV, AVGO, JPM, TROW, SLG, MPC, PSX; President Trump was critical of the strong dollar and attacked the FOMC chair (again) for raising rates

Sectors in Focus Today

- Cloud and SaaS names (VEEV, ULTI, SAP) ahead of CRM’s results post market

- Diabetes names (NVO, SNY) after Lilly announced a lower priced Humalog insulin

- NIO and other electric makers (and potentially lithium players, ALB, SQM) after Tesla’s Musk announced they would unveil the Model Y in the coming weeks. The model is expected to be built with many elements of the cheaper Model 3

Notes From the Sell Side

Kraft Heinz had a rough week after never really recovering from results, a dividend cut and writedown that sent shares plunging. Morgan Stanley analysts led by Dara Mohsenia are now ready to declare that the "wurst" is now over in the name, upgrading the rating to equal-weight. The analysts still have a bearish outlook on the condiment and packaged food supplier, but that outlook is now "appropriately" discounted in the outlook. They write that the 2019 EBITDA views are "reasonable" and see possible upside if 3G gets further involved. Shares are indicated to open up by more than 2%.

Group 1 Automotive shares are getting a slight boost this morning after Goldman Sachs analysts led by David Tamberrino raised their rating to buy from neutral given their expectation for shares to outperform peers. The auto dealer’s largest markets are set to outperform the industry following strategic initiatives to boost margins and improved gross profits from its integrations of acquisitions in the UK, they write. (NOTE: The co. attributes 4% of its sales to Brazil and nearly 18% to the U.K, according to data compiled by Bloomberg)

Tick-by-Tick Guide to Today’s Actionable Events

- Carnival in Rio

- RSA Security Conference starts in San Francisco (ORCL, PFPT, IBM, INTU, CSCO, FEYE, AKAM)

- Citi Global Property CEO conference (CBL, SLG, CPT, KRC, EQIX)

- FSCT investor day

- Pdufa date for J&J’s esketamine

- 10:00am -- Dec. Construction spending

- 4:05pm -- CRM results

- 5:00pm -- CRM earnings call, CTRP earnings

- 5:30pm -- HUYA earnings

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.