Trouble Is Brewing in the Darkest Corner of China’s Shadow Banking

Trouble Is Brewing in the Darkest Corner of China’s Shadow Banking

(Bloomberg) -- Analysts on the lookout for China’s next financial shock are training their sights on the least regulated corner of the nation’s sprawling shadow banking system.

Their concern centers on so-called independent wealth managers, which have expanded rapidly in recent years by selling high-yield products to affluent investors. Largely untouched by a government clampdown on nearly every other form of non-bank financing, the industry has grown from obscurity into a major source of funding for cash-strapped Chinese companies.

The worry now is that products arranged by independent wealth managers will face mounting losses as China’s economic slowdown deepens and corporate defaults surge. Confidence in the industry has plunged since July, when Noah Holdings Ltd. said that 3.4 billion yuan ($477 million) of credit products overseen by one of its units were exposed to an alleged fraud by a Chinese conglomerate. U.S.-listed shares of Noah, one of China’s biggest independent wealth managers, have tumbled 38% in the past three months.

“I wouldn’t be surprised to see some losses,” said Jasper Yip, Hong Kong-based principal of financial services at Oliver Wyman, a consulting firm. “More borrowers will run into payment difficulties in a slowing economy.”

The repercussions could be significant if losses on such products fuel a broader retreat from high-yield assets in the world’s second-largest economy. One factor that concerns analysts: Because the products are opaque and regulation is minimal, nobody knows exactly how much money is at risk.

What’s clear from financial statements published by Noah and Jupai Holdings Ltd., another U.S.-listed independent wealth manager, is that the industry has experienced breakneck growth.

Assets under management at a Noah unit that structures its own products climbed 40% to 169.2 billion yuan in the two years ended December 2018 -- a period when the broader Chinese shadow banking system shrank because of tighter regulations. Jupai’s assets under sole or shared management have more than quadrupled since 2015 to 56.8 billion yuan, according to the company. Official industrywide figures don’t exist, but Noah estimated in 2016 that China had upwards of 8,000 independent wealth managers.

While the firms offer a wide variety of investments including plain-vanilla mutual funds, many of the products are backed by high-yield loans to companies -- often property developers -- that lack access to traditional sources of funding like banks.

Because the credit products are sold only to investors who have at least 3 million yuan of financial assets or earned an average 500,000 yuan in the past three years, they fall outside the increasingly strict rules governing mainstream wealth management products offered by Chinese banks. While WMP holdings of non-standard credit assets (mostly corporate loans) are capped at 35%, the credit products issued by independent wealth managers aren’t subject to any such limits.

That has allowed them to ramp up exposure to riskier debt and offer higher yields, a major draw for investors at a time when the rates on traditional WMPs have been falling. Marketing materials for some of Noah’s products show an expected annualized return of 7.7% for an investment duration of 9 months, five times higher than the benchmark deposit rate.

Critics of independent wealth managers including Sun Jianbo, president of China Vision Capital Management in Beijing, argue that the firms often understate the risks of their products when marketing to investors.

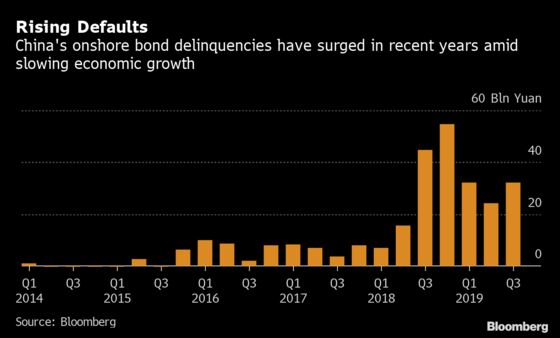

That worry has only deepened in recent months as China’s economy slowed to the weakest pace since at least 1992 and the nation’s companies defaulted on domestic bonds at the fastest pace on record. Noah’s failure to spot the risks of lending to Camsing International Holding Ltd., the conglomerate it accuses of fraud and whose chairman was detained by Chinese police in June, provided another reason for caution. The Camsing case is still under investigation by police, who haven’t announced any charges.

Noah said in an emailed statement that it’s offering loans at preferential rates to some clients whose money is tied up in products affected by the case. Camsing and the China Securities Regulatory Commission didn’t respond to requests for comment. Jupai, whose stock has dropped 50% in New York this year, didn’t reply to questions on its market performance.

Because independent wealth managers focus on affluent investors, they may pose less of a systemic risk than other segments of China’s shadow banking system that cater to the nation’s masses.

And while China’s financial regulators have so far refrained from tightening restrictions on the industry, that could soon change. The CSRC published draft rules in February for wealth managers and distributors of investment products that would increase punishments for those that fail to disclose risks properly. The Shenzhen Asset Management Association last month published draft rules on winding down products that run into trouble, saying that some wealth managers have failed to meet professional standards.

The proposed regulations will help reduce risks, but in all likelihood the industry’s problems are bigger than most investors realize, according to Liu Shichen, Shanghai-based head of research at Z-Ben Advisors, a fund management research firm.

That’s partly because many wealth managers have been using their own capital to make clients whole when products suffer losses, he said. (Noah and Jupai said they don’t use their own cash to repay investors.)

“What we have seen is only a fraction of the problematic products,” Liu said.

--With assistance from Molly Dai.

To contact Bloomberg News staff for this story: Evelyn Yu in Shanghai at yyu263@bloomberg.net;Jun Luo in Shanghai at jluo6@bloomberg.net

To contact the editors responsible for this story: Jun Luo at jluo6@bloomberg.net, Michael Patterson

©2019 Bloomberg L.P.

With assistance from Bloomberg