Treasury Yields Hammerlocked as Fed Optimism Meets Global Risks

Treasury Yields Hammerlocked as Fed Optimism Meets Global Risks

(Bloomberg) -- Headwinds from Rome to Riyadh have helped to cap the recent surge in Treasury yields, while the combination of Federal Reserve policy tightening and increasing debt supply appears to be providing a firm floor for U.S. rates.

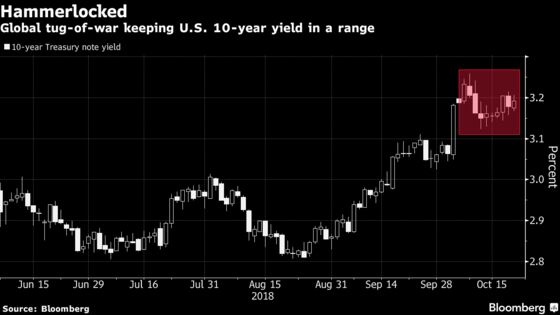

The tug-of-war that has kept America’s 10-year yield boxed within a 14-basis-point range for the past two weeks looks set to continue as traders weigh the U.S. growth outlook against risks that could spur a flight to haven assets. Minutes from the Fed’s last gathering indicated it’s willing to keep lifting rates even to the point of restricting growth, providing a boost to yields. At the same time, the market is on edge over Italy’s budget standoff, Brexit and the death of Saudi Arabian journalist Jamal Khashoggi. Equity volatility is also a risk, as are signs of dollar funding pressures at the front end.

The coming week will provide insights on the U.S. growth picture from gross domestic product data, and potentially some clues into Fed thinking, with new vice chairman Richard Clarida delivering his first major address. There will also be an influx of new Treasury supply at the shorter end of the market that may give renewed impetus to curve flattening. Italy, which had its credit rating cut by Moody’s Investors Service on Friday, is likely to remain in focus too, along with America’s ongoing trade spat with China, while the Saudi situation has the potential to upend oil and other markets.

“The Treasury market is very skittish now,” said Subadra Rajappa, head of U.S. rates strategy at Societe Generale SA in New York. “The markets’ perception of some of these events is very binary. Still, from a fundamental perspective, both growth and inflation are looking positive in the U.S. and Fedspeak shows they don’t seem to have nearly as much concern over these global developments as they have in past years.”

All of this creates a backdrop that will keep 10-year yields stuck within a broad range of about 3 percent to 3.25 percent over the next few weeks, according to Rajappa.

Libor Pressure

The 10-year yield rose about three basis points in the past week to 3.19 percent, swinging within a range of just over seven basis points. Rates at the short-end of the curve rose more, helping to flatten the yield curve between 2-and-10 year securities for a second straight week, and upward pressure was most evident in dollar-based money markets.

The three-month London interbank offered rate, which serves as the basis for trillions of dollars in loans and floating-rate securities globally, recorded its biggest one-week surge since March, reaching a level unseen since November 2008. Part of that gain stemmed from firming expectations about Fed hikes, although there has also been a widening of the spread over overnight index swaps that move in sync with monetary policy expectations and the approach of year-end funding needs is also having an impact. The increase in Libor could add to strains on some companies and emerging economies and is one of several signs that pressure is growing in dollar funding markets.

What to Watch In the Coming Week

- An array of Fed speakers on the agenda:

- Oct. 23: Minneapolis Fed President Neel Kashkari speaks at a conference; Atlanta Fed President Raphael Bostic speaks at Louisiana State University; Dallas Fed President Robert Kaplan speaks in Galveston, Texas

- Oct. 24: Kansas City Fed President Esther George speaks at a conference in Sydney; Fed’s Bostic speaks in Baton Rouge; Cleveland Fed President Loretta Mester speaks in New York; Fed Governor Lael Brainard speaks in New York

- Oct. 25: Fed Vice Chairman Richard Clarida speaks in Washington; Fed’s Mester speaks in New York

- The week’s most notable economic reports include Friday’s GDP data and the Fed’s Beige Book on Wednesday

- Oct. 22: Chicago Fed activity index

- Oct. 23: Richmond Fed manufacturing index

- Oct. 24: MBA mortgage applications; FHFA house price index; Markit manufacturing and services PMI; new home sales; Fed Beige Book

- Oct. 25: Trade balance; wholesale and retail inventories; durable and capital goods orders; jobless claims; Bloomberg consumer comfort; pending home sales; Kansas City Fed manufacturing activity

- Oct. 26: First estimate third quarter GDP; University of Michigan consumer sentiment index

- The Treasury will auction bills and notes:

- Oct. 22 brings $45 billion of three-month bills and $39 billion of six-month bills, while sales of four-week and eight-week bills are slotted for Oct. 23

- Treasury to sell $38 billion of two-year notes on Oct. 23, $39 billion of 5-year notes on Oct. 24, and $31 billion of 7-year notes on Oct. 25; it will also issue $19 billion of two-year floating-rate notes on Oct. 24

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Jenny Paris

©2018 Bloomberg L.P.