Treasury Curve Flattens as Jobs Report Leaves Fed Outlook Intact

Treasury yields climbed after U.S. employment data showed underlying strength.

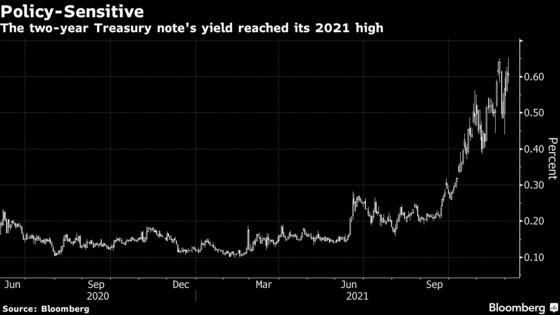

(Bloomberg) -- The U.S. two-year note’s yield reached the highest level of the year after U.S. employment data showed underlying strength and wage pressures viewed as likely to keep the Federal Reserve on a path toward tightening monetary policy next year.

The policy-sensitive two-year note’s yield climbed to 0.653%, eclipsing its prior peak reached Nov. 24. Yields across the curve subsequently retreated from session highs as U.S. equity benchmarks fell and were mostly lower shortly before midday in New York, with the two-year little changed on the day.

The climb in the two-year yield has the “makings of a breakout,” said Kevin Flanagan, head of fixed income strategy at Wisdom Tree Investments. “The rise in short-dated yields is indicative of an impressive labor market that allows the Fed to discuss a faster pace of tapering at its December meeting.”

While the November nonfarm payrolls increase of 210,000 was less than half the median estimate of economists in a Bloomberg survey, a drop in the unemployment rate to 4.2% from 4.6% along with wage gains and increased labor-force participation painted a more complicated picture.

Overall, the jobs data were seen as allowing the Fed to proceed with a faster wind-down of its asset purchases -- which Chair Jerome Powell and several other central bank officials this week said was called for in light of persistent inflation -- and possibly to begin raising rates by the middle of 2022.

“The turn-around in the two-year note is the market figuring out that this is not a disappointing payroll report that takes the Fed out,” Jeffrey Rosenberg, senior portfolio manager for systematic fixed income at BlackRock Inc., said on Bloomberg Television. “The narrative is still the same, pricing in the acceleration. How far the market gets ahead of the Fed and whether the market can push the Fed to go even further than that is kind of the next phase.”

The upward pressure on short-dated Treasury yields resulted in a flatter curve as 10-, and 30-year Treasury yields fully erased their increases and slid to session lows as stocks fell. Curve-flattening has dominated the bond market in recent weeks, reflected in expectations that Fed rate hikes next year will tame inflationary pressure and potentially slow the economy.

“If people think that the Fed can hit 2.5% on their funds rate or even get higher than that, I think they’re really missing the big picture here,” said Michael Collins, senior portfolio manager at PGIM. As the central bank tightens policy, there is the prospect that “demand is going to be slowing more quickly than people think” and “inflation is going to be coming down,” said Collins. The policy rate will probably peak at 1% or 1.5%, “and I think that’s what’s priced in right now.”

©2021 Bloomberg L.P.