Treasury Market Set for a Respite From Record Supply Onslaught

Treasury Market Set for a Respite From Record Supply Onslaught

(Bloomberg) -- The world’s biggest bond market is set to get a reprieve from the past year’s torrid onslaught of ever-increasing auction sizes.

Most Wall Street dealers predict Treasury Secretary Janet Yellen’s debt managers will hit the pause button for the next few months, after the department hoisted long-term auctions to unprecedented sizes the last three quarters to finance pandemic relief. Officials will announce their issuance plans on Feb. 3.

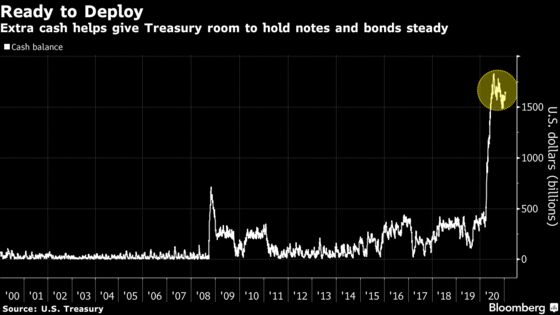

A respite would still leave the market having to digest a massive serving of bonds: The Treasury’s refunding sales are expected to remain at historically large levels. And federal deficit spending is still on an upward trajectory, with President Joe Biden proposing an additional $1.9 trillion of virus aid. The reason the Treasury can hold off on boosting note and bond sales now is that it ramped them up so much last year, and it also has a cash balance of about $1.6 trillion that it can tap. All things being equal, the pause may ease some of the upward pressure on yields that many analysts anticipate in 2021.

“Treasury is pretty well funded now,” said Blake Gwinn, director of U.S. rate strategy at NatWest Markets. “It’s a good time for them to take a break from the really aggressive campaign of coupon debt increases that we’ve had for almost the last year. And there’s also a large degree of uncertainty regarding how much of Biden’s package actually gets done and when.”

Gwinn -- along with most Wall Street strategists -- expects the Treasury will whittle down its cash pile and possible adjust T-bill issuance for any funding needs over the next three months. A move to reduce its cash may also be prudent given that the department will need to shrink that pile if Congress doesn’t lift the debt ceiling or re-suspend the current limit, which ends July 31. In that scenario, Treasury is mandated to return its cash balance to the level it was at the time the last suspension was put in place, in 2019.

Still, Treasury’s 8:30 a.m. Washington time refunding announcement on Wednesday will be a key event for bond traders as always. That’s especially true given that Yellen has just taken the helm at Treasury and now oversees the nation’s borrowing policy.

Market Significance

The significance of the issuance outlook for the roughly $21 trillion Treasuries market was evident in early January. Ten-year yields, a benchmark for global borrowing, spiked above 1% for the first time since March on speculation that unified Democratic control of Congress made another massive round of debt-financed stimulus likely.

Goldman Sachs Group Inc., Jefferies, UBS Group AG and Credit Suisse are among firms making the consensus call that Treasury won’t lift nominal note and bond auction sizes. A few outliers, including Barclays Plc and Morgan Stanley, anticipate an increase.

A consensus outcome means Treasury’s refunding sales, to be held in the second week of February, would be as follows:

- $58 billion of 3-year notes ($4 billion more than the November refunding, but unchanged from this month)

- $41 billion of 10-year notes (same as the November refunding)

- $27 billion of 30-year bonds (same as the November refunding)

- The total of $126 billion would be $4 billion more than was sold at the November refunding, and would mark a record for the round -- but that’s only because Treasury lifted 3-year notes by $2 billion in December and again in January.

“Treasury will keep everything steady this meeting, using it as an opportunity to take stock of things,” said Priya Misra, head of global rates strategy at TD Securities. “They came into the year over-funded and need to bring the cash balance down anyway. Treasury also wants to keep their flexibility as there could be $1 trillion more in stimulus, or no more at all.”

Murky Path

The path of government spending is murky given it’s unclear just how much of his plan Biden can get through Congress. Republican lawmakers have signaled enthusiasm only for the $160 billion earmarked for Covid-19 testing and vaccines.

Democrats could also bring other portions of the proposal through Congress in a so-called reconciliation bill, which allows the Senate to proceed on a simple-majority vote -- avoiding the need for 60 votes to block a filibuster. Yet some Democrats have balked at the size of the aid, and specifically to the $1,400 checks Biden wants to distribute to households. The loss of just one Democrat could doom any legislation with the Senate split 50-50 between the two parties.

Dealers expect sales of Treasury Inflation-Protected Securities to grow, a plan the government detailed in November. Officials may also give more insight into their consideration of issuing debt linked to the Secured Overnight Financing Rate, the successor to the scandal-plagued Libor benchmark.

Upward Trajectory

The sense in the bond world is that a recovering economy and ultraloose Federal Reserve policy will push long-term borrowing costs higher in 2021, but only modestly. The median forecast among analysts surveyed by Bloomberg is for the 10-year rate to reach 1.3% in the fourth quarter, from 1.07% now. That would still be below levels seen at the start of 2020 -- of around 1.6% -- before the pandemic rocked markets.

The economic highlight of the coming week is expected to drive home the rocky road ahead. Labor data set for release on Feb. 5 are forecast to show 58,000 nonfarm jobs were created in January, a meager rebound from the surprise loss of 140,000 in December.

“Monetary policy will remain as accommodative as possible for the foreseeable future,” said Nick Maroutsos, head of global bonds at Janus Henderson Investors, which manages $358 billion. “Growth will bounce as we move out of Covid, but overall it will be subdued and that will likely put a cap on yields.”

What to Watch

- The economic calendar:

- Feb. 1: Markit U.S. manufacturing PMI; construction spending; ISM manufacturing

- Feb. 3: MBA mortgage applications; ADP employment; Markit U.S. services PMI; ISM services

- Feb. 4: Challenger job cuts; unit labor costs; jobless claims; Bloomberg consumer comfort; factory orders; durable goods, capital goods

- Feb. 5: Nonfarm payrolls; trade balance; consumer credit

- The Fed calendar:

- Feb. 1: Minneapolis Fed’s Neel Kashkari; Dallas Fed’s Robert Kaplan; Atlanta Fed’s Raphael Bostic and Boston Fed’s Eric Rosengren at conference

- Feb. 2: Kaplan; Cleveland Fed’s Loretta Mester

- Feb. 3: Kashkari; St. Louis Fed’s James Bullard; Philadelphia Fed’s Patrick Harker; Mester; Chicago Fed’s Charles Evans

- Feb. 4: Kaplan; San Francisco Fed’s Mary Daly

- The auction calendar:

- Feb. 1: 13-, 26-week bills

- Feb. 4: 4-, 8-week bills

©2021 Bloomberg L.P.