Bets on Fed Show More Than One 2019 Cut Possible as Bonds Rally

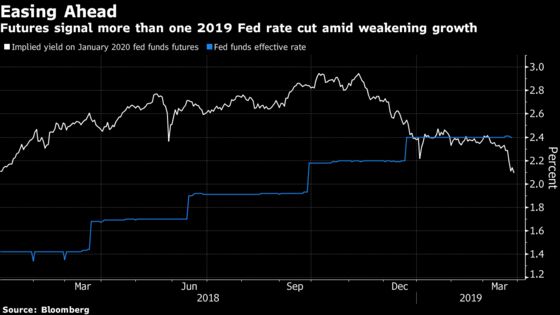

Fed funds futures are now pricing in more than 30 basis points of easing by the end of 2019.

(Bloomberg) -- Traders amped up bets on Federal Reserve interest-rate cuts this year and Treasuries surged as investors around the world sought the safety of bonds amid increasing concern about a slowdown in global growth.

Fed funds futures are now pricing in more than 30 basis points of easing by the end of 2019, suggesting at least one quarter-point cut. Benchmark 10-year yields tumbled to their lowest level since December 2017, touching 2.35 percent.

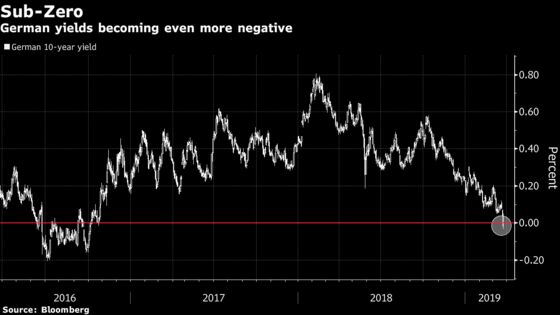

A surprise move by New Zealand’s central bank to signal that its next shift would likely be a cut also stoked gains in bonds. Meanwhile, Germany’s benchmark yield slid further below zero after the nation sold 10-year notes at a negative rate for the first time since 2016.

“There are lingering concerns about the growth prospects in the U.S.,” said Alex Li, head of U.S. rates strategy at Credit Agricole SA. “Investors’ mindset has changed after the Fed last week revised their growth forecasts and removed all the rate-hike dots for 2019.”

Given benchmark 10-year yields have now broken below a range that had held since the start of the year, Li is advising investors to step to the sidelines and not fight the trend.

Money-market traders continue to extend the amount of Fed easing they see this year, predicting the central bank will reverse course on policy even as officials have signaled only that they’ll stand pat on rates. The implied rate on fed funds futures that expire in January 2020 has fallen from 2.14 percent on Tuesday to 2.09 percent. That compares to the overnight benchmark targeted by the Fed, currently at 2.40 percent, and implies more than one full cut is priced in for this year.

Reverse Course?

One potential policy maker who appears willing to push toward easing is Stephen Moore, whom President Donald Trump may nominate for a seat on the Federal Reserve Board. Moore told the New York Times in an interview that the central bank should immediately reverse course and lower rates by half a percentage point.

Monetary policy in Europe appears poised to support global debt as well. European Central Bank President Mario Draghi said the risks to the euro area are tilted to the downside, while any pickup in inflation is delayed.

“The race to the bottom continues for government bond yields,” Fawad Razaqzada, a technical analyst at Forex.com, wrote in a note. “Central banks have turned dovish in recent months owing to evidence of a slowing global economy.”

Haven demand was also spurred by concerns in emerging markets, with the Turkish lira weakening as traders grappled with the government’s curbs on trading the currency. Developing-market stocks slipped, as did U.S. shares.

Auction Appetite

The Treasury received about average demand for its $41 billion sale of five-year notes, which drew a yield of 2.172 percent. That was slightly above where the market was pricing the issue just before the bidding ended. The sale was of particular interest given the recent outperformance of that part of the curve, generally referred to as the belly.

The speed of the decline in U.S. yields has also been fueled by mortgage-related hedging in the swaps market, said Credit Agricole’s Li. That’s because a drop in financing costs likely sparked more people to refinance their mortgages, cutting mortgage-bond holders’ duration.

Ten-year Treasuries yield about 2.38 percent, down four basis points from Tuesday. Yields on 10-year bunds fell seven basis points to around minus 0.08 percent.

Marty Mitchell, an independent strategist, said in his daily newsletter to clients that increasing amounts of negatively yielding bonds outside America have supported the U.S. market and there are also haven flows into Treasuries. He recommended clients continue to “buy the dips” in Treasury prices, and noted downside yield support at 2.34 percent, 2.32 percent and 2.3 percent.

Market Hesitation

Binky Chadha, a strategist at Deutsche Bank AG, has indicated that the move in yields and rate-cut bets may have its limits, and could even reverse.

“Further declines in the 10-year require pricing in of more rate cuts, but since 2014, the market has been hesitant to price more than 1 rate move by the Fed in either direction,” Chadha wrote in a note. “In the absence of very negative data or worsening of any of the long list of well known risks, the market is unlikely to take a strong view on further rate cuts and this argues for a V-shaped move in the 10 year.”

Some derivative traders are already beginning to wager against the move in rates. A fresh wave of eurodollar options trades was put on Wednesday, with the motivation appearing to be betting against the dovish pivot across the front-end.

A closely watched segment of the U.S. curve that’s often seen as a harbinger of recession when it flips moved deeper into inversion. The 3-month rate last week dipped underneath the 10-year yield for the first time in more than a decade and on Wednesday it fell to as much as 11 basis points below. In the lead-up to the economic downturn that began in December 2007, this part of the curve initially went negative about 23 months before the recession started.

Quantitative Easing

Helping drive long-term yields lower and invert the curve is investors’ growing belief that central banks will quickly step in -- beyond just cutting rates -- and support the economy if things look dire, including buying more bonds.

“Market participants believe that if we were to go into a recession the reaction function could be that quantitative easing programs begin again, with central banks going into long-duration bonds,” said Thomas Wacker, head of credit in the chief investment office of UBS Global Wealth Management, which oversees about $2 trillion.

The Fed announced last week that it would end its balance sheet run-off beginning in October, sooner than most strategists had predicted.

There’s little in the way of lower yields the rest of this month, according to Jim Vogel, a strategist at FTN Financial.

“The last five days now is largest volume period of 2019, setting up still more volatility next week as fresh data make their appearance,” he wrote in a note.

--With assistance from Edward Bolingbroke.

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, ;Ven Ram at vram1@bloomberg.net, Mark Tannenbaum

©2019 Bloomberg L.P.