Treasuries’ Best Year Since 2011 Still Has Headwinds to Conquer

For many on Wall Street the case for higher yields persists.

(Bloomberg) -- Treasury bears just went through a rough week, but for many on Wall Street the case for higher yields persists.

The U.S. election results fueled a washout of the market’s record short bet. But investors and strategists alike still see yields plodding higher as the focus eventually turns from uncertainty surrounding the vote to the economic rebound from the pandemic. Federal Reserve monetary support and the prospect of fiscal stimulus, even if it may be smaller than many expected just a week ago, could bolster growth and push up long-term yields.

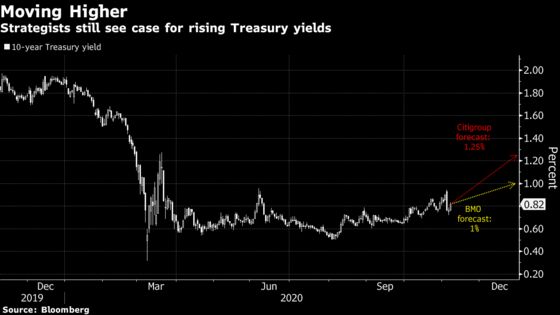

Treasuries are on pace for their strongest year since 2011. However, if strategists at primary dealers BMO Capital Markets and Citigroup Inc. are right, some of the gains may fade. The firms see the 10-year finishing December at 1% and 1.25%, respectively, from 0.82% now. Either level would be the highest since March. Upward pressure emerged Friday after robust jobs data, and it may build as investors digest this week’s unprecedented $122 billion slate of note and bond issuance.

“We’ve had headwinds that prevented the Treasury market from pricing to economic reality,” said Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets. “There is already a ton of economic and monetary-policy stimulus in the system that will eventually translate to upward pressure on prices -- which will correspond to higher inflation expectations and a steeper curve.”

The 10-year yield rose 6 basis points Friday after a stronger-than-forecast report of job gains, paring its weekly decline to 6 basis points. At one point last week, the yield curve reached the steepest since 2016 before the voting results dashed pre-election bets on a Democratic sweep and a major virus-relief package.

Strong Year

Buoyed by a first-half surge as yields sank to record lows, U.S. Treasuries have earned 8.4% in 2020 as of Nov. 5, according to Bloomberg Barclays index data. That leaves them on track for the best year since returning 9.8% in 2011. The market is likely to book solid annual gains even if 10-year yields do climb, given that they ended 2019 at 1.92%.

Bank of America Corp. strategists this past week recommended a tactical short on 10-year Treasuries to profit from a potential rise in yields to about 0.9%. They view the post-election rally as largely fueled by unwinding positions, but they also see a relatively high probability of fiscal stimulus in early 2021.

“The economy is recovering way faster than anyone anticipated,” said Chris Leonard, head of U.S. rates trading at Barclays. “Yet some people have remained skeptical. So the more the recovery continues, it will put pressure on investors and speculators to think Treasury yields will rise.”

Barclays and BMO economists also predict another dose of fiscal aid. Barclays is penciling in about $1 trillion, while BMO anticipates a range of about $500 billion to $750 billion. The Treasury says it is assuming an estimated $1 trillion in further Covid-10 relief through March.

Selloff Hurdles

Granted, there are solid reasons to expect yields may struggle to decisively bust out of the range they’ve held for months. That scenario could push the curve flatter, instead of steeper.

For one thing, the supply deluge may start to ebb given the prospect of more limited government spending should the election ultimately produce a divided Congress.

Of course, the other big headwind for bears is the record-setting pace of new coronavirus cases and the risk of fresh lockdowns.

There’s also the possibility that the Fed steps up its asset purchases, especially if yields climb and risk slowing the economy. The expectation of such action has fueled strong demand on any selloffs for months now.

Gene Tannuzzo, portfolio manager at Columbia Threadneedle, says he sees the 10-year yield’s upside limited for now to about 1% given the Fed’s bond buying, meaning a range of about 0.75% to 1% is likely for the rest of the year.

What to Watch

- It’s a holiday-shortened week for traders, with the U.S. bond market shut Wednesday for Veterans’ Day

- Here’s the economic calendar:

- Nov. 10: NFIB small business optimism; JOLTS job openings

- Nov. 11: MBA mortgage applications

- Nov. 12: Consumer price index; weekly jobless claims; Bloomberg consumer comfort; monthly budget statement

- Nov. 13: Produce price index; University of Michigan sentiment

- The Fed calendar:

- Nov. 9: Cleveland Fed President Loretta Mester, Dallas Fed’s Robert Kaplan

- Nov. 10: Kaplan appears twice; Boston Fed’s Eric Rosengren appears twice; Fed Vice Chair for Supervision Randal Quarles; Fed Governor Lael Brainard

- Nov. 12: ECB’s Christine Lagarde, BOE’s Andrew Bailey, Fed’s Jerome Powell Speak at ECB Forum; Chicago Fed President Charles Evans

- Nov. 13: New York Fed President John William; St. Louis Fed President James Bullard

- The auction calendar:

- Nov. 9: 13-, 26-week bills; 42-, 119-day cash-management bills; 3-year notes

- Nov. 10: 10-year notes

- Nov. 12: 4-, 8-week bills; 105-, 154-day CMBs; 30-year bonds

©2020 Bloomberg L.P.