Virus Fears Squash Reflation Bets in $20 Trillion Bond Market

Treasuries Are Caught Between Vaccine Glee and Inflation Doubts

(Bloomberg) -- There’s a tug of war taking place in the $20 trillion Treasuries market between traders taking heart from progress toward a coronavirus vaccine and those monitoring a resurgence in infections.

Even after U.S. yields climbed last week to their highest level since March, expectations for a pick-up in inflation off the back of an inoculation-induced economic rebound remain muted. The bond selloff looks mostly done for Barclays Plc, while ING Groep NV anticipates a pullback in yields driven by renewed demand for the safety of government debt.

Anxiety over the economic toll of the ongoing virus surge -- plus the U.S. Federal Reserve’s ultra easy monetary policy -- may limit further increases in benchmark yields, which are poised for this year’s biggest two-month jump. Even with a clinical vaccine success, a broader reopening of the global economy will take time. That doesn’t bode well for inflation, which trillions of dollars in monetary and fiscal stimulus have failed to spur.

“While vaccines could be a game changer, the near-term tug-of-war with rising infection rates and weak fundamentals are likely to stymie the reflation trade,” Societe Generale SA strategists led by Subadra Rajappa wrote in a note. “Global disinflationary forces are likely to keep central banks dovish.”

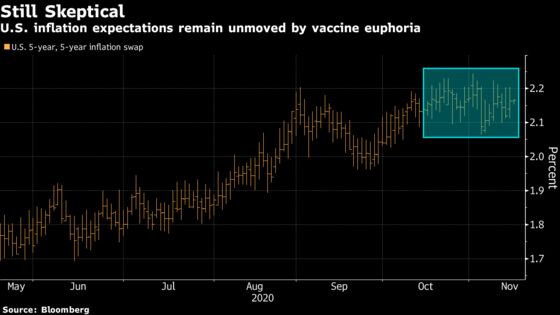

Five-year, five-year U.S. inflation swaps, a gauge of market expectations for consumer-price rises, barely budged on news in the past week about two new inoculations with success rates of more than 90%. They continue to hover in a 2.10%-2.20% range in place since mid-October, while similar measures in Europe languish well below the European Central Bank’s goal of close to, but under 2%.

| Read more: |

|---|

|

Barclays strategists were among those to push back on the reflation narrative favored by analysts such as JPMorgan Chase & Co.’s Marko Kolanovic, who endorsed increasing exposure to stocks and avoiding sovereign bonds following the vaccine news. The U.K. bank sees debt yields capped around current levels, while ING expects the 10-year Treasury rate, which climbed within a whisker of 1% last week, dropping back to 0.75%.

The yield dropped 4.89 basis points Tuesday to 0.86% after data showed U.S. retail sales rose in October at the slowest pace in six months.

Negative Yields

“A large bond market selloff remains unlikely as the ‘post-Covid’ recovery might still be quite long,” Barclays strategists led by Anshul Pradhan wrote.

The global stock of negative-yielding investment-grade debt is still near a $17 trillion record set earlier this month, in another sign that investors remain downbeat on inflation. In Germany, the longest-dated bond yields still languish at minus 0.1%, reflecting doubts over price pressures and expectations that the ECB may have to do more to stimulate the economy.

Global central banks have so far shown little willingness to scale back their unprecedented economic-support policies. The ECB is still expected to further boost its 1.35 trillion-euro ($1.6 trillion) pandemic bond-buying program next month, while the Reserve Bank of New Zealand will begin offering banks three-year loans in early December to help avoid the prospect of negative rates.

Still, the U.S. bond market saw traders reinstate some positions over the past week that imply a pickup in consumer-price pressures in the longer term. The yield premium on 30-year Treasuries over five-year debt climbed toward an almost four-year high following the vaccine reports.

Inflation Outlook

For Russell Silberston, an investment strategist at asset manager Ninety One Plc, inflation is more likely to return in the U.S., given the Fed is willing to tolerate an overshoot of its 2% target.

But across much of the rest of the world, the vaccine news just eliminates the worst-case economic scenarios. Even in the U.S., the central bank could choose to extend the maturity of its asset purchases next month, which could “limit curve steepening,” according to JPMorgan.

“The consensus among policy makers was that there was always going to be a vaccine and that was embedded in their forecasts,” Ninety One’s Silberston said. “All that has changed is that it has come a bit more quickly and appears to be more efficient.”

Years of central bank easing in the developed world -- first in the wake of the financial crisis and now amid the pandemic -- shows that reigniting inflation won’t be an easy task. And in the U.S., whether the fiscal taps open as well, depends largely on the outcome of the senate race.

“The size of the fiscal package likely coming from the U.S. is materially lower than expectations pre-election,” said John Taylor, a money manager at AllianceBernstein LLP. “We’re waiting for a better entry point before building a bigger inflation position.”

©2020 Bloomberg L.P.