Traders on Edge as Fed Looks Poised for Data-Independent Easing

Traders on Edge as Fed Looks Poised for Data-Independent Easing

(Bloomberg) -- Traders face an onslaught of information about the state of the U.S. economy this week. Nevertheless, they’re likely to take their cues directly from the Federal Reserve, since data have proven a poor guide to the path of policy.

Economic reports aren’t dragging the central bank to the interest-rate cut that’s widely anticipated on Wednesday. Numbers due next week are expected to show an uptick in the Fed’s favorite measure of underlying inflation and unemployment staying close to a half-century low.

It’s small wonder, therefore, that the prospect of the U.S. central bank’s first easing in more than a decade has stirred trepidation among traders, since it’s unclear what happens next. While markets have been priced for lower interest rates for much of the year, traders have struggled to read the Fed’s signals.

In contrast to June, trading volume last week was even more tepid than it usually is in the middle of the U.S. summer, and traders -- suffering from low conviction -- have been stepping out of the fray even while their dovish bets look set to be rewarded.

“It’s extremely unlikely that any of the data is really going to change the narrative very much ether way,” said Thomas Simons, senior money market economist at Jefferies LLC.

On the likelihood of another cut beyond July, he said, “we don’t think that it’s necessarily appropriate, but we’ve moved away from thinking about what the Fed should do and trying to now just look at what the Fed is going to do.”

The market is indicating that the central bank will deliver at least a 25-basis-point cut on Wednesday. But the Fed can meet that expectation and still come off as hawkish, sending yields higher. Traders will want their “ounce of prevention” -- as Chairman Jerome Powell has described a modest easing -- with a dovish chaser, such as an assurance that more cuts will come if needed.

Some observers also expect the Fed central bank to stop shrinking its balance sheet this month rather than waiting until September, as previously announced. While this move wouldn’t have much immediate impact on the broader market, it would end an element of policy tightening might appear on the surface to be incongruous with rate cuts.

The main risk to current positioning is the possibility of a 50-basis-point reduction. That’s kept traders across the front end of the curve on edge and extremely sensitive to recent Fed speeches and press reports.

Futures and options volumes in the eurodollar market dropped below recent averages over the past few days, with one player pocketing gains on a bullish wager early last week to lighten risk over the July decision. But bets on bold action from the Fed were still trickling in, with a fresh trade midweek targeting a half-point easing by September.

The exception to last week’s subdued trading was a flurry of activity on Thursday, which saw selling of bonds on both sides of the Atlantic after the European Central Bank sounded less alarmed about the economic outlook than some had expected. That helped lift Treasury yields, with the two-year rate ending last week at 1.85% and the 10-year at 2.07%.

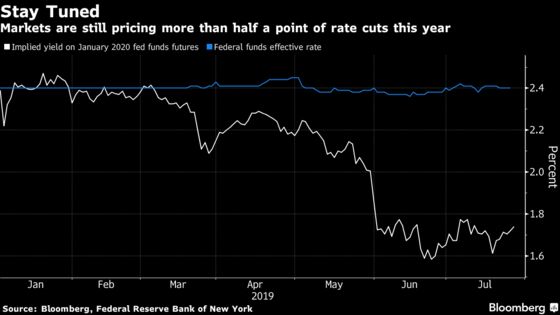

U.S. central bankers won’t have missed the message from this episode: that market expectations are high and easily disappointed. Bets on easing in the second half of 2019 have come off a little last week, but fed funds futures are still priced for the policy rate to fall 66 basis points this year.

For his part, Simons reckons the Fed could be headed for another modest cut in September, but “the market is over its skis a little bit on expectations for central banks globally at this point.”

What to Watch This Week

- The main focus will be on the Federal Open Market Committee decision due Wednesday, although the Bank of Japan and Bank of England are also holding policy meetings this week, and the U.S. will resume trade talks with China.

- Here’s the economic calendar:

- July 29: Dallas Fed manufacturing activity

- July 30: Personal income and spending; PCE deflator; S&P CoreLogic home prices; pending home sales; Conference Board consumer survey

- July 31: MBA mortgage applications; ADP employment change; employment cost index; MNI Chicago PMI

- Aug. 1: Challenger job cuts; jobless claims; Bloomberg consumer comfort; Markit U.S. manufacturing PMI; ISM manufacturing survey; construction spending

- Aug. 2: Jobs report; trade balance; factory orders; University of Michigan sentiment

- And the Treasury auction schedule:

- July 29: $36 billion of three-month bills; $36 billion of six-month bills

- Aug. 1: 4- and 8-week bills

To contact the reporters on this story: Emily Barrett in New York at ebarrett25@bloomberg.net;Edward Bolingbroke in New York at ebolingbrok1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker

©2019 Bloomberg L.P.