Bullish Shipping Analysts Don’t Care About the Threat of Trade Armageddon

Bullish Shipping Analysts Don’t Care About the Threat of Trade Armageddon

(Bloomberg) -- Who cares about the threat of a global trade meltdown? Not shipping analysts tracking prices for moving everything from oil to crops, it seems.

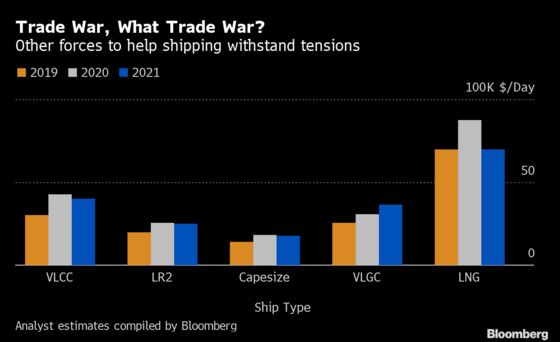

Across every type oil, gas, coal, iron ore and grain-carrying vessel, industry analysts surveyed by Bloomberg are expecting the rates ships earn to jump sharply next year.

That would be impressive given that an escalating trade war between the U.S. and China is nudging the world economy toward its first recession in a decade. The International Monetary Fund last month lowered its projections for trade growth in 2019 and 2020, having also done so in April.

So why do shipping analysts think the industry can withstand such a hit? One widely-held view is that there’s little of the huge fleet growth that’s dogged freight markets so often in the past. Another is that an industry switch to less-polluting fuel from January could result in fewer ships being available for charter.

The regulations, known widely as IMO 2020, were set out in 2016 by the International Maritime Organization, part of the UN. They were designed to try and cut emissions of sulfur oxides, a pollutant blamed for causing acid rain and linked to human health conditions including lung cancer and asthma.

“The first half of 2019 was bad pretty much across the board for shipping rates,” said Randy Giveans, an analyst at Jefferies LLC in Houston. “2020 is looking much better due to slowing supply growth and the positive impacts of IMO 2020.”

The industry’s mandated fuel upgrade could be bullish for a few reasons. Several thousand ships are going to be fitted with equipment called scrubbers to allow them to keep burning today’s cheaper product. That work is starting to ramp up and will continue well into the first half of 2020. That means fewer vessels for charter.

And those carriers that don’t get the equipment installed look likely to face much higher fuel costs. As such, some may find it uneconomical to continue trading and get demolished, while others could simply sail slower, according to Giveans. Both scenarios would be negative for fleet supply and bullish for freight.

Details Matter

“As an outsider, if you are a generalist, if you are reading the press, it’s only bearish,” said Frode Morkedal, an analyst at Clarksons Platou Securities in Oslo. “You would have to look at the details which are quite attractive. It’s a supply driven environment. Nobody has been ordering ships for a while.”

Along with analysts at Evercore ISI., Deutsche Bank, and Fearnley Securities, Morkedal also said IMO 2020 will be supportive of rates.

Whether slow fleet growth and a new fuel will really be enough to overcome a serious hit to trade and the global economy is another question. Several analysts’ central assumption is that demand could be eroded, but that there shouldn’t be a significant contraction in the amount of cargo.

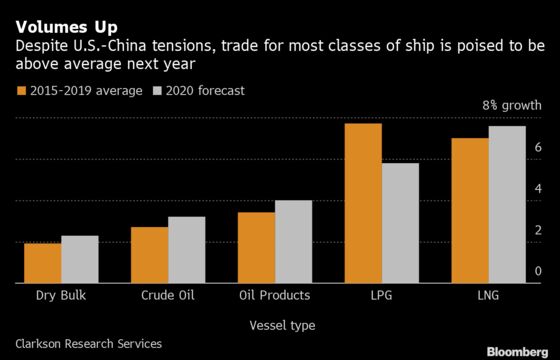

Clarkson Research Services Ltd., a unit of the world’s biggest shipbroker, is estimating that growth in demand for ships will largely outstrip fleet expansion next year. An exception is container shipping, where both demand and vessel supply will increase by 3.3%.

“With order books close to historical lows in commodities shipping we are constructive on the outlook despite the trade tensions,” said Jo Ringheim, an analyst at Arctic Securities A/S in Oslo. “We also remain upbeat for oil tankers due to increased long-haul Atlantic basin exports, a manageable order book, and the anticipated IMO 2020 impact on oil demand and vessel supply.”

--With assistance from Brendan Murray.

To contact the reporters on this story: Firat Kayakiran in London at fkayakiran@bloomberg.net;Timothy Abington in London at tabington@bloomberg.net

To contact the editors responsible for this story: Alaric Nightingale at anightingal1@bloomberg.net, John Deane

©2019 Bloomberg L.P.