Tough Test Looms for Russia's Sanctions-Plagued Central Bank

Tough Choice Looms for Russian Central Bank Plagued by Sanctions

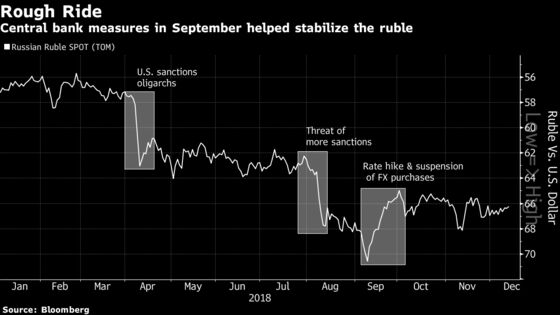

(Bloomberg) -- Markets have stabilized since Russia’s central bank delivered a surprise rate hike in September, but with inflation rising and the risk of new U.S. sanctions looming, Governor Elvira Nabiullina faces a fresh test when she delivers her next move on Friday.

The central bank has added to the complexity by promising to announce closely watched plans for resuming billions of dollars in foreign-currency purchases on Friday as well. All the moving parts have analysts the most split they’ve been in months on the regulator’s next move.

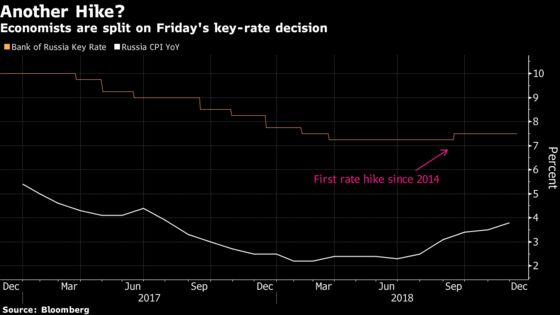

Most economists surveyed by Bloomberg -- 26 of 42 -- forecast the central bank to keep the rate at 7.5 percent, with the rest seeing a quarter-point hike. The last time there was such a split was in June, when the regulator left the rate unchanged amid expectations of a cut.

Some see the relative market calm leaving room for holding the rate even if Nabiullina goes ahead with plans to restart buying next month, potentially hitting the ruble. Others argue that rising inflation, sanctions fears and pressure on the currency mean another protective hike -- or even more -- is coming.

“The regulator faces a tough choice,” said Valery Vaisberg, the head of research at Region Group in Moscow, one of just two analysts who correctly forecast a reverse in policy in September. “Hiking by 25 basis points and keeping a hawkish tone would help protect the Russian currency.”

Nabiullina has sent mixed signals since the first rate increase in almost four years, saying that while that move wasn’t the start of a tightening cycle, the regulator will be choosing between a hike and a hold Friday.

This time, with a value-added-tax hike next month expected to boost inflation and fears that the U.S. could impose new sanctions, some analysts say another hike or even two by the spring will be needed to control the damage.

“Inflation is climbing to the upper end of the central bank’s forecast and inflation expectations are rising and the situation will only get worse with the value-added tax increase next year,” said Liza Ermolenko, an economist at Barclays in London. “Most likely, the central bank will raise the rate to send a signal to the market that inflation expectations remain a priority.”

| What Our Economists Say... |

| “The Bank of Russia is ready for a hurricane, but the storm doesn’t look quite as bad as feared. We expect the central bank to leave the key rate unchanged, without softening its hawkish stance.” --Scott Johnson, Bloomberg Economics |

Annual inflation accelerated to 3.8 percent in November, creeping closer to the central bank’s 4 percent target, and the regulator estimates it could rise further this month before peaking at 6 percent when the VAT increase kicks in. Tough new sanctions under consideration that hit sovereign-debt issuance could push that even higher.

The central bank’s plans for FX buying add more uncertainty. Nabiullina last month suggested the purchases -- suspended in August as the ruble came under pressure -- are likely to resume in January. Analysts are divided on how much pressure the billions in buying for the central bank’s reserves will put on the ruble. Morgan Stanley said the regulator could start slowly, initially doing only half the daily volumes mandated under a budget rule aimed at insulating the ruble from volatility in oil prices.

“We see decisions on rates and foreign-currency purchases as interrelated,” Morgan Stanley economist Alina Slyusarchuk wrote in a research note. “The more actively the central bank comes back to the foreign-currency market, the more hikes it would need to deliver.”

But others say that to really protect the ruble, it would take more tightening than the central bank could stomach amid current weak growth. The currency has advanced 0.9 percent this month, but is still on track to post a more than 13 percent drop for the year.

“It’s like drinking your favorite coffee without a cover in a moving car: to enjoy, you either take a big gulp (hike decent and fast) or slow down the speed (cut volatility),” something the central bank doesn’t have the levers to do amid sanctions uncertainty, Dmitry Polevoy, chief economist at the state-run Russian Direct Investment Fund, wrote in a note.

--With assistance from Zoya Shilova.

To contact the reporters on this story: Anna Andrianova in Moscow at aandrianova@bloomberg.net;Natasha Doff in Moscow at ndoff@bloomberg.net

To contact the editors responsible for this story: Gregory L. White at gwhite64@bloomberg.net, Tony Halpin

©2018 Bloomberg L.P.