A Little Hostility Is Just What Japanese Tech Needs

(Bloomberg Opinion) -- “I’m not selling,” says the chairman of one of Japan’s biggest technology companies.

Let me grab some popcorn and a ringside seat for what I hope will be a hotly contested bidding war. Japan’s tech sector is ripe for further mergers and acquisitions. But the rarity of hostile takeovers means most deals feel like they’ve been hammered out over a polite lunch.

This one could be different.

Toshiba Corp. already owns 52.4% of electronics-manufacturing equipment maker NuFlare Technology Inc. But Toshiba wants it all, so last month it made a public tender offer for the rest at 11,900 yen per share, a premium of around 49% above its 50-day moving average. Toshiba Chief Executive Officer and Chairman Nobuaki Kurumatani probably figured that his 65 billion yen ($596 million) offer was a formality. He announced two other buyouts at the same time.

Then along comes rival Hoya Corp., a Japanese supplier of materials used in electronics production. Last week, it launched its own unsolicited bid for NuFlare, offering 8.4% more than Toshiba had.

So after what looked like a rubber-stamp deal, Toshiba’s Kurumatani is now faced with a possible bidding war with a gadfly rival. And he’s digging in his heels, as Bloomberg’s Pavel Alpeyev and Yuki Furakawa describe it after interviewing him this week.

“Price is not the issue — it’s life or death” for NuFlare, he told them.

Of course, price is the issue. At least, it should be.

Hoya’s offer for NuFlare, at just 1,000 yen higher than Toshiba’s, barely seems serious.

But its announcement did have the effect of pushing NuFlare’s stock 13% higher as investors speculated Toshiba might need to offer more. Such a price battle is great news for those NuFlare shareholders who aren’t named Toshiba. It’s also good for the broader Japanese market.

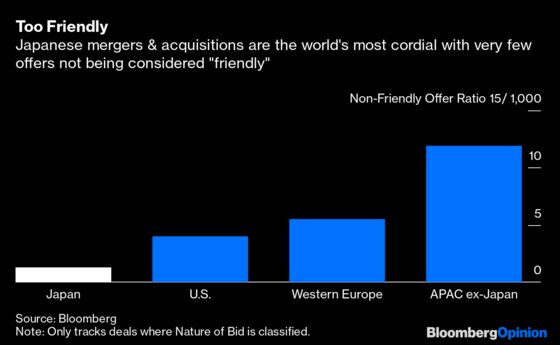

Out of more than 3,100 M&As of Japanese firms tracked by Bloomberg in the past five years, only four are classified as “unsolicited.” The rest were considered “friendly.” None were “hostile.” That contrasts with 137 of more than 34,500 U.S. deals that were not considered friendly. In other words, the rate of unfriendly offers in Japan is less than one-third of that in the United States.

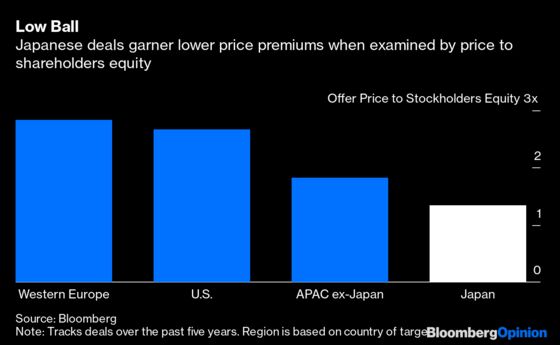

The result for deal values is palpable. U.S. mergers and acquisitions over the past five years had a median transaction price of 2.67-times stockholder equity, double the 1.34 in Japan. Using another metric, the deals bid a median of 2.79-times book value versus 1.39. Kurumatani is probably aware of these statistics. He’s a former banker, brought in to revive Toshiba after it lost billions of dollars in a nuclear energy project.

Three years ago, a deal spree in Japan had me advocating for more mergers. The nation is home to world leaders in chemicals and equipment, crucial parts of the technology supply chain. Yet many need to bulk up in preparation for greater competition, especially from China, if they’re going to avoid the government bailouts and foreign buyouts that have been hallmarks of the past decade.

Toshiba taking over NuFlare isn’t necessarily a bad thing, but it’s somewhat meaningless when you consider that it already holds a majority of the target. A more innovative move would be for the company to widen its scope and broaden its capabilities — rare earths and new materials come to mind, given their increasing importance in new technology and gadgets.

By facing a hostile competitor, maybe Toshiba won’t take its existing portfolio of companies for granted and will instead be prompted to look further afield for places to spend its money.

Hoya’s bid might not go far since Toshiba is in control and won’t sell, but we should hope that the gumption it’s shown will inspire other companies to make unsolicited bids. Even if Hoya fails this time, at least NuFlare shareholders will get a higher price while investors may be prompted to look for other possible takeover targets and raise bidding.

Japan is sitting on some great companies. We just need a bit of fireworks to make them shine.

This search only includes deals for which a Nature of Bid was classified.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.