Too Cheap to Ignore, Emerging Dollar Bonds to Fly With Fed

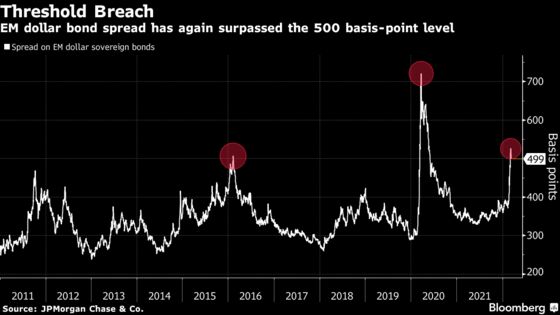

The extra yield offered by developing-nation sovereign debt over U.S. Treasuries has risen above 500 bps, crossing a threshold.

(Bloomberg) -- Emerging-market dollar bonds are starting to look like a bargain.

The extra yield offered by developing-nation sovereign debt over U.S. Treasuries has risen above 500 basis points, crossing a threshold breached only two other times in more than a decade. That’s drawing money managers including FIM Partners and Vontobel Asset Management to bet spreads will quickly tumble, just like they did following the previous spikes.

As the Federal Reserve prepares to raise interest rates this week, investors are searching for assets that can outperform amid tighter monetary conditions and a strengthening dollar. Emerging-market bonds denominated in the U.S. currency seem to fit the bill, and have a history of rallying during Fed hikes. While a worsening war in Ukraine -- or fallout from a Russian debt default that’s possible as soon as Wednesday -- may still derail this trade, a fear of missing out on a market bottom is pushing investors to selectively load up on the securities.

“Emerging-market spreads have never finished a calendar year with a negative return when starting above 300 basis points,” said Francesc Balcells, chief investment officer of emerging-market debt at FIM Partners in London. “There is a lot of negativity priced into the debt at the moment.”

A JPMorgan Chase & Co. measure of sovereign-risk premium in emerging nations rose to 526 basis points on March 8. That’s higher than the 507 basis points hit after the Fed’s 2015 rate hike, and the 468 basis points reached in 2011 after the U.S.’s credit rating was downgraded. On both occasions, a bond rally ensued, cutting the spread on developing debt to about 250 basis points. A surge during the Covid-related rout of March 2020 was also followed by gains within weeks.

EM Weekly Podcast: Fed Hike; Russia Bond Deadline; Brazil Rates

FIM Partners has started buying debt issued by countries in the Gulf and Latin America and is looking at beaten-up high-yielders such as Oman. The asset manager will also invest in new debt offerings from junk-rated Bahrain and Colombia that will “come with big concessions” to their existing debt, Balcells said.

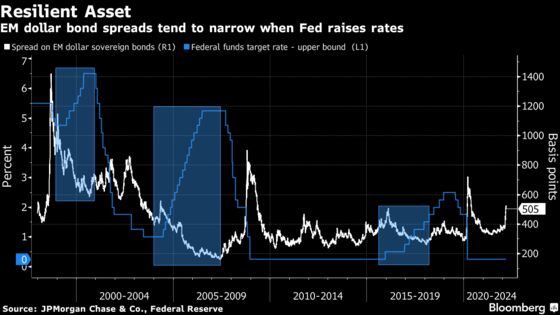

Adding to the bullish sentiment, history suggests emerging-market dollar debt tends to rally once Fed hikes get underway as it offers investors a way to own higher-yielding assets without local-currency risk.

“A tightening of emerging-market hard-currency spreads is likely once the Fed begins to hike, as it has occurred in the last three hiking cycles,” said Carlos de Sousa, a money manager at Vontobel.

Selective Bets

But cheapness alone isn’t enough to sustain investor interest in emerging-market assets, particularly when a raging war threatens to boost inflation and sink global growth. Goldman Sachs Group Inc. said it’s premature to buy Asian credit now despite a decline, given the potential for a wide range of outcomes from Russia’s invasion of Ukraine.

Developing-nation dollar bonds posted an annual loss in 2013 when the taper tantrum sparked a capital flight, and when the 2018 trade dispute between the U.S. and China hurt demand for risk assets. This year, emerging markets are facing a combination of both Fed tightening and a geopolitical flare-up. Their dollar debt has lost almost 12% this year, according to data compiled by Bloomberg.

“If Ukraine is somehow resolved, then the Fed can return to center stage,” said Guido Chamorro, co-head of emerging-market hard-currency debt at Pictet Asset Management. “In that scenario, the first or second hike could signal a good entry point for emerging markets.”

Money managers that are dipping back into the asset class have turned selective, favoring longer-maturity bonds that are less sensitive to higher rates or the debt of countries benefiting from the commodity boom.

Vontobel’s de Sousa prefers Ecuador because crude prices around $110 a barrel reduce the nation’s need to tap overseas capital markets. Bank of Singapore is advising clients to buy 30-year bonds and sovereigns that are net energy and commodity exporters, according to Todd Schubert, its head of fixed-income research.

Still, for Avenue Asset Management, which has started buying debt in the single B credit-rating category, the potential rewards are worth the headline risk.

“Emerging-market dollar bonds look pretty attractive at the moment,” said Carl Wong, the company’s head of fixed income.

Here’s what to watch in emerging markets this week:

- Russia is due to make a $117 million coupon payment on dollar bonds on Wednesday, with a failure to pay starting a potential wave of defaults; the central bank is also due to leave its key rate on hold this week

- China’s activity data will give a steer on the economy’s trajectory in early 2022, with production growth estimated to rise in the first two months of the year

- Brazil’s central bank is expected to deliver on its pledge of a slower pace rate hike on Wednesday and policy makers may adjust the tone of their communication based on how the war-driven surge in oil prices may impact the country’s growth outlook

- Turkey will likely keep interest rates unchanged on Thursday

- In Chile, fourth-quarter GDP growth will add evidence of the strong recovery in 2021 and show robust consumption, increasing net exports, and waning investment

©2022 Bloomberg L.P.