Today’s Dirty Utilities May Be Tomorrow’s ESG Winners

(Bloomberg Opinion) -- One way to think about the ESG thing is in religious terms: Proselytizers target heathens, not the saved.

Environmental, social and governance investing today enjoys more hype than clarity. There is no agreement on exactly what counts as a compliant investment, and there is often a lack of clear economic signals tied to ESG-favored outcomes (elusive carbon pricing is a prime example). Does it make sense to invest in a company that’s already ticked a lot of ESG boxes or one that could yet do so? And how to be rewarded?

U.S. utilities can thread this needle. Greenhouse-gas emissions from the power grid have fallen by more than a quarter since 2007, but much remains to be done. Moreover, utilities earn a regulated return on investment in new stuff, so there are quantifiable gains to be made on greening their asset base.

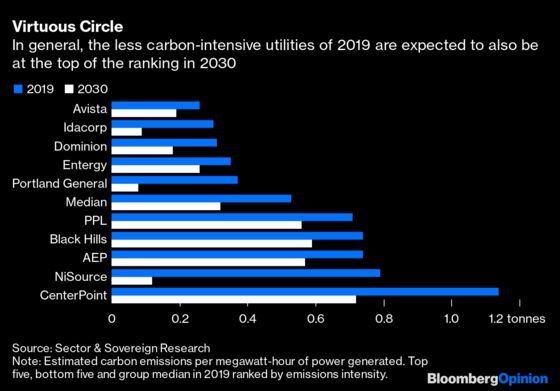

Hugh Wynne and Eric Selmon, utilities analysts at Sector & Sovereign Research, have benchmarked this opportunity for 25 companies with a collective market cap of more than $600 billion. Their starting point is the carbon intensity of electricity generation in tonnes per megawatt-hours, both in 2019 and estimated for 2030, as implied by the companies’ decarbonization targets. In estimating that, they assume the utilities replace their highest-emitting plants (running on coal, oil or natural gas, in that order) with renewable generation at an average cost over the next decade of $1 per watt for solar power and $1.50 for wind.

One immediate observation is that the utilities that score better in terms of having low carbon intensity in 2019 also tend to be at the top of the table in 2030.

You might think that makes them a shoo-in for ESG investors. But addressing climate change quickly means removing the highest-intensity sources of emissions first. Surely it makes at least as much sense to invest in companies that are big emitters now but have committed to fixing that — and need capital in order to do so. Bonus: As utilities, they have a chance of getting those investments into their regulated asset base.

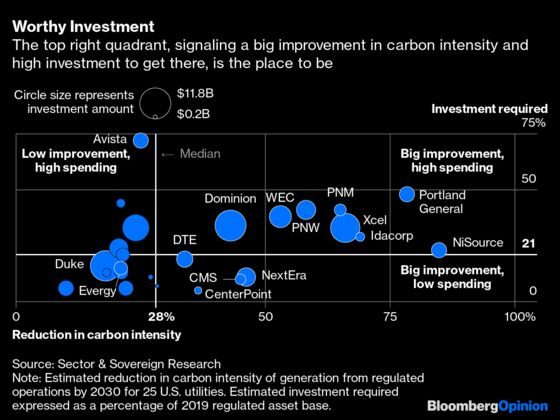

Rather than looking at absolute virtue signals, consider who is moving furthest and likely to spend big to get there.

Utilities with nuclear plants — usually larger companies — or hydroelectric generation tend to score well on carbon-intensity already. Those that don’t, and which have more room for improvement, tend to be smaller utilities in the Midwest and West with significant coal-fired and other fossil-fuel generation capacity.

As estimates built on objectives, these numbers aren’t set in stone. The added wrinkle is that regulators may not necessarily let utilities put investments in new capacity into the regulated asset base, but force them to contract power in competitive auctions. That would limit the overall opportunity versus the dollar amounts in the chart, although the environmental goal would still be met.

Apart from ESG investors, the chart makes a useful screen for utilities themselves; ones looking to buy other utilities, anyway. Big investment requirements, particularly tied to a secular theme like renewables, make the best targets. PNM Resources Inc., the New Mexico utility that appears in that upper-right quadrant, is already the subject of a $7.6 billion agreed acquisition by Spanish renewables giant Iberdrola SA, due to close next fall.

It is interesting to note Duke Energy Corp. and Evergy Inc. — both reportedly considered as targets at some point by NextEra Energy Inc. — screen low in terms of targeted cuts to emissions intensity. While that makes them potentially less interesting for an ESG portfolio, the potential to come in and execute a more ambitious decarbonization plan may make them interesting for NextEra.

Regulators are another audience. By Wynne’s and Selmon’s calculations, the average cost of carbon abatement across the 25 utilities is just $19 per tonne, with a range of $13 to $37. Even if these costs do not reflect spending on associated wires and other infrastructure, they suggest further decarbonization is affordable across the states.

The marginal cost rises as the highest-intensity sources are taken out; another reason to target these first. So as those costs rise, particularly as energy storage is incorporated to squeeze out gas-fired peaker plants, regulators should think more broadly. For example, with transportation now the biggest source of emissions in the U.S., it may make sense to steer utilities’ investment budgets toward lateral efforts like vehicle-charging infrastructure once their generation portfolios have decarbonized to a certain point. Either way, the ESG crowd should give their blessing.

—With graphics assistance from Elaine He.

These are unsubsidized prices. The exact mix of solar and wind assets is determined either by published targets or the cheapest option depending on that utility's service territory. For the group, the analysis resulted in a split of 70% solar and 30% wind for the new generation capacity. The analysis does not include estimates for the spending required on new transmission or distribution infrastructure.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2021 Bloomberg L.P.