Robots Conquered Stock Markets. Now They’re Coming for Bonds and Currencies

E-platforms can drive out traders by: they require fewer humans to make deals, and they require new skills from those who remain.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- Ashok Krishnan’s colleagues at Bank of America initially brushed off his pitch to automate trading. He recalls how some barely acknowledged him in the halls. But before long their aversion gave way to requests for help.

As head of electronic trading in the bank’s global markets division, Krishnan is among a group of Wall Street equities veterans -- including Phil Allison at Morgan Stanley and Mark Goodman at UBS Group AG -- promoted in recent years to take on a delicate assignment: Build machines to handle trading in other markets such as bonds and currencies. They’re convinced it’s possible after watching computers take over stocks.

In an interview at Bank of America Corp.’s headquarters in New York, Krishnan, 48, ticked off technologies such as algorithmic and mobile trading that are giving machines a greater role in making complex markets.

Persuading humans is something else.

The long-predicted automation of bond and currency trading has been slow to arrive, after traders voiced skepticism that happened to protect their business and jobs. They argued clients want to talk through complex transactions and that automation weakens relationships. Even shifting simple bets to electronic platforms would reduce interactions with customers, missing opportunities to arrange other deals and “cannibalizing” the business. Yet investors are demanding more advanced platforms to cut costs, as well as new tools providing a clearer view into markets.

“If you don’t do this, your P&L goes down because the client just does business somewhere else,” Krishnan said, invoking a Wall Street acronym for earnings.

The stakes are huge for Wall Street banks competing in the $22 trillion market for U.S. Treasuries and corporate debt and the $5.1 trillion-a-day foreign-exchange market. Handling fixed-income products remains one of industry’s biggest revenue generators. Now firms must disrupt the old model by building out their electronic platforms, or they risk getting sidelined in the future.

Equities migrated to computers first because they’re standardized and trade frequently, making it relatively simple to match buyers and sellers. The same goes for parts of bond and FX trading, such as Treasury futures and spot currency transactions. That’s left stock veterans with the technical experience to tackle more-complex products -- as well as the confidence needed to overcome years of resistance.

“It started with the equity guys saying, ‘Let’s make these markets look like our markets,”’ said Kevin McPartland, head of research for market structure and technology at consultant Greenwich Associates. “From the bond side it was: ‘No, no, no. I’ve been doing this for 20 years. I know my clients. There’s no way you can get a machine to replicate the knowledge I have.’”

Krishnan trained as an electronics and telecoms engineer before becoming a banker. He was running Bank of America’s electronic trading of equities two years ago when his bosses expanded his responsibilities to include fixed income, currencies and commodities. His peers at rival shops are leading similar efforts. Clients, too, are moving in the same direction.

Take Vanguard Group Inc.’s Andy Maack. Formerly an equities portfolio manager, he was elevated in 2013 to build and run a centralized currency-trading desk for the asset manager, which oversees more than $5 trillion. Maack’s expectations are based on his work with stocks: He says banks should offer advanced algorithms that fill orders quickly, cheaply and with extensive trade reporting and analytical tools.

Already, more than 90 percent of Vanguard’s spot-currency deals are handled electronically. Of those, over half rely on sophisticated algorithms, which calculate optimal times, order sizes and venues to trade.

Goldman’s Warning

“I’ve noticed a pretty significant change of behavior over the last five years,” Maack said, noting that even old-school Wall Street traders -- known for their prowess with phones and message systems -- have come to accept computerized processes. “When somebody from equities got involved, the FX desk transitioned faster to electronic.”

It helps that bank leaders have gotten behind the push.

Last year, Goldman Sachs Group Inc.’s chief financial officer, Marty Chavez, told analysts that the old arguments against automation no longer made sense and that the firm was analyzing how traders and salespeople work to automate more processes. Advances in computing power mean machines “can handle that extra complexity,” he said. He was later named co-head of the firm’s trading division.

Electronic platforms can drive out traders two ways: They require fewer humans to facilitate transactions. And they require new skills from those who remain.

Concerns about jobs appear warranted: The world’s 12 largest banks have reduced front-office staff -- those who produce revenue -- by 11 percent from 2013, according to Coalition Development Ltd.

Yet banks have little choice but to adapt. Buy-side investors are embracing new technologies and pressing their market-makers to do it, too, to cut costs and offer more transparency, said Morgan Stanley’s Allison. He oversees fixed-income automated trading from London and previously worked in equities at KCG Holdings Inc. and UBS.

It made sense for the division to enlist a stocks specialist, said Allison, who studied mathematics at the University of Cambridge. “I probably bring a different perspective,” he said. “I’ve managed large groups of people, all the way from high-touch sales traders through to heavy C++ developers.”

He was hired by Sam Kellie-Smith, who previously ran equities trading at Morgan Stanley and now leads the bank’s fixed-income division.

At UBS, Goodman has seen the stock market move from the speed of a fax machine to millionths of a second. Instead of working phones, traders now create algorithms to slice, time and route orders. He’s working on a similar push for FX, rates and credit desks. For Goodman, who practices kung fu in his free time, embracing technology has been a good career strategy.

“I took a risk,” Goodman said. “You get an opportunity to do something new. And if that eventually replaces the old, then you have an opportunity to really expand your career, rather than following what is a well-trodden path.”

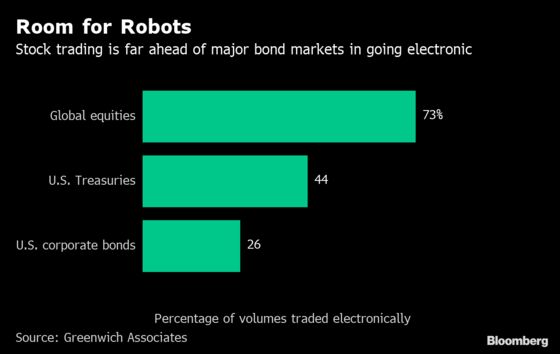

In the most liquid equity markets, more than 90 percent of trades are executed electronically, according to estimates from Greenwich Associates. That compares with 79 percent in global foreign exchange, 44 percent in U.S. Treasuries and 26 percent in U.S. corporate bonds, with the most room for growth in the latter two markets, according to McPartland at Greenwich.

“People say, ‘This market can’t be electronified, it’s different,’” he said. “That doesn’t hold water anymore.”

--With assistance from Sonali Basak, Alexandra Harris and Molly Smith.

To contact the reporter on this story: Lananh Nguyen in New York at lnguyen35@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, ;James Hertling at jhertling@bloomberg.net, David Scheer, Dan Reichl

©2019 Bloomberg L.P.