Three Megacaps Give the Market an Early Xmas Gift: Taking Stock

Three Megacaps Give the Market an Early Xmas Gift: Taking Stock

(Bloomberg) -- S&P futures are staging a very slight recovery after one of the worst two-day performances since October. Things may have gotten so bad (some are now comparing the fourth-quarter selloff to the Great Depression and Pearl Harbor!) that we may be setting up for an oversold bounce, which would give the bulls something to cheer about, however many of them are left.

One of the more cautious equity strategists alluded to this earlier in the week: Morgan Stanley’s Mike Wilson, in discussing the many signs investors were giving up on equities, found that as expectations for 2019 become more realistic, the groundwork may be "finally" setting up for rally.

So the futures action is tenuous, and obviously nowhere near a level that anyone should call an "all clear," especially after seemingly every bounce last week got sold hard. But three megacaps may have just given the markets an early present.

Three Big Presents

The action overnight may be just what Santa Claus needed to work up that rally bulls have been waiting for what seems like forever. Oracle shares are up ~6% after delivering on results and outlook, which may help provide a boost to the rest of tech -- that’s a good sign as that space was responsible for the lion’s share of Monday’s selloff, with 94% of tech names lower, including Micron which is expected to report later today and set a fresh 52-week low yesterday.

Boeing and Johnson & Johnson also rode to the rescue with $25 billion in repurchase authorizations (Boeing boosted their program to $20 billion from $18 billion and raised the dividend while JNJ approved a $5 billion buyback), giving investors that nod that the companies may feel their equities are undervalued.

Given that JNJ was a major part of the weakness in the S5HLTH index over the past two days, a slight uplift may be enough to stem some of the bleeding. Screens were red across the spectrum, with no safe sector besides gold.

No Safe Havens

A true fear trade was in place with money flowing to the Swiss Franc and Japanese Yen. The most defensive sectors in the market, like utilities, health care and staples, were among the hardest hit as investors sought to sell whatever winners they may still hold. Deutsche Bank wrote that weekly sentiment showed the highest bearish reading since 2009 in describing "record inflows" to money markets and out of equities and credit funds.

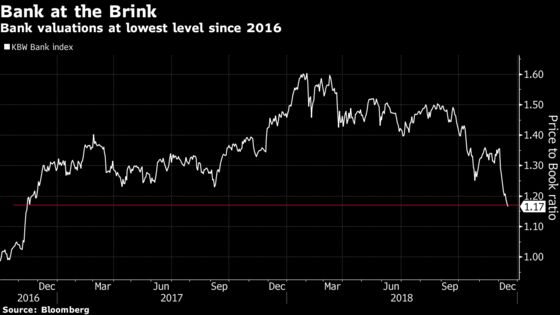

If there were any winners, it would have to be the banks, which were resilient in the face of ominous Goldman Sachs 1MDB scandal headlines and declining treasury yields. The worst performer over the past month, its possible some of the money from the Obamacare ruling-related healthcare selling found its way to the underperforming financials, which is scraping the bottom of historical valuations.

But for banks, the story will still be the FOMC meeting, which gets underway today and concludes with the decision Wednesday where market participants can read the tea leaves on whether growth is a real concern, or whether "financial conditions" (read: stock market and credit) are such to warrant a pause in the interest rate hike cycle sooner than expected.

Trump renewed his criticism of Fed policy on Monday (his ~13th such attack), appealing for a pause, though this time he had a chorus of voices echoing similar sentiment in Druckenmiller/Warsh’s WSJ piece and Doubleline’s Gundlach.

But Its Still About Growth

Its hard to completely ignore the growth narrative as the rationale for the underlying equity market weakness, even just taking a one day sample of the two paltry data points we had to work with Monday: 1) the regional Empire manufacturing data, which came in at the lowest since May 2017, and 2) the NAHB data, which was the lowest level since 2015 while missing estimates.

The NAHB figures are notable in that the two month decline was the worst since 2001, or well before the housing crisis. That puts an exclamation point on the ongoing travails in the sector we’ve recounted since the fall months. That said, homebuilder stocks like Toll Brothers and Lennar fell less than the market on Monday, perhaps in a sign there’s only so much further they can fall. Housing starts data is due at 8:30 a.m. in New York.

But I have to agree that discussion itself over growth risks becoming a self-fulling prophecy, as my colleague Cameron Crise wrote yesterday, after citing data that Google queries about a "U.S. recession" have hit their highest level since the end of 2009.

That may fly in the face of data, as just last week Goldman Sachs joined JPMorgan in saying the growth concern was overdone. Monday’s superlatives on the market action make that a tougher pill to swallow, but FedEx results today post-market may help provide a glimmer into the health of the economy, despite Amazon.com competition concerns analysts are so quick to discuss. That Amazon headwind could be part of why the quarter’s earnings are primed to be some of the most volatile in years (FDX options are pricing in a near 6% move compared to its average 3.5% around earnings).

Commercial vehicle manufacturer Navistar just reported, and at least the signals there for trucking demand are strong as the top line views for 2019 beat analysts forecasts.

Damage Is Done

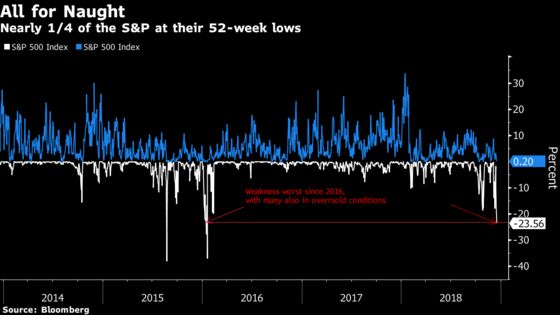

But whatever the narrative, the S&P 500 unleashed a world of pain on any last thread of technical support Monday, setting fresh intraday and closing lows for 2018. This followed a break of the November closing lows Friday, and as BMO’s Russ Visch put it, there may be a “rush for the exits,” and “a move to 2,445 makes a lot of sense to us.”

The internals told most of the story with a fifth of each of the 3 major gauges setting new 52-week lows, which isn’t surprising considering the S&P was at its lowest since October. That’s the largest proportion for the S&P since January of 2016. Not only that, but a fifth of the S&P 500 was technically oversold, as defined as below the 14-day RSI value below 30, the most since the late October selloff.

The deep selling Monday put strategists on course to miss their 2018 targets by the most since the financial crisis, according to data compiled by Bloomberg. They may need a Christmas miracle to get that on track.

Notes From the Sell Side

Two cautious Tesla notes out this morning: 1) Morgan Stanley’s Adam Jonas sees fourth quarter marking an "emerging peak" in sentiment and potentially for the shares, and 2) Goldman’s David Tamberrino reiterated his sell rating as he expects a "lull in demand" starting in the first quarter that may not be fully made up by initial deliveries across Europe.

Credit Suisse slashed Philip Morris to an underperform (shares down ~2% already), which makes it the second bank out of 21 that has an equivalent sell rating on the stock. While negative on PM, the note actually reads cautious on the global tobacco sector following a proprietary survey of next-generation products users in Japan, the U.S. and the U.K.

And two big sector notes out from Morgan Stanley, one on the electrical equipment and multi-industry sector with a boatload of rating changes (Illinois Tool Works, Flowserve, and Grainger are all underweight now while Fortive and Ametek are overweight) and another upgrading the midstream energy sector to an attractive view (favors Energy Transfer and Williams Companies).

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- IPO lockup expiry: IIIV, APTX, MGTA, AVRO, EPRT, KZR, XERS

- 7:00am -- DRI, FDS earnings

- 8:00am -- BNFT investor day

- 8:30am -- Housing Starts

- 8:30am -- AGCO investor meeting

- 8:30am -- DRI earnings call

- 9:00am -- NAV earnings call

- 9:11am -- SpaceX launch is scheduled

- 10:10am -- Galaxy Investment CEO Mike Novogratz on Bloomberg TV

- 11:40am -- Gamco CEO Mario Gabelli on Bloomberg TV

- 12:00pm -- CBIO research & development day

- 4:01pm -- MU, AIR earnings

- 4:05pm -- JBL earnings

- 4:15pm -- FDX, ABM earnings

- 4:30pm -- API oil inventories

- 4:30pm -- MU, JBL earnings call

- 5:30pm -- FDX earnings call

- 11:00pm -- The Boring Company tunnel unveiling

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editor responsible for this story: Arie Shapira at ashapira3@bloomberg.net

©2018 Bloomberg L.P.