Thomas Cook’s Rescue Tests Reputation of Default Protection

Thomas Cook’s Rescue Tests Reputation of Default Protection

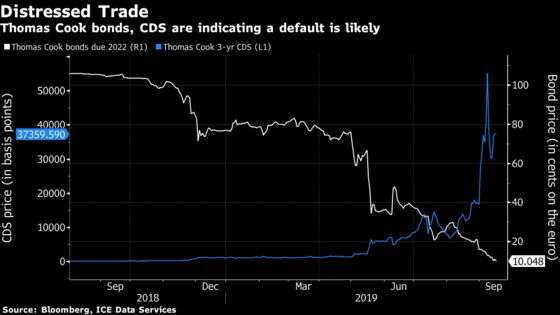

(Bloomberg) -- The $10 trillion market for derivatives that pay out if a company goes bust faces a test of its credibility as U.K. travel agent Thomas Cook Group Plc heads toward a $1.1 billion rescue.

Thomas Cook filed for Chapter 15 bankruptcy protection in the U.S. on Monday as part of a broader debt restructuring. But the filing stopped short of stating the company is insolvent, an ambiguity that means hedge funds holding credit-default swaps insuring Thomas Cook debt may not get their money.

Investors holding the swaps are already battling against a technicality in the terms of Thomas Cook’s planned debt restructuring that threatens to make their CDS holdings worthless. The rescue centers on converting Thomas Cook debt into equity, which leaves the swaps with no bonds to insure.

“Buying insurance against a default and then being unable to claim when the company does actually default defeats the point of having it,” said Henry Craik-White a portfolio manager at Wells Fargo Asset Management in London. “It makes a mockery of the product.”

CDS contracts pay out when a Determinations Committee of swaps traders decides that a company running into difficulty and failing to keep up with its debt obligations constitutes a so-called credit event.

The hedge funds holding Thomas Cook CDS are threatening to scupper the rescue plan, which is led by China’s Fosun Tourism Group, by blocking it at a creditor meeting later this month. If that maneuver is successful, it could also challenge the reputation of the CDS market.

Regulators are already eyeing the derivatives market for so-called manufactured credit events, when funds entice companies to miss bond payments they could otherwise make. Even the Pope has linked the swaps to “extremely immoral actions.”

“Once a company gets close to a credit event, CDS protection buyers have a serious incentive to make sure the swaps get triggered,” said Mahesh Bhimalingam, senior European credit strategist at Bloomberg Intelligence. “It can encourage some activity that feels like abuse of power or market manipulation to outsiders.”

Sona Asset Management, one of the hedge funds seeking a payout on Thomas Cook swaps, made money on a similar trade earlier this year involving retailer New Look. Sona was able to ensure New Look swaps paid out by buying enough of the U.K. fashion retailer’s bonds to influence its debt restructuring.

Asset Rules

Credit protection on banks and sovereigns is easier to settle than on companies because those contracts were updated in 2014 to allow them to pay out even after debt is converted into equity or wiped out.

Thomas Cook’s case may lead to more pressure for those rules, known as “asset-package delivery” to be applied to corporate CDS.

“If only the asset-package delivery rule applied to European corporates as well, there wouldn’t be this problem,” said Soren Willemann, a Barclays Plc credit strategist.

A spokesman for the International Swaps and Derivatives Association said that any change to the market’s rules will require “broad industry consensus and agreement.”

Chapter 15 protection has triggered CDS payments before, for example on Canadian paper company Tembec Industrials Inc. over a decade ago, according to Neill Keaney, an analyst at CreditSights in London. But the precise level of court protection required by Thomas Cook may be deemed insufficient for a credit event, he said.

The Determinations Committee has come in for criticism in the past when traders experienced delays in settling swaps linked to Spanish lender Banco Popular Espanol SA and commodity trader Noble Group Ltd.

“If Thomas Cook CDS doesn’t pay out then there will be inevitable questions over the efficacy of the instrument,” Keaney said. “Arguments will arise again over letter of the law versus spirit of the law.”

To contact the reporter on this story: Katie Linsell in London at klinsell@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Chris Vellacott

©2019 Bloomberg L.P.