This Strange Expansion Might Set Up a Mundane Recession

(Bloomberg Opinion) -- General Motors Co. just announced the closing of four factories in the U.S. and one in Canada. Three of the factories are in Michigan and Ohio — states that voted for Donald Trump in 2016, in part thanks to his promise to bring back American manufacturing jobs. So much for that.

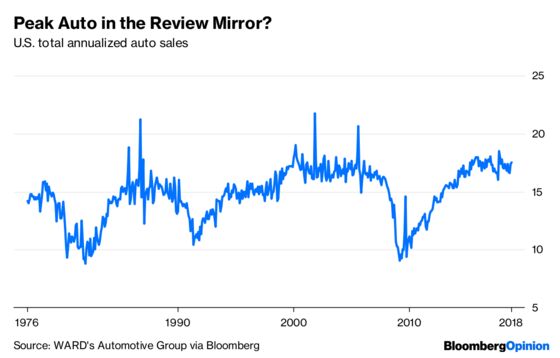

GM has long been a troubled company, requiring a government bailout in the Great Recession and struggling to build popular cars ever since. But the recent plant closures may have a cause that goes beyond GM’s boardroom. Auto sales in the U.S. have declined from their level of three years ago and have taken a considerable drop from their peak in 2017:

And that’s even with gas prices that have fallen significantly in the past few months.

Looking at history, a clear pattern emerges — auto sales tend to rise in the early stage of an expansion, but peak and decline shortly before a recession.

There’s actually a fundamental economic reason why this should be true. Unlike nondurable goods and services such as food, heating and insurance that people have to purchase even in bad times, consumption of durable goods like cars and houses can be delayed. If you’re unemployed, or worried about becoming unemployed, or if sales at your company are bad this year, you can keep driving your old car a little while longer, or put off buying that new condo.

As economists Robert Barsky, Christopher House and Miles Kimball pointed out in a 2007 paper, putting off spending on durable goods is a big part of what triggers a recession. Lower auto and home sales are a consequence of a bad economy, but they also cause the economy to get worse.

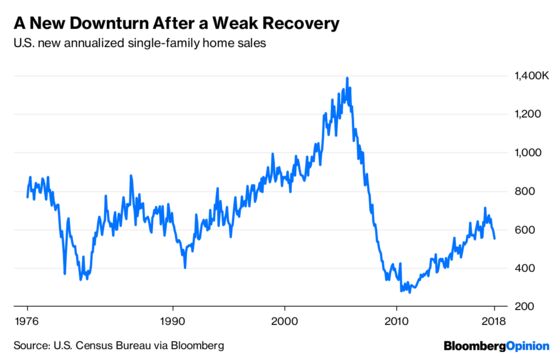

Housing is usually a bigger factor than cars. In another 2007 paper, economist Ed Leamer argued that residential investment is the biggest driver of the economic cycle. He wrote:

Residential investment consistently and substantially contributes to weakness before…recessions…Eight of the ten [U.S. postwar] recessions [before 2007] were proceeded by sustained and substantial problems in housing.

And of course, one year after that was written, the U.S. saw the biggest housing-driven recession of them all.

Housing has been particularly weak throughout the recovery from the Great Recession, probably because Americans bought so many houses before the crash, and also probably because more young people are living longer with their families:

But even from this low level, 2018 has seen a downturn in new home sales. Housing starts are at essentially the same level as 2016.

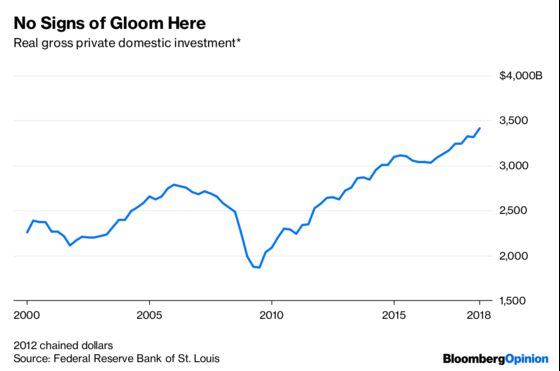

So with auto sales in decline and new home sales low and falling, the economy looks to be on shaky footing. But businesses are still investing enthusiastically:

All of this makes for a very strange expansion. Why is business investment holding up, even as GM prepares to shutter factories and housing falters from already-low levels?

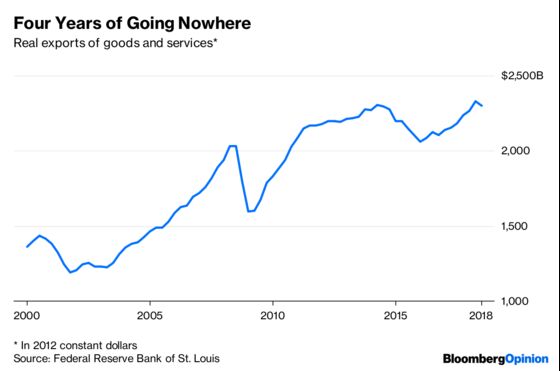

It could be that they’re planning to ramp up exports. But those don’t look particularly strong either:

And with President Donald Trump’s trade war hitting U.S. exports such as gas and agricultural products, there seems to be little reason to expect an overseas sales boom in the near future.

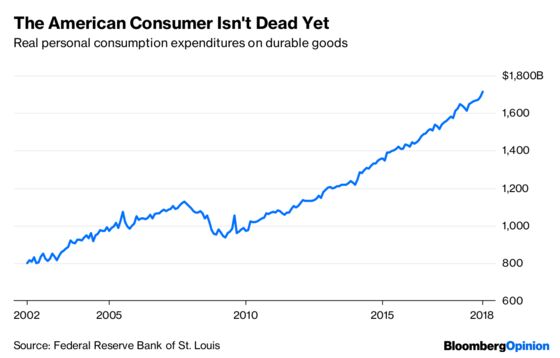

One possibility is that American consumer tastes are simply shifting, as millennials trade cars for smartphones and choose to live with their parents. Overall consumption of durable goods is holding up better than cars or autos:

But another possibility is that the U.S. economy has simply hit the top of the current business cycle, and is headed for a downturn. That’s certainly what Leamer’s paper, with its emphasis on housing over business investment as a leading indicator of recessions, would suggest.

So is a recession coming soon? Some of the pieces do seem to be falling into place. Macroeconomic indicators like term and credit spreads have been looking shaky. Lots of observers have been watching the corporate-debt market, especially BBB-rated bonds and leveraged loans. If consumption falters, corporations that loaded up on risky debt could suffer a wave of defaults. Meanwhile, Trump’s trade war seems to be causing unpredictable and mostly negative effects, as companies find it harder to purchase inputs from overseas, or they run into foreign retaliation.

Thus, a particularly strange expansion may soon turn into a rather typical recession. That would be sad, because it would mean that the biggest trough in 80 years was followed by one of the most underwhelming peaks. That’s a good argument for the Fed to hold off on rate hikes in order to stave off this possibility, and Trump should think twice about continuing his trade war.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.