There Will Be Blood. Apple, FedEx, Who’s Next?: Taking Stock

Let’s recap the travesty that has unfolded over the past couple of days.

(Bloomberg) -- So let’s recap the travesty that has unfolded over the past couple of days.

Apple sucker-punched the rest of tech with its warning that caught everyone by surprise (not the cut itself so much, but the magnitude of it), but they most definitely won’t be the only U.S. company hurt by the trade war.

FedEx showed us this last month just how bad the trade frictions are impacting business, but you can now take White House Council of Economic Advisers chairman Kevin Hassett’s word that it’s going to get worse for a whole swath of companies if we remain at a stalemate:

- "It’s not going to be just Apple," he told CNN

- "There are a heck of a lot of U.S. companies that have sales in China that are going to be watching their earnings being downgraded next year until we get a deal with China"

- "The Chinese economy is slowing in a way that I haven’t seen in a decade," adding that it’s "going to be bad" for U.S. companies that have a lot of business in China

So, um, that’s a pretty cheerful outlook, especially with what looks like minimal movement on the negotiating front between the U.S. and China.

In case you missed it, we published a story yesterday that listed a slew of large U.S.-based companies (market cap above $5 billion) with heavy exposure to China (more than 10% of quarterly revenue attributed to the region) that investors may expect a ratcheting down of numbers, including many semiconductors like Applied Materials, Teradyne, and Texas Instruments, and gaming names like Wynn Resorts and Las Vegas Sands.

But perhaps Kudlow will stir up some optimism on Bloomberg TV later this morning, or maybe the resumptions of talks between the two sides next week will actually go somewhere.

But in the interim, bubkus. And not only that, we also have a government shutdown that is likely to be the longest ever, as Cowen put it earlier this morning -- "One week away from tying shutdown record of 21 days with no end or catalyst in sight to reopen" -- though there will be a resumption in talks (sound familiar?) later this morning between congressional leaders that should shed more light on the partisan schism.

Other no-good very bad things that happened were the China Caixin PMIs, which were downright ugly, and the U.S. ISM Manufacturing, which was worse. The latter index missing all estimates in the Bloomberg survey and new orders plunged by the most in nearly five years, which added fuel to the fire during Thursday morning’s post-Apple selloff.

Meanwhile, the airlines were a hot mess after Delta cut its revenue view for the second time in two months. Plus Ford’s auto sales whiffed, but the bigger news was the automaker joining GM by forgoing monthly reporting for quarterly.

Less transparency isn’t exactly what investors want to see, especially after what happened to Apple shortly after the company decided to stop reporting iPhone unit sales. And that came a day after Tesla cut prices, which decimated that stock given renewed demand concerns for the company’s vehicle offerings.

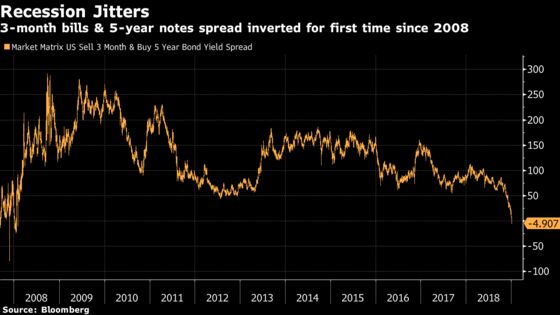

Oh, and both the S&P and Nasdaq went out at lows on Thursday. Portions of the yield curve inverted yesterday (spread between 3-month bills and 5-year notes turned negative for the first time since 2008, as the chart below shows, while the 1- and 2-year section also did the deed), which will only give fodder to those bears saying that a recession is around the corner.

Additionally, investors continue to pull money out of this market, with $18.7 billion of outflows in U.S. stock funds over the past week, according to Lipper.

And yet, it’s pretty amazing that we haven’t retested the December lows. Moreover, the S&P 500 is still up more than 4% since Christmas and looking to add to those gains with today’s early action: E-minis are up ~35 handles after China announced its first all-inclusive required reserve ratio cut since March 2016.

Perhaps today’s jobs data (Thursday’s ADP figure was actually a big beat) or Powell’s comments alongside Yellen and Bernanke at the American Economic Association meeting can help propel the bounce further. Though don’t be surprised if a heavy reversal weighs at some point during the session, as would be standard for what we’ve seen with this tape lately.

On Tap for Next Week

The American Economic Association conference isn’t just about the aforementioned three amigos. The event rolls on through the weekend, where New York Fed president John Williams will present a paper while Atlanta Fed’s Raphael Bostic and San Francisco Fed’s Mary Daly will participate in panel discussions. And there’ll be plenty more fed speak trickling in all week, including Powell speaking to the Economic Club of Washington D.C. on Thursday.

The other big event over the weekend is a Sunday night press conference from Jensen Huang, CEO of Nvidia, the leader in chips for computer graphics, at the consumer electronics show known as CES. Watch for any product announcements - Citi expects the company to announce a new partner in automotive following last year’s pacts with Uber and Volkswagen.

As for what to expect during the week, the resumption of U.S. and China trade talks are front and center, while the deep unknown of earnings preannouncements, revenue forecast cuts (thanks a lot, Apple) and the exhausting saga over the government shutdown are fresh in trader’s minds.

But in terms of catalysts set in stone, the focus falls squarely on the biggest healthcare event of the year: JPMorgan’s annual conference in San Francisco (see our giant presentation-by-presentation preview), which just got a little bit more exciting after Bristol-Myers ponied up a ton of dough for perennial biotech target Celgene - see below for iShares Nasdaq Biotech ETF, or IBB, components that rallied after the merger news hit the tape.

Other sell-side events that could provide actionable commentary on earnings, guidance and trade frictions include UBS’s Greater China conference in Shanghai, Citi’s global TMT West conference in Las Vegas (ON Semi, Roku, Verizon and AT&T) and Goldman’s global energy conference in Miami (Exxon, Chevron, and many more). There’ll also be plenty more tech CEOs giving keynotes at CES throughout the week.

As for earnings, we’ll get numbers from two important South Korean companies in electronics behemoth Samsung and flat panel TV maker LG Electronics as well as Indian IT services name Infosys. In the states, we’ll get results from Lennar (among the largest listed homebuilders), spirits giant Constellation Brands (now a quasi-pot stock), Bed Bath & Beyond (which has zero international revenues), and spray lubricant smidcap WD-40, which has relatively high exposure to Asia-Pacific at ~16% of sales.

Notes From the Sell Side

Goldman has a bevy of sector notes out today, but the one that’ll probably get the most attention is their call on Internet stocks. They maintain an attractive view on the group given "relatively high returns and growth relative to valuation" and upgrade Etsy and Expedia, downgrade Ebay, Snap and Criteo, and add Netflix to the conviction list.

BofAML sees potential for semiconductor stocks to trough sometime in the first quarter before re-acceleration of growth in the second half. They upgrade Intel to a buy and downgrade Texas Instruments, Maxim Integrated and Analog Devices (RBC is also out cutting ADI) all to neutral. Top picks are Broadcom and Marvell.

And looks like there’s a split in thinking on the auto suppliers today, with Baird downgrading a host of names (Adient, Autoliv, Veoneer to underperform and Visteon to neutral) while UBS upgraded both Lear and Dana to buy.

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- QCOM lawyers to present arguments in FTC trial

- 7:00am -- ANGO earnings

- 8:30am -- Nonfarm Payrolls, Unemployment Rate

- 8:30am -- LW earnings

- 8:30am -- FLXN 4Q guidance call

- 8:40am -- USX CEO Eric Fuller on Bloomberg TV

- 9:00am -- MNKD business update call

- 9:35am -- Larry Kudlow on Bloomberg TV

- 9:45am -- Markit PMIs

- 10:15am -- Powell, Yellen, Bernanke interviewed at American Economic Association

- 10:15am -- Fed’s Bostic speaks at AEA

- 10:30am -- EIA natgas storage

- 11:00am -- DoE oil inventories

- 11:30am -- Trump meets with congressional leaders at the White House

- 1:40pm -- Fed’s Mester on Bloomberg TV

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Arie Shapira

©2019 Bloomberg L.P.