There’s a Global Wall of Cash Primed to Snap Up U.S. Treasuries

There’s a sense that the peak in yields may not be far off.

(Bloomberg) -- The Treasury market’s bears had better take notice: There’s a wall of global cash poised to swoop in and buy, likely limiting the upside in yields.

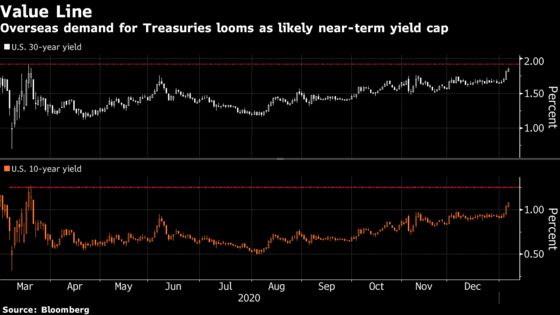

The prospect of a unified Democratic government has jump-started inflation expectations, catapulting long-term Treasury yields back to heights last seen in March 2020 -- and approaching levels where many international investors say they’d look to buy.

For money managers in Asia and Europe monitoring the world’s biggest economy, there’s a sense that the peak in yields may not be far off, amid concern over the fallout from soaring virus cases and the slow rollout of vaccines. There’s also the likelihood that President-elect Joe Biden’s $1.9 trillion stimulus proposal is going to face hurdles in a closely divided Congress that’s also about to take up impeachment proceedings.

The upshot is that investors in Europe, and particularly in Japan -- the biggest overseas holder of American government debt -- have their sights set on buying more if the 10-year gets into the 1.25% to 1.3% range and the 30-year to around the 1.92%-to-2% zone. In both cases that’s a mere 10 basis points, even a bit less, above the latest peaks seen before the surging reflation trade appeared to lose momentum.

“The trajectory on the virus is creating downside risks for economic data,” said Mark Dowding, chief investment officer in London at BlueBay Asset Management, which oversees about $67 billion. “Over the next few months, the 10-year yield should range between about 1% and 1.25%,” and the firm would look to buy if yields breached the top end, he said, with 2% serving as the key point for 30-year bonds.

Foreign demand has always been a key component of prognosticating in the Treasuries market, and there are far-reaching implications from this looming appetite. For one thing, it stands to limit the cost to U.S. taxpayers of financing the nation’s swelling debt load, at roughly $21 trillion and counting. But it also means investors in other asset classes may have less to fear from climbing Treasury yields.

The biggest bond dealers have a mixed take on what’s next for yields. HSBC this week recommended buying Treasuries on what it called an “overdone” selloff. Meanwhile, Goldman Sachs raised its year-end target for 10-year yields to 1.5% from 1.3%, given the “greater fiscal impulse” likely under unified Democratic control of government.

‘Huge’ Risks

But overseas buyers may not wait for rates to get that high, with cracks in the growth-rebound story emerging. This past week saw the biggest jump in filings for jobless claims since March, and an unexpected decline in retail sales.

“The risks around the economic outlook are huge,” said James Athey, a London-based money manager at Aberdeen Standard Investments, which oversees over $560 billion. “There are risks in both directions, but I’d argue the preponderance are to the downside -- toward less positive growth outcomes, less positive virus outcomes, less positive vaccine outcomes. If 10-year yields get to 1.25% to 1.30%, I’d be comfortable adding to my long-duration positions.”

Wall Street chart-watchers are looking at that area too as the next big obstacle for yields, given the level of roughly 1.27% represents the peak seen in the market pandemonium of March.

There are already signs that the bond-market selloff is luring buyers. This week, investors lapped up the Treasury’s sales of 10-year notes and 30-year bonds. The week ahead brings a $24 billion auction of 20-year debt.

Japan Decides

For the global bond market, much rides on the preferences of Asia-based investors. Japan owned about $1.3 trillion of Treasuries as of October, the biggest foreign pile. China is next with about $1.1 trillion, the least since 2017. On Tuesday, the government releases data for November. Markets are closed Monday for Martin Luther King Jr. Day.

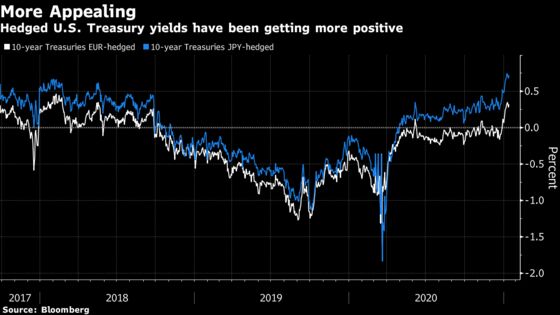

So far, Japan’s buyers are biding their time. For this key investor segment, yields aren’t quite high enough to give them confidence they’ve limited potential capital losses. That’s even as the yen has reached the stronger end of its recent ranges and as the cost of currency hedging has dropped.

“There won’t be much of an outflow from Japan until Treasury yields stop rising,” said Takenobu Nakashima, chief rates strategist at Nomura Securities.

For Nakashima, one strong signal will be if U.S. 10-year rates, adjusted for hedging costs, consistently exceed 30-year Japanese government bond yields -- which are around 0.65%, up from around 0.25% in March. That’s been the case for roughly a week now.

“Japanese investors tend to buy big after confirming yields have peaked out -- they aren’t momentum riders,” said Masahiko Loo, a fixed-income portfolio manager at AllianceBernstein Japan. “There won’t be a major outbound shift until 10-year yields rise to 1.3%, as current levels would return just about 80 basis points after hedges, and buying at these levels likely is just confined to short-covering.”

To be sure, some investors -- such as life insurers with longer-dated yen liabilities -- may be content to keep more money at home after Japanese yields climbed last year on supply concerns.

Signals Parsed

The next step in the bond market may depend in part on signals from the Federal Reserve related to its bond-buying program. The yield targets that these overseas buyers are aiming for grew a bit more distant this week after Fed Governor Lael Brainard pushed back against suggestions the central bank could taper its asset purchases later this year.

Remarks from other officials that discussions about such a shift may be possible in 2021 had driven a key measure of the yield curve to the steepest since 2017. That move and the falling costs of hedging currency risk have made Treasuries more appealing for foreign accounts, with roughly $17 trillion of global debt yielding less than zero.

“There is a significant yield advantage to be had in U.S. Treasuries versus these other markets,” said John Taylor, London-based money manager at AllianceBernstein. “The cost to hedge the currency is minimal -- all central banks are effectively at zero -- so global flows will likely move into the U.S. market if the yield gap widens further.”

What to Watch

- In a holiday-shortened week with no major data releases, the highlights may be the Jan. 19 confirmation hearing of Janet Yellen for Treasury secretary, followed by Biden’s inauguration the next day

- The economic calendar:

- Jan. 19: Treasury International Capital flows

- Jan. 20: MBA mortgage applications; NAHB housing index

- Jan. 21: Building permits; Philadelphia Fed business outlook; weekly jobless claims; housing starts; Bloomberg economic expectations/consumer comfort

- Jan. 22: Markit U.S. PMIs; existing home sales

- The Fed calendar is empty before the Jan. 27 decision

- The auction schedule

- Jan. 19: 13-, 26-week bills; 42-, 119-day cash-management bills

- Jan. 20: 20-year bonds

- Jan. 21: 4-, 8-week bills; 10-year TIPS

©2021 Bloomberg L.P.