The Tape Isn’t Telling You the Whole Truth: Taking Stock

The Tape Isn’t Telling You the Whole Truth: Taking Stock

(Bloomberg) -- The tilt is higher, and you can point to a couple reasons this morning, though to the extent that this screams buy U.S. stocks is arguable -- especially on quadruple witching day where we are bound to see some interesting activity with elevated volumes.

China stimulus measures as part of its annual National People’s Congress session definitely boosted stocks in the Asian region, and anything to boost the sagging growth outlook will help the usual suspects here, mainly some key tech names like Micron and AMD, or economically dependent names like U.S. Steel.

There’s more green on the screen than not, and Broadcom’s results post-market definitely helps firm up the semiconductor sentiment worries that surfaced a few months ago, and lend credence to the fact that the market in that segment has bottomed. But some key names may provide some downside pressure to be aware of this morning:

Mega-cap Oracle disappointed, and has already attracted a downgrade and some tempered optimism from a key bull:

- BMO’s Keith Bachman is moving to the sidelines with a cut to market perform, and is "dubious" that the business software and cloud name can improve its revenue rates

- Overweight-rated Piper Jaffray highlighted "expectations were elevated" with positive sentiment, and noted that the company’s guidance for revenue growth is likely weighing on the stock

Adobe is also weaker, here’s what some on the Street are saying:

- Cowen sees "lots of noise" in the numbers and cut its price target. "Peeling back the onion" on the numbers, the analysts write, "create new questions" around the company’s momentum

- Morgan Stanley wrote that you shouldn’t read too much into the results after a "very strong" multi-year move in the stock. Ultimately though, results lacked key elements of how it got to this point: consistent beat and raise quarters, low operating expenses, and ARR ahead of expectations

Tesla’s Model Y unveiling broadly disappointed with shares lower this morning, as some indicate it doesn’t do enough to differentiate:

- Morgan Stanley’s Jonas asks "Y" you should buy a Model 3 when so much is shared between the two. He sees likely cannibalization among the models

- There were "few surprises," RBC’s Joseph Spak wrote, indicating it felt "very Model 3-ish" with slightly more room. He also discussed the mood at the event as "more subdued" than events he had seen from the company before

Redemption (maybe)

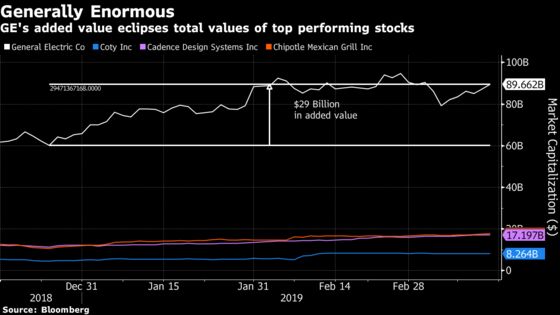

In other areas of the market, its worth taking a look at our favorite industrial giant following yesterday’s crazy action. GE has come a long way. It is now the best performer in the S&P over the past three months, with gains in excess of 50% (!). Critics could point to the low base and share price from which it built this return as part of the story, but the bottom line is in pure market value growth, there’s no competition among the top percentage gainers this year, which include Coty, Cadence Design Systems, and Chipotle Mexican Grill.

This may not have been the case if just a few different things occurred. Its guidance early in the day missed expectations -- expectations that had already come down following the CEO’s comments at the JPMorgan conference just days earlier. The market has rewarded honesty. His discussions of debt being too high, the challenges that still face the company and a free cash flow view for 2020 that exceed some expectations put investors at (slightly more) ease. With the latest rebound, shares are trading more in line with its 5-year historical multiple on a blended forward P/E, and a slight discount on blended forward enterprise value/EBITDA ratio basis.

A Little Pick-Me-Up

Another relatively under-the-radar development in recent months seems to be changing course. My colleague Elena Popina explains.

The past few months have been rough for drug-store chain stocks, but it looks like they have finally found a bottom following a slump. After losing a quarter of its value in 12 days since Feb. 20, CVS has gained 6.7% in the last five sessions; Walgreens is up 3.4% in the same time, while Rite Aid is has gained 13% in the past six days (the Street saw management changes, job cuts and $55 million in cost savings announced on Tuesday as a step in the right direction).

There were not too many industry-specific catalysts for a rebound, but the likely thinking was that the rout has gone a little too far (a confluence of factors caused the slump in the first place, from mediocre quarterly results [for CVS and Walgreens] to concern over Amazon.com breaking into the sector, floated "medicare for all” plans by Congressional Democrats, to news that the FDA put Walgreens on notice for selling cigarettes to minors).

All three stocks were up Thursday, with Walgreens and Rite Aid being among the top five gainers in the BI North America Health Care Supply Chain Competitive Peer Group. Among the top gainers, Diplomat Pharmacy is due to report later this morning. Rite Aid has rallied in response to a management shake-up, while CVS has gained partly because Bernstein’s analyst Lance Wilkes joined a list of CVS bulls, initiating his coverage with a buy and saying he sees the company as a long-term winner amid Aetna’s solid government growth outlook and an attractive retail strategy (the $68 billion CVS/ Aetna acquisition closed in November). This comes after Citi cut the stock’s price target to $68 from $94 last week, citing concerns about the firm’s debt and cash flows.

On Tap for Next Week

Two major central banks - in the U.S. and England - post decisions on policy rates next week, with the Federal Reserve announcing the decision on Wednesday and the Bank of England the next day. The Fed and BoE are both expected to hold on to raising rates, but what would be of particular importance is the policy makers’ forecast on the pace of future rate hikes.

The earnings season is winding down, but next week will bring a few important announcements. Nike is due to report its third-quarter after the bell on Thursday (watch for the company’s North America and online sales, which powered the company’s second-quarter results beat). FedEx is due to report on quarterly results on Tuesday. To Lee Klaskow, an analyst at Bloomberg Intelligence, slowing growth in Europe and China has added pressure to the stock’s valuation, so it could be worth watching the sales numbers in from these regions. The Dow Jones Transportation Average that FedEx is a part of has plunged in 13 of the past 15 days.

Also happening in the days ahead: Edwards Lifesciences and and Medtronic’s low-risk transcatheter aortic valve replacement studies are scheduled as late-breakers on Sunday, March 17 (see preview). Fox Corp. (new Fox effectively post-Disney merger), will begin trading under TFCF next week. March Madness is upon us, and the 68-team lineup for NCAA men’s college basketball tournament will be revealed during a Selection Sunday on March 17. The first round begins March 21.

Notes From the Sell Side

One of the few holdouts for Amazon bullishness turned positive on Friday, with KeyBanc upgrading the stock to overweight. With the move, there’s now just one firm with a hold rating and just one with a sell, compared with 47 buys. KeyBanc forecast “an inflection point in Amazon’s profits over the next three years” that will be “driven by improving retail margin expansion coupled with the mix shift to higher margin [Amazon Web Services] and Advertising segments.” Analyst Edward Yruma wrote that there had been “a litany of recent announcements that, in aggregate, can improve retail margins.” Among these is the introduction of “Amazon Day,” which “allows preassigned consumer pickup days that should improve shipment cost efficiency.” Such moves, along with continued growth in the high-margin AWS and advertising businesses, could “justify the next leg of multiple expansion.”

AT&T was upgraded to outperform at Raymond James, which wrote that positive earnings growth, “combined with a strong de-levering story,” are likely to drive shares toward its $34 target, which it described as conservative. Analyst Frank Louthan wrote that short-term investors “may not find this case particularly compelling,” but that for those with a long-term view, “locking in the 6.7% yield and waiting for mean reversion in valuation is likely to be rewarded.”

Sectors in Focus Today

- Women’s retail (JILL, NWY, FRAN) after Ascena Retail adj. EPS missed the lowest analyst estimate and is indicated to have it worst day since mid January; other retailers also disappointed, with teen retailer ZUMZ also missing expectations and TLYS

- Cloud players after a series of large tech names reported, including PVTL (marginally lower), DOCU (-4.7%), ORCL (-3.5) and ADBE (-3%)

- Semiconductor names as Broadcom beat consensus for earnings and the forecast for the year implies 2H improvement for the segment (watch the SOX index in which its a large constituent, SWKS, ADI, MCHP)

Tick-by-Tick Guide to Today’s Actionable Events

- Chinese premier’s press conference at closing of National People’s Congress

- GNW/China Oceanwide -- deal termination deadline

- 6:00am -- BlackRock holds annual general meeting

- 8:30am -- US Empire State Manufacturing

- 8:32am -- Tiger Woods tees off at the Player’s Championship with Webb Simpson and Patrick Reed

- 9:15am -- Industrial Production

- 10:00am -- University of Michigan Consumer Sentiment

- 10:00am -- HEI, TPVT hold annual general meeting

- 1:00pm -- SNX annual general meeting

--With assistance from Ryan Vlastelica and Elena Popina.

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.