The Rumbling Sound in U.S. Stocks Is the Return of Risk Appetite

The Rumbling Sound in U.S. Stocks Is the Return of Risk Appetite

(Bloomberg) -- Beneath the din of earnings, clanging economic alarms and the blare of a political circus, U.S. investors are quietly rediscovering their nerve.

With the S&P 500 just touching a record, it may sound odd to suggest there was a lack of confidence to begin with. But gains this year have been built on caution as investors chased the safest, most bond-like shares.

Not so this week. A strategy of buying cheap stocks won, while defensive names faltered. Small-caps, the most-shorted companies and the rockiest equities all beat the S&P 500 as it crawled toward its peak.

These are the faint sounds of risk appetite returning. Not a blast, like last month, but a steadier beat. After months of fear, this not-so-bad earnings season, hopes for a mini trade deal between the U.S. and China, and the occasional defiant economic reading are proving just enough to rekindle optimism.

“There’s been a strong crowded positioning into defensive sectors and secular growth,” said Jason Draho, head of Americas asset allocation at UBS Global Wealth Management. “If things actually get better, there’s upside certainly for equities, but the bigger story is more of a rotation of people looking to buy cyclicals, looking to buy potentially value, and other markets that have underperformed the U.S.”

Consider the winners list from the week just ended. While household product makers and real estate companies have dominated most of the year, the last five days saw gains of 9% or more in Tiffany & Co., Intel Corp. and Halliburton Co. The four best performing industries in the S&P 500 were energy, chipmakers, banks and transportation.

About a fifth of all S&P 500 members reported earnings this week, and on balance they have beaten -- admittedly low -- expectations. That’s persuaded some investors U.S. companies are weathering the trade storm and reminded them slowing global growth is not the same as no global growth, or worse.

At the same time, the pessimism that has defined the bond market in 2019 is easing. The yield on 10-year Treasuries has rebounded about 30 basis points from a three-year low last month, and most economists expect the Federal Reserve to pause rate cuts after one more next week. The MOVE Index of expected volatility for U.S. bonds just posted the biggest weekly drop since January.

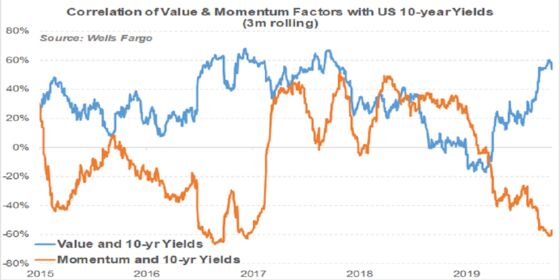

For value shares and smaller listed companies, that is key. Value’s positive correlation with bond yields has been strengthening lately, while the relative performance of small caps is also increasingly tied to the debt market, Pravit Chintawongvanich, a strategist at Wells Fargo, wrote in a note this week.

Even so, it’s doubtful any investors will be getting carried away -- memories of September are too fresh for that. Back then, the strategy of chasing winners and dumping losers -- dubbed momentum -- was hammered amid a sudden violent shift in sentiment that spurred value shares. But it didn’t last.

After two weak business investment readings on Thursday, value lost a bit of ground as the momentum cohort recovered. This month’s rotation has also been a reflection of some idiosyncratic sector moves. Energy was the best performing sector in the S&P 500 this week after oil prices climbed to the highest in a month.

“Is this the start of a lasting rotation? It is really hard to say, but for now it seems to be more driven by sentiment than by macroeconomic effects,” said Olivier Blin, a fund manager at Unigestion SA. “It’s possible that we remain in that fairly choppy environment with individual performance seesawing depending on the geopolitical or monetary policy context.”

All the same, Blin has dialed down exposure to factors such as low-risk that are sensitive to rising bond yields and turned overweight on value and carry strategies.

For now, the economic picture has ammo for bulls and bears alike. While data this week showed U.S. business investment declined, initial unemployment claims fell slightly and sales of new homes stayed close to the strongest pace of the expansion. Meanwhile, simmering political tension in Washington continues to hang over markets.

Yet value investors have other reasons to be bullish. The factor is almost the cheapest versus growth shares -- those with the potential for faster sales or profits -- since the dot-com bubble, meaning there’s a low bar for the rotation to continue. Bank of America Corp. strategists last week recommended neutralizing exposure to momentum and adding value, arguing the latter remains neglected and tends to do best in the fourth quarter.

“There’s an asymmetric type of scenario where if things get better, the stuff that’s really underperformed can snap back quite a bit, whereas if things get worse, they’re already priced for negative news,” said Draho at UBS WM. “The flip-side is if things do get better there’s a lot more potential downside in some of the more defensive proxies.”

To contact the reporters on this story: Justina Lee in London at jlee1489@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.