The Risk of Fallen Angels in Asia’s Bond Market Is Rising

For a group of borrowers that sit on the cusp of a junk rating, there’s no relief in sight.

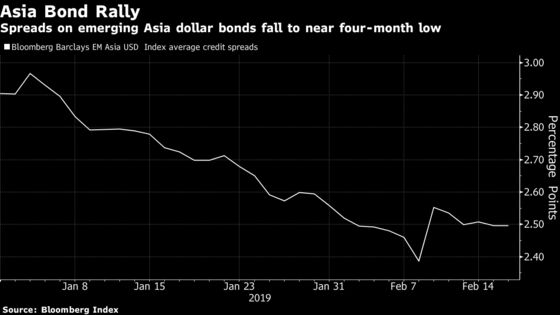

(Bloomberg) -- Asia’s dollar bond markets have staged a blistering rally this year, but for a group of borrowers that sit on the cusp of a junk rating, there’s no relief in sight.

As worsening global macro-economic conditions put firms under pressure, concerns over so-called fallen angels, or investment-grade companies that are cut to junk, are mounting in Asia and globally. Man Group Plc, the world’s largest publicly traded hedge fund manager, warned investors in December of the “astonishing bubble” in BBB level debt.

The U.S.-China trade war and jitters over a slowdown are prompting worries that weaker companies could falter. Moody’s Investors Service cut Bharti Airtel Ltd., India’s second-largest wireless carrier, to junk earlier this month and downgraded five Asian companies in January, compared with two upgrades. A move to below investment grade raises borrowing costs and also prompts a wave of forced selling by investors who may be unable to hold junk securities.

“The macro picture remains a major headwind for the investment market,” said Arthur Lau, head of Asia ex-Japan fixed income at PineBridge Investments, who sees more fallen angels in the region this year. “Some of the companies are likely to face more margin pressure and operational challenges.”

Election Risk

Globally, an era of easy money has fueled borrowers to take on leverage and they remain vulnerable to any tightening in liquidity. In Asia, major elections in countries like India could also throw up surprises for investors, and add to the volatility. At least eight Asian companies’ bonds were cut from investment grade to junk in 2018, an increase from four during the previous year, according to Bloomberg-compiled data.

Read more of BlackRock’s views on BBB debt

Borrowers that are on the brink include India’s state-owned Power Finance Corp. and REC Ltd., which are both rated one step above junk by Moody’s and Fitch Ratings. Indian chemical giant UPL Ltd.’s bonds are also on the edge of becoming non-investment grade.

“There are more issuers on the borderline with a worsening credit profile,” said Manjesh Verma, head of Asia credit sector specialists at Citigroup Inc. “We see rising fallen angel risks.”

Some of the bonds on the cusp of junk are “mispriced” and price declines would be “significant” if these companies drop to junk grade, Verma said.

To contact the reporter on this story: Denise Wee in Hong Kong at dwee10@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Ken McCallum, Beth Thomas

©2019 Bloomberg L.P.