The Moody’s Mystery Is How South Africa’s Rating Held Up So Long

The Moody’s Mystery: A South Africa Rating That Just Won’t Sink

(Bloomberg) -- Explore what’s moving the global economy in the new season of the Stephanomics podcast. Subscribe via Pocket Cast or iTunes.

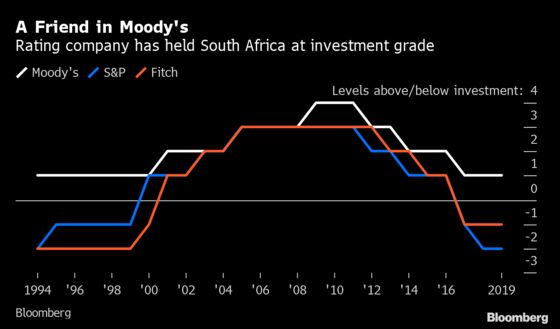

For a quarter-century, South Africa has been able to count on an investment-grade rating from Moody’s Investors Service. Bond buyers lately may be forgiven for wondering why.

Financial markets have been pricing in a downgrade for months, and the other two major rating companies have had South Africa at junk status for two years. Should Moody’s follow suit, the nation would suffer enormous financial consequences.

For one, the country would lose its place in the FTSE World Government Bond Index, which requires at least one investment-grade rating from either Moody’s or S&P Global Ratings. Exiting it would spark an investor selloff and outflows of as much as $15 billion, according to Bank of New York Mellon Corp., at a time when South Africa needs portfolio investment to finance its persistent current-account deficit. A downgrade would also raise borrowing costs, complicating the government’s efforts to balance the budget.

South Africa doesn’t need more fiscal woes. It’s already spending 138 billion rand ($9.2 billion) to bail out Eskom Holdings SOC Ltd., the troubled state power utility. Coupled with other likely industry aid packages, deficit spending will rise to a decade high next year, with debt topping 70% of gross domestic product, according to this week’s medium-term budget statement. The country’s 10-year bond yield is almost three percentage points higher than lower-rated Brazil’s.

“From a rating agency’s perspective, this means only one thing: The debt trajectory is unsustainable over the long term,” Cristian Maggio, London-based head of emerging-market strategy at TD Securities, said in a report after Wednesday’s budget release. “We think the sovereign debt ratings will have to be adjusted lower.” An “outright downgrade is unlikely without a prior change of outlook.”

Finance Minister Tito Mboweni himself said Thursday that the fate of the Moody’s rating was “not looking good.” Most analysts in a recent Bloomberg survey predicted that Moody’s would change its outlook on the nation’s credit rating to negative, from stable, before the end of the year -- a move likely to precede a downgrade. Moody’s is scheduled to review its rating on Friday, after a call with Treasury officials. The company declined to comment on why it hadn’t downgraded South Africa.

“I expect Moody’s to look at three things: the debt metrics, is our growth story credible and what are we doing on the expenditure side,” Dondo Mogajane, director-general at the National Treasury, said in an interview in Cape Town. “It remains a challenge and a concern.”

Moody’s already rates Eskom’s long-term debt at B2, five notches below investment grade and lower than Fitch. That means the utility has to rely on government guarantees to borrow in capital markets, increasing the strain on state finances. Should Eskom be unable to repay its debt, the government would be on the hook for as much as 280 billion rand.

Moody’s, say former government officials, investors and economists, has kept South Africa investment-grade partly because of history, partly because of methodology.

When South Africa emerged from apartheid and the consequent international isolation in 1994 under the leadership of Nelson Mandela, one of the first things it sought was a credit rating that would allow the government to access funding in international markets. Fitch responded with a BB rating, two levels below investment grade, and S&P followed suit.

Then came Moody’s, with an assessment of Baa3, the lowest investment rating and two levels higher than the others. Mandela’s charisma had something to do with it, according to Estian Calitz, director-general of the Treasury at the time and now an economics professor at Stellenbosch University.

But South Africa also worked hard to earn credibility, he said.

The president and his cabinet “had a profound understanding of what it would take to get South Africa back to international markets,” maintaining fiscal discipline even as they pursued policies aimed at redressing economic inequalities, Calitz said earlier this year.

President Thabo Mbeki, who succeeded Mandela in 1999, continued along that path, and South Africa’s credit rating improved during his administration. It reached its apex with Moody’s in 2009, a year after Mbeki was replaced by Jacob Zuma. That’s when the tide started turning, according to Lungisa Fuzile, a former director-general of the Treasury who resigned from office during Zuma’s presidency.

A series of downgrades ensued, sparked by a slowing economy, institutional decline and rising political risks, including Zuma’s firing of his respected finance minister, Nhlanhla Nene. By 2017, Fitch and S&P had the country at junk, while Moody’s had shaved its rating by three levels.

Moody’s and S&P consider broadly similar factors when making their assessments, according to information published on their websites: The economy, institutional strength, fiscal position and susceptibility to event risk. But Moody’s appeared to give greater weight to the institutional and political factors that underpin the willingness to repay debt, according to Calitz.

“The rating companies had two questions in 1994: Can you repay foreign debt and service debt until maturity, and will you do it?” said Calitz. “The political factor seemed to have weighed a bit more with Moody’s than with S&P. Moody’s seemed to look more at the political economy whereas S&P was stronger on the technical factors.”

It’s not like Moody’s hasn’t come close to cutting South Africa to junk. The company placed it on review for a cut to sub-investment grade in December 2017. But when the review was concluded three months later, the country kept its Baa3 rating and was rewarded with an outlook change to stable from negative.

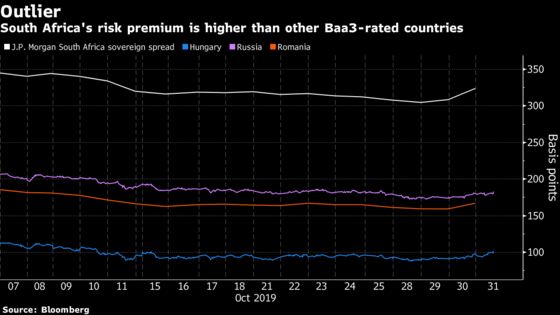

Market pricing indicates it’s only a matter of time before Moody’s comes into line with its competitors. The cost of insuring South Africa’s debt for five years using credit-default swaps is more than double that for Russia, which has a similar rating at Moody’s. And it’s higher than that of Brazil, which is rated junk.

The premium investors demand to hold South Africa’s dollar debt rather than similar-maturity U.S. Treasuries, at 345 basis points, is about on par with Bolivia, rated one step below investment level, and Jamaica and Belarus, both six notches into junk. And among emerging markets, only junk-rated Turkey, Lebanon and Nigeria pay more for 10-year local-currency debt.

South Africa’s longer-maturity debt and its low level of foreign-currency bonds -- 10% of total debt -- set the country apart from other emerging markets, said Lucie Villa, Moody’s vice president and lead sovereign analyst for South Africa, in September.

“That’s certainly something that explains one of the reasons why we are at Baa3 at the moment,” Villa said at the company’s sub-Saharan Africa summit in Johannesburg.

While the country still faces major challenges -- including the crisis at Eskom -- President Cyril Ramaphosa has started repairing some of the damage since he came into office in February last year. Though some investors are frustrated at the slow pace of change, Moody’s is giving him some breathing room, said Gina Schoeman, a Johannesburg-based economist at Citigroup Inc.

“Moody’s will look at all of this and say he’s actually had very little time to enact a lot,” Schoeman said. “It comes down to, will Moody’s see fiscal effort, are they seeing an effort to actually do something on growth? And then they’re going to have to weigh that up with the more fundamental deterioration in GDP, in debt, in the fiscal metrics.”

To contact the reporters on this story: Robert Brand in Cape Town at rbrand9@bloomberg.net;Prinesha Naidoo in Johannesburg at pnaidoo7@bloomberg.net

To contact the editors responsible for this story: Rene Vollgraaff at rvollgraaff@bloomberg.net, Anne Swardson, Paul Sillitoe

©2019 Bloomberg L.P.