The $200 Trillion Gold Rush That Has Reshaped Private Banking

The $200 Trillion Gold Rush That Has Reshaped Private Banking

(Bloomberg Markets) -- Ten years ago, stock markets plunged, major banks faltered, and the global economy teetered on a precipice. Few would have predicted that the ensuing decade would produce an explosion in wealth.

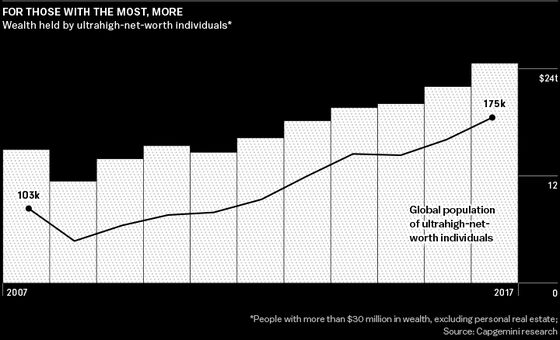

But that’s just what happened. An unprecedented infusion of central bank funds into the world’s largest economies bolstered asset prices, making many people richer and exacerbating inequality. Global personal wealth reached a record $201.9 trillion last year, according to Boston Consulting Group Inc.

For some banks, this burgeoning affluence brightened an otherwise dreary postcrisis landscape. Giants including UBS, Morgan Stanley, and Bank of America seized the opportunity. With trading desks hamstrung by a flurry of new rules, banks set out to woo the growing ranks of the super rich.

But the business of managing the fortunes of the elite was changing as well. The U.S. and Europe cracked down on tax evasion, driving clients to pull tens of billions of dollars out of Switzerland and forcing private banks there to seek new pockets of wealth. Money laundering scandals brought fines and yet more rules. Compliance costs soared, and clients started paying closer attention to fees and the services they received for them. Technology made nimbler, cheaper investing tools possible.

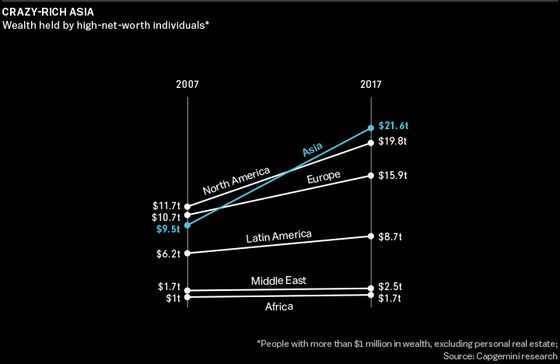

Perhaps the biggest force reshaping global wealth management has been the ascent of China. Its economic expansion produced an eruption in private wealth across Asia, where almost 2,000 people become millionaires each day. In 2015 the Asia-Pacific region overtook the U.S. in assets held by millionaires, leaving banks scrambling for talent and office space. Local banks challenged the dominance of established Western wealth managers. As China opens its market to foreign companies, an ocean of money is waiting to be tapped.

In the Americas, Canadians are feeling the positive impact of the tech boom and new asset classes such as cannabis and cryptocurrencies. Funds from rich Latin Americans are flooding Miami in search of political stability and a haven currency. Across the industry, but particularly in the U.S., the super rich’s family offices invest and network like institutions. At the lower end of the wealth spectrum, meanwhile, registered investment advisers and robo-advisers use low-cost funds to take business away from private banks.

Looming over this gold rush is the end of the central bank stimulus that drove so much wealth creation. Interest rates are rising in the U.S.; China is seeking to curb a record borrowing binge. Throw in the escalating trade war between the U.S. and China, Britain’s exit from the European Union, and rising nationalism across the globe, and the next decade may prove far more challenging for wealth managers than the last one. —Devon Pendleton and Christian Baumgaertel

In Switzerland, Bankers Read Balance Sheets

TOTAL POPULATION

8.5 MILLION

HIGH-NET-WORTH INDIVIDUALS*

474,000 (5.6%)

Andreas Arni remembers the heyday of Swiss private banking. As a wealth manager at Credit Suisse Group AG in the 2000s, he spent his days chasing after the fortunes of rich Latin Americans. Money was pouring in from around the world, lured by the promise of Swiss banking secrecy.

These days he’s leading about 100 relationship managers chasing a different type of client: Swiss entrepreneurs. These clients aren’t looking to hide money from the taxman, but rather to extract it from their businesses, get help with succession planning, and achieve competitive investment returns. And because their money isn’t stuck in an undeclared account, they will shop around for better and cheaper services elsewhere if they’re not happy.

“To serve these clients, you need bankers who understand balance sheets and companies,” Arni says in a conference room at Credit Suisse’s headquarters on Zurich’s Paradeplatz. “Ninety percent of the wealth of entrepreneurs sits within their companies. You need to find it and unlock it.”

Swiss private banking has been transformed since the U.S. and European governments cracked down on secrecy, imposing billions of francs in fines and requiring banks to disclose information on international clients. Four years ago a Credit Suisse unit pleaded guilty to helping Americans cheat on their taxes, becoming the first global bank in a decade to admit to a crime in a U.S. courtroom. The rising cost of complying with new regulations squeezed profit margins, especially at smaller banks, pushing dozens to close or combine.

The survivors adapted by exiting less profitable markets and offering clients access to specialized investments, including infrastructure and real estate, to improve returns. Swiss private banks—apart from Credit Suisse and UBS Group AG—doubled their profits, to 2.8 billion francs ($2.8 billion) in 2017 from two years earlier, according to a KPMG LLP study.

Although booming equity markets helped, so did changes in strategy. “The competitiveness in the market due to lower margins and the regulatory environment led to a further professionalization of the industry,” says Patrick Odier, senior managing partner at Bank Lombard Odier & Co., Geneva’s oldest private bank.

Switzerland still attracts the biggest share of the global elite’s fortunes: more than $1.8 trillion in offshore money last year, or 21 percent of the $8.6 trillion market, according to a Deloitte LLP report. But it’s facing tougher competition from Hong Kong, Singapore, the U.K., and the U.S. as the overall market for offshore wealth management has been shrinking.

Swiss banks are seeking new clients at home. Those include thousands of closely held, often family-owned businesses. In Switzerland, some $160 billion in assets is tied up in such companies, according to Boston Consulting.

UBS and Credit Suisse, which scaled back their trading units after the financial crisis, are increasingly using their capital to finance transactions for private-banking clients. The goal is to persuade rich clients to trade more and bring business such as initial public offerings to the investment bank.

“It’s not enough to simply wait for the liquidity event. You constantly have to come up with ideas to add value for them,” says Jean-François Bunlon, head of Swiss domestic clients at HSBC Private Banking SA in Geneva. —Jan-Henrik Förster

* High-net-worth individual defined as adult with more than $1 million in financial wealth, excluding real estate. Source: BCG Global Wealth Market Sizing Database

In Canada, New Tech Wealth Rushes In

TOTAL POPULATION

36.7 MILLION

HIGH-NET-WORTH INDIVIDUALS

460,500 (1.3%)

To see the changing face of wealth in Canada, consider blockchain advocate Anthony Di Iorio. The entrepreneur, who turns 44 in January, bought Canada’s largest penthouse condominium outright in June, cashing in cryptocurrency to help cover the C$28 million ($21.4 million) price for the top three floors of the St. Regis Residences Toronto.

Early bets on Bitcoin and the blockchain-based Ethereum platform pushed Di Iorio’s riches to levels as lofty as the view from his 57th-floor wraparound terrace overlooking Canada’s largest city. He parlayed that fortune into investments in dozens of tech startups and his own company, Decentral Inc. “I’ve always reinvested and tried to create businesses that create value, rather than just take the money and not do anything,” says Di Iorio, whose V-neck T-shirt, dark jeans, and white sneakers belie his wealth.

More Canadians are becoming millionaires because of strong economic growth and a real estate boom. Aging business owners and baby boomers are looking to cash out. But a burgeoning technology industry here, bolstered by government policies that support tech education and welcome immigrants with tech skills, is also fueling newfound riches.

Canada is home to top researchers in artificial intelligence, prompting giants such as Microsoft Corp. and Google parent Alphabet Inc. to open facilities in cities including Montreal and Toronto. Several pioneers in blockchain and cryptocurrency are Canadian, and Ethereum, which Di Iorio helped get off the ground, was conceived in the country. Toronto created more jobs in 2017 than the San Francisco Bay Area, Seattle, and Washington, D.C., combined.

Last year Canada ranked eighth worldwide for the number of individuals with at least $1 million to invest, holding a combined wealth of $1.2 trillion, according to Capgemini SE.

Emerging tech riches haven’t gone unnoticed by bankers such as Ann Bowman at Royal Bank of Canada, one of the world’s largest wealth managers with C$986 billion under administration. RBC’s 175 private bankers in Canada specialize in business owners, executives, and star athletes, but the bank also courts those in technology. “We typically work at an early stage of wealth creation, because complexities are occurring much earlier than that IPO that identifies that unicorn billion-dollar tech company,” Bowman says. She leads Canadian private banking from the 14th floor of Royal Bank’s headquarters in Toronto’s financial district.

Canadian wealth managers are cultivating younger, tech-savvy entrepreneurs often ill-equipped to deal with sudden riches, says Joanna Rotenberg, who leads Bank of Montreal’s personal-wealth management businesses. “Our opportunity, frankly, is to help these people who have in some ways popped their heads up into large financial success.”

Wealth also has emerged from Canada’s marijuana industry after the government legalized the drug for recreational use in October. A pot-stock boom made millionaires out of some investors and executives, with those betting on companies such as Canopy Growth Corp. and Tilray Inc. finding new fortunes—at least on paper.

The swelling ranks of Canadian millionaires have banks looking toward expansion. Toronto-Dominion Bank agreed to buy Greystone Capital Management in July, adding a platform with alternative assets and funds attractive to the wealthy. Bank of Nova Scotia spent C$3.54 billion this year on MD Financial Management, which caters to doctors and their families, and Montreal-based money manager Jarislowsky Fraser.

Although tech riches are a recent phenomenon, property has been king for much of the past decade, says Brad Henderson, chief executive officer of Sotheby’s International Realty Canada. That’s driven demand for luxury homes. “The population of people who can afford top-tier homes in Canada has gotten bigger,” says Henderson, who credits the tech boom and the success of those who own businesses or work in areas such as banking. “As much as we look at certain properties and think that they have eye-popping values, they do sell.”

Di Iorio says his 16,178-square-foot Toronto penthouse, one of the most expensive in Canada, is part of his “safety net” of real estate investments. “I see it as less risky than crypto,” he says. “It’s good to diversify.” —Doug Alexander

In Saudi Arabia, Riches Mingle With Risks

TOTAL POPULATION

31.8 MILLION

HIGH-NET-WORTH INDIVIDUALS

59,000 (LESS THAN 0.2%)

First, JPMorgan Chase’s Jamie Dimon canceled, then BlackRock’s Larry Fink and Blackstone Group’s Stephen Schwarzman.

One by one, the leaders of the world’s top banks and investment managers said they would skip the most important financial gathering in the Gulf region, Saudi Arabia’s Future Investment Initiative. The executives, many of whom had lauded Crown Prince Mohammed bin Salman at the event a year earlier, were rattled by an allegation so gruesome they chose to stay away: that Saudi operatives had killed and dismembered Jamal Khashoggi, a journalist critical of the government.

The incident highlighted the quandary for wealth managers as they seek to tap the region’s vast riches. On the one hand, the crown prince’s plan to transform the kingdom’s oil-dependent economy by selling state holdings and investing in infrastructure and financial assets could spur a new wave of wealth creation. On the other hand, Khashoggi’s shocking disappearance was hardly the only troubling development since Prince Mohammed consolidated power.

Saudi Arabia has flexed its military muscle in Yemen, pushing as many as 14 million people to the brink of starvation, and led a coalition of regional allies in a blockade of Qatar. The crown prince imprisoned dozens of Saudi princes, ministers, and senior officials at the Riyadh Ritz-Carlton Hotel for months as part of an anticorruption crackdown. Earlier this year he even picked a diplomatic fight with Canada.

The Gulf has long been a target for international wealth managers, but much of the business was traditionally conducted from hubs like Geneva or London. There are more than 650,000 high-net-worth individuals in the Middle East, according to Capgemini’s wealth report. Their wealth, including real estate investments, increased more than 75 percent over the past decade, to $2.5 trillion in 2017, even with oil prices depressed for years.

After Crown Prince Mohammed unveiled his economic blueprint in 2016, banks started expanding in the region. Credit Suisse, whose biggest shareholders include Qatar and Saudi Arabia’s Olayan Group, is looking to hire more relationship managers in Saudi Arabia to offer private-banking services. UBS, which has had a physical presence in the region for more than 50 years, plans to invest more. Deutsche Bank AG, with Qatar among its top shareholders, is targeting the Middle East as a priority.

The opportunity in Saudi Arabia means even those executives who blanched at the Khashoggi scandal aren’t quitting the country. JPMorgan Chase & Co.’s Dimon said his decision to drop out of Saudi Arabia’s October conference accomplished “nothing” and that business relationships with the country will continue. BlackRock Inc.’s Fink said in early November that doing business in Saudi Arabia is “not something I’m ashamed of.” —Archana Narayanan

In Miami, Latin America’s Offshore Hub Thrives

LATIN AMERICA’S TOTAL POPULATION

639 MILLION

HIGH-NET-WORTH INDIVIDUALS

190,300 (LESS THAN 0.03%)

Every December, the migration begins. Moneyed people from all over the globe flock to South Florida to attend Art Basel Miami Beach, one of the world’s premier art fairs. Many stay the week; others wait out the winter. Others decide it’s time to relocate for good.

Private bankers are paying attention.

The wealthy have always been attracted to Florida’s sun, sand, and nonexistent state income tax. But the state seemed to lack the cultural cachet that many entrepreneurs demanded.

Since Art Basel’s Miami offshoot arrived in 2002, much has changed. Miami’s Wynwood neighborhood has emerged as a bustling art and fashion district, and the city has opened new museums and a performing arts complex. Billionaire President Donald Trump invites world leaders to his winter retreat in Palm Beach, about a 90-minute drive up the coast from Miami.

Today, Florida is home to the U.S.’s wealthiest ZIP code (33109), nine of the world’s 500 richest people, and a growing share of the world’s wealth management business. It’s among the most popular places for multimillionaires to have second homes, along with New York and the Hamptons. It’s not yet Switzerland, but bankers say this informal capital of Latin America is among the fastest-growing recipients of offshore capital in the world.

“Florida has gone from a retirement community to a vibrant, international, exciting place to be,” says Steve Wagner, who co-founded Omnia Family Wealth after leaving Merrill Lynch’s private bank three years ago. “It’s become a destination for families of significant wealth to own property.”

Recently, some of the growth has come from a series of Latin American tax-amnesty laws that surfaced capital previously residing in the shadows. Government data show some $200 billion emerged from programs in Argentina, Brazil, Chile, Colombia, and Mexico. Before the amnesty, many compliance-conscious bankers never would have touched those funds.

In addition, a steady drumbeat of economic and political crises in the region—including in Brazil, Latin America’s largest economy—have persuaded some entrepreneurs to park their savings offshore.

Unlike Switzerland, Miami shares a time zone and a climate with Latin America and has dozens of direct daily flights to the region’s capital cities. An estimated 65 percent of the residents of Miami-Dade County speak Spanish at home. Walk into many private-banking offices here, and you’re as likely to be treated to a Brazilian cafezinho or a Cuban sweet coffee as an espresso.

At São Paulo-based Itaú Unibanco Holding SA, Latin America’s largest lender by market value, clients now keep about 30 percent of their capital abroad in the dollar and other hard currencies, up from close to nothing a decade ago, says Carlos Constantini, head of international private banking.

His clients’ offshore assets have swelled to $23 billion, from only $3.4 billion 10 years ago. About $13 billion is in Miami, the fastest-growing office, he says. Miami, he says, “provides a very competitive and a very convenient market for Latin American clients.” —Jonathan Levin

In the U.S., Wealth Seeks to Go Private

TOTAL POPULATION

329 MILLION

HIGH-NET-WORTH INDIVIDUALS

13.7 MILLION (4.2%)

Joan Solotar is armed with more than stocks and bonds.

In leading Blackstone Group LP’s private-wealth business, she’s courting millionaires with an array of investments that are far more difficult for the average investor to access—buyouts, direct lending, real estate, and hedge funds. But she’s also tapping into something that all of the largest wealth managers are waking up to: a demand for wagers in private markets.

“This is not a fad,” Solotar says. “If you’re saving for your children’s college education or your own retirement, those are not investments that you need to access on a daily basis. You’re thinking out 10 years, 20 years, 30 years.”

Blackstone, best known for its roots in private equity investing, has said that more than half of its assets could come from individuals in the next five years. The company has been courting those with $1 million to $5 million to invest. While Solotar is working to bring her company’s menu to the merely very well-off—even looking to tap into the market for 401(k) retirement funds—the largest banks are continuing to move upstream.

Soaring equity markets since the depths of the financial crisis have made many Americans much wealthier, widening the gap between the richest and the poorest. Even after the rapid growth in riches in Asia over the past decade, the U.S. still has 41 percent of the world’s millionaires and four times as many individuals with fortunes greater than $50 million as China, according to a Credit Suisse report.

Those are the customers the biggest wealth managers covet. Goldman Sachs Group Inc.’s minimum account for ultrahigh-net-worth clients is $10 million, with Morgan Stanley setting its minimum at $20 million of investable assets. Still, for Goldman, the typical client has about $50 million with its private wealth division. Morgan Stanley declined to disclose its average account size. UBS told shareholders on Oct. 25 that it aims to amass $70 billion in net new funds over the next three years from American clients with fortunes of more than $100 million.

These banks, along with JPMorgan Chase and others, are all racing to provide specialized investments for their clients. These include buyout funds, infrastructure, real estate, and even equity in Uber Technologies Inc., Palantir Technologies Inc., and other closely held startups.

Tucker York, who runs the $460 billion private-wealth business at Goldman Sachs, says the field is becoming much more crowded. “When I started in the business, it was one of the main attractions of having an account with Goldman Sachs: the ability to invest side-by-side with partners’ capital in some of the private equity things we’re doing,” he says. These days, he says, “there are far more options and choice around that.”

Of more than 300 family offices that UBS surveyed this year, half said they were considering more private equity bets. Many are also gearing up for acquisitions. The value of deals done by family offices jumped to $100.6 billion in 2016, from $25.1 billion five years earlier, according to the most recent data available from PitchBook Data Inc., which also cited an uptick in venture capital wagers.

Banks have been building teams to help billionaires pursue takeovers, sometimes sidestepping private equity funds entirely. Credit Suisse, which has more than 20 bankers dedicated to such an effort, has a $3 billion portfolio of loans that back stakes in private companies. UBS and JPMorgan Chase have begun new efforts to court family offices across the U.S. to help clients scout fresh targets.

Baby boomers have amassed enough assets to create what may become the largest intergenerational wealth transfer in the country’s history. Innovative investment offers aside, that prospect is keeping relationship managers busy with some of the less glamorous aspects of the business: tax structuring, insurance, and estate planning.

The U.S. accounts for more than a third of the $8 trillion in assets held globally by ultrahigh-net-worth individuals, those with $20 million to invest, according to Boston Consulting. UBS reckons there are probably even more rich individuals in the U.S. than surveys suggest. “A tendency to keep businesses private for longer before listing on public markets means that wealth creation is underreported,” according to the Swiss bank’s billionaires report, released in October. —Sonali Basak

In Asia, China Keeps Bankers Busy

CHINA’S TOTAL POPULATION

1.39 BILLION

HIGH-NET-WORTH INDIVIDUALS

1.14 MILLION (LESS THAN 0.1%)

Business has never been better for Jessie Leung, a recruiter in Hong Kong for a number of private banks in Asia. “The demand for talent is huge,” says the 34-year-old, who starts answering emails at 6 a.m. and is still on client calls after 10 p.m. Her billings have increased “exponentially,” she says. “Every bank is growing.”

Assets held by rich Asians doubled over the past decade, to $21.6 trillion, according to Capgemini, making the region the largest market for wealth managers. Last year almost 2,000 new millionaires were minted each day in the region. But China, the source of much of this wealth, is just beginning to open its giant domestic market to foreign companies.

There are emerging risks as well. U.S. tariffs slapped on billions of dollars of Chinese exports threaten to hit the entrepreneurs behind the country’s economic ascent and have already helped send the local stock market into a tailspin. Jack Ma, whose rise from English teacher to China’s wealthiest man helped make rich capitalists acceptable in the communist country, predicted that tariffs may be just the beginning of a trade war that could last 20 years.

Hong Kong and Singapore have reaped a wealth-management bonanza as offshore hubs catering to China’s burgeoning class of millionaires and billionaires. In July, Switzerland’s Julius Baer Group moved from one Singapore office to another, which, at 100,000 square feet, is 40 percent larger. In Hong Kong, Bank of Singapore doubled the size of its waterfront office.

Some companies are offering pay increases of 30 percent or more in Hong Kong and Singapore to poach from rivals, according to private bankers and recruiters. Leung says pay increases of as much as 40 percent aren’t unusual, and she’s seen increases of as much as 60 percent.

Offshore banking is still dominant, but the landscape is changing. On Asian Private Banker’s list of the 20 largest institutions, six are from Asia these days. But international private-banking giants still dominate, helped by their ability to manage the ever-increasing costs of legal compliance, technology, and recruiting. “You have to be at scale to be able to operate in this region,” says Tjun Tang, a senior partner at Boston Consulting in Hong Kong. “The bigger players are growing faster than the smaller players.”

Two of the biggest, Switzerland’s UBS and Credit Suisse, are aiming for the next big thing: China’s massive pool of onshore wealth. Estimated at $20 trillion, compared with only $930 billion held offshore, it’s now mostly managed by domestic banks.

They’re betting that having a foot in the door early will give them a head start on rivals. So Credit Suisse is courting rich Chinese entrepreneurs. UBS currently has more than 140 wealth-management staff in China and is still hiring.

Yet the push isn’t without risks. Banks including UBS and Julius Baer temporarily restricted staff travel to China in October after a Singapore-based UBS employee’s departure from Beijing was delayed by authorities, according to people familiar with the internal discussions at the banks.

“China’s onshore market is a holy grail,” says Kenny Lam, group president of Noah Holdings Ltd., China’s first private-asset manager for the ultrarich. “Capturing it is difficult.” —Alfred Liu and Chanyaporn Chanjaroen

Pendleton covers wealth at Bloomberg in New York. Baumgaertel is a senior editor in Munich. Förster covers banks in Zurich. Alexander covers finance in Toronto. Narayanan covers finance in Dubai. Levin covers finance in Miami. Basak covers finance in New York. Liu covers finance in Hong Kong. Chanjaroen covers finance in Singapore.

To contact the editor responsible for this story: Stryker McGuire at smcguire12@bloomberg.net

©2018 Bloomberg L.P.

With assistance from Editorial Board