The $15 Billion Arconic Buyout That Wasn't

The $15 Billion Arconic Buyout That Wasn't

(Bloomberg Opinion) -- Arconic Inc. would have made for one of the biggest private equity buyouts of recent times. Don’t cry over the deal’s demise, though.

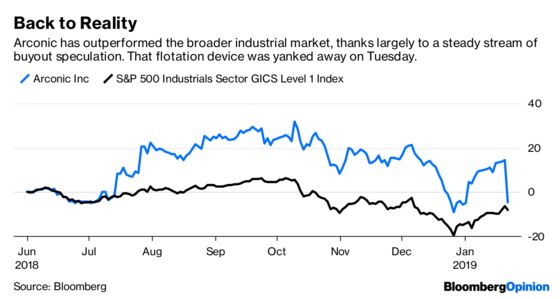

The maker of metal parts for airplanes and cars announced on Tuesday that it had decided against a sale of the company, putting an end to a tumultuous, months-long bidding process. Reuters reports that Arconic rejected a $22.20 offer from Apollo Global Management. That would have implied a valuation of more than $15 billion including debt and ranked among the top 10 largest North American buyouts in the post-recession era. But as I noted last week, the increasing contortions by both Apollo and Arconic’s largest shareholder Elliott Management Corp. to make a deal work suggested one probably shouldn’t happen at all.

Among the complicating factors were volatility in the high-yield debt market and belabored negotiations over the fate of a cladding business implicated in London’s Grenfell Tower fire in 2017. To get around the first, Apollo was seemingly biding its time and waiting for a window to obtain the financing it needed to complete a takeover. With credit markets thawing recently, it likely could have pulled that off one way or another (Reuters reports Apollo’s offer was fully financed). But you have to question the wisdom of loading up Arconic with enough debt to merit a credit downgrade to the single B level at a time when economic concerns are mounting among industrial companies. On Tuesday, Stanley Black & Decker Inc. plunged more than 15 percent after forecasting a modest slowdown in revenue growth for 2019 and an earnings-per-share gain that was weaker than analysts had anticipated.

To that end, I was struck by the fact that Arconic’s chairman John Plant said the company chose to remain independent because it didn’t feel the takeover proposals it had received were in the “best interests of Arconic’s shareholders and other stakeholders” –emphasis my own. Clearly, shareholders would have preferred a deal; the stock slumped about 20 percent after Arconic said it would no longer pursue a sale. But it’s not difficult to make the case that employees, suppliers and customers could be worse off if Arconic were to attempt to shoulder a mountain of extra interest expense in addition to the rising costs, tariffs and currency swings that are already pinching companies’ profitability. That burden could become more untenable if a global recession were to undermine the strong air-travel demand that’s fueled Boeing Co. and Airbus SE’s record backlog and, by extension, Arconic’s growth.

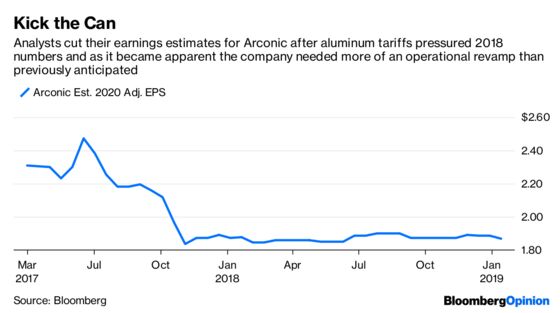

This rebuff is all the more interesting given Elliott’s involvement at Arconic. The activist investor successfully pushed for the ouster of Arconic CEO Klaus Kleinfeld in 2017 and overhauled the board, eventually adding one of its own portfolio managers. Elliott was reportedly willing to roll its equity stake into an Apollo-led buyout and buy a majority interest in a spinoff of the cladding business as a means of helping to mitigate the potential liabilities from the Grenfell fire for the buyout firm. These maneuvers struck me as a bit desperate, particularly coming from a firm that had based its campaign at Arconic around the idea that it had better ideas than management for how to run the company and could guide it to a stock price between $33 and $46 a share.

Now, as the distracting sale process comes to an end, Elliott will get its shot to prove that.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.