(Bloomberg Opinion) -- Tesla Inc.’s third quarters have become a wildcard for the stock’s many bulls and (especially) bears. Wednesday evening’s surprise profit sent the stock soaring, in a virtual replay of what happened this time last year. The big question is whether history will keep repeating or if Tesla can finally achieve the sustained profits and self-funding it has claimed to be on the cusp of for a while.

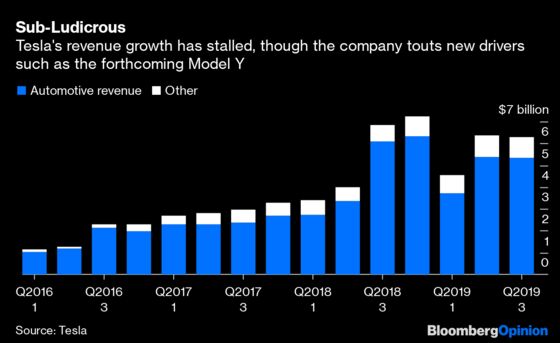

This matters for two reasons. First, investors added more than $9 billion to Tesla’s value on the back of a net profit of $143 million and free cash flow of $371 million. Second, revenue was actually down on both a sequential and year-over-year basis. When all of Tesla’s value is essentially in its multiple — that is, the promise of stratospheric growth — and growth has gone negative, then it’s fair to say the pivot to earnings had best be (a) ongoing and (b) better than a hundred million or so a quarter.

Tesla says it has been focusing on cost-control in preparation for the next phase of growth, with expansion in China and an expected 2020 launch of the Model Y featuring prominently in Wednesday’s announcement. This is catnip for bulls, looking past the evident slowdown in sales to another growth story and suggesting the company has finally gotten its arms around its biggest challenge: selling cars for more than it costs to make them.

But we aren’t there yet. On the growth front, it’s worth noting Tesla implicitly cut its guidance for the year; it is now “highly confident” of delivering more than 360,000 vehicles this year versus an old range of 360,000 to 400,000.

The profit and free cash flow figures also require scrutiny. Despite a slight drop in revenue, Tesla’s pre-tax profit swung up by almost $550 million from the second quarter. Of that, $126 million, or almost a quarter, was due to a positive swing in “other income,” including foreign-exchange gains. Another $117 million reflected restructuring charges going to zero. Tesla’s spending on SG&A also fell to its lowest share of revenue since the final quarter of 2018, the last time it reported a GAAP net profit. At less than $600 million, it was also the lowest in absolute terms since the second quarter of 2017, when Tesla sold less than a quarter the number of vehicles. By far the biggest swing, worth $317 million, was the improvement in gross profit margin.

To be clear, cutting costs is positive and necessary. The question is whether this can be sustained, given we’ve been here before, only to be quickly disappointed.

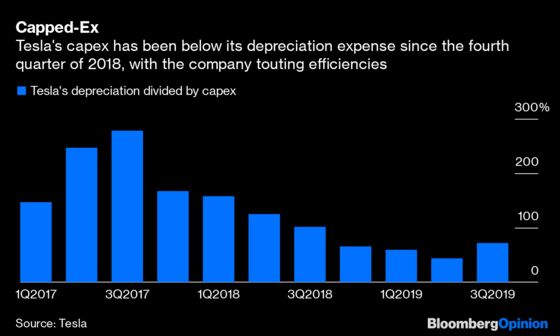

Tesla’s free cash flow, meanwhile, was positive for the second quarter in a row, at $371 million. Again, that is positive. Again, the number was flattered by Tesla underspending on its capex budget. Guidance for the year was $1.5 billion to $2 billion. Based on the low spending in the first half, the mid-point of Tesla’s range implied it spending an average of $610 million in the third and fourth quarters. Capex came in $225 million below that level, equivalent to 61% of the free cash flow. Tesla’s capex continues to come in lower than its depreciation expense, which is striking for a company with such expansive ambitions. The company puts this down to rising efficiency.

There is something ludicrous about the stock of a company already priced at $46 billion, or 422 times the 2020 GAAP earnings forecast, surging because it reported a small net profit rather than a small net loss (the consensus estimate was a negative $234 million). Ditto for a few hundred million of free cash flow largely explained by below-guidance capex. Tesla’s own forecast points to positive profits and free cash flow continuing, but which may suffer “temporary exceptions, particularly around the launch and ramp of new products.” Meanwhile, the company’s belief that it “has grown to the point of being self-funding” echoes previous statements.

As was true this time last year, a good quarter is welcome. But justifying the hopes already embedded in Tesla’s valuation remains very much a work in progress.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.