Tesla Remains a Sell at UBS After Target More Than Doubled

Tesla Target More Than Doubled at UBS. It’s Still a Sell

(Bloomberg) -- Even after more than doubling his Tesla Inc. price target, UBS Group AG analyst Patrick Hummel still recommends that investors sell the electric-car maker.

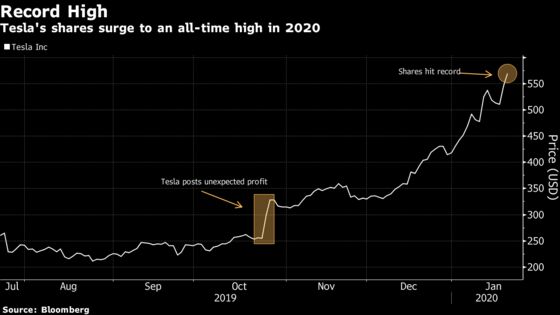

With the shares worth more than twice as much as they were at the beginning of October, UBS’s increased target of $410 is still 28% below the last closing price of $569.56.

While Tesla has the potential to become the most profitable original equipment manufacturer (OEM), the positives are “taken for granted” at the current price, according to Hummel, who sees the company’s volumes doubling by 2022.

Having the biggest long-term opportunity in autonomous vehicles, Tesla justifies a market value “well above” most incumbent OEMs, Hummel wrote in a note to restart coverage of the stock. Still, risks in execution and U.S. demand following the phase-out of electric vehicle tax credits seem to get ignored, he said.

The shares have surged of late amid a surprise third-quarter profit and strong deliveries for the fourth quarter, while the company’s market capitalization topped $100 billion on Wednesday.

Just this week, Tesla’s biggest bull predicted that the stock could reach a level as high as $960 by early 2021. The stock has nine buy ratings, 11 holds and 17 sells, with an average price target of about $370, according to Bloomberg consensus estimates.

The shares fell 1.2% in U.S. pre-market trading, also weighed down by a downgrade to neutral from outperform at Exane BNP Paribas. Tesla is due to report quarterly earnings next Wednesday.

To contact the reporters on this story: Kit Rees in London at krees1@bloomberg.net;Beth Mellor in London at bmellor@bloomberg.net

To contact the editors responsible for this story: Celeste Perri at cperri@bloomberg.net, Paul Jarvis

©2020 Bloomberg L.P.