Hearing Without Listening to the Sound of Tesla

The electric-car maker sends conflicting signals that should raise doubts about its lofty stock price.

(Bloomberg Opinion) -- Six months ago, Tesla Inc. was in the middle of its “funding secured” debacle, CEO Elon Musk was linking his lack of sleep to the company avoiding bankruptcy (in a tweet to Arianna Huffington, by the way), and the stock was trading just north of $300. Fast forward to today, and Tesla has just lost its general counsel after only two months on the job, Musk’s Twitter habit remains problematic, and the stock is trading just north of $300.

The dissonance is strong with this one. Whether Dane Butswinkas’s abrupt departure from the general counsel job had anything to do with Musk’s latest tweets about production targets or not, it should give some pause when you consider it was only in early December that the high-powered lawyer, a 30-year veteran at Williams & Connolly, was saying this:

… Tesla presents a unique and inspiring opportunity. Tesla’s mission is bigger than Tesla – one that is critical to the future of our planet. It’s hard to identify a mission more timely, more essential, or more worth fighting for.

Butswinkas’s abrupt exit isn’t the first we’ve seen at Tesla, of course. Dave Morton, who became chief accounting officer the day before Musk’s “funding secured” tweet, lasted less than a month after the public attention and pace at Tesla exceeded his expectations. Meanwhile, chief financial officer Deepak Ahuja has served multi-year stints at Tesla but announced his retirement with the equivalent of a by-the-way at the end of the most recent earnings call. Meanwhile, my colleague Dana Hull has reported on numerous other departures at the company over the past couple of years, and one of Tesla’s largest shareholders roughly halved its position in the fourth quarter.

Possibly, all the turnover and tweets just numb the senses. But the dissonance in Tesla’s numbers, on full display in the 10-K filing that dropped on Tuesday, is hard to ignore.

Tesla’s losses came to almost $1 billion in 2018. This would have been closer to $1.4 billion without the sale of $419 million of regulatory credits (see this for an explanation on these). In the second half of the year, Tesla did actually record a net profit of $451 million; although, by my estimates, sales of regulatory credits accounted for about 58 percent of that. To be clear, there’s nothing wrong with this: Tesla makes products that qualify for credits and so is entitled to sell them for a gain.

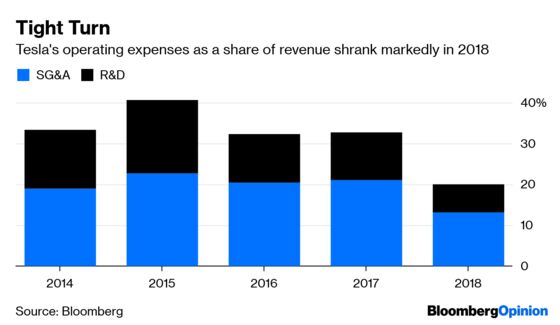

Once you strip out those gains, it means Tesla’s adjusted net loss shrank from $2.3 billion in 2017 to $1.4 billion in 2018. Which is still a big improvement. But it also reflects a step change in Tesla’s cost structure. The company’s operating expenses (excluding restructuring charges) of $4.3 billion were only 11 percent higher than in 2017 despite revenue almost doubling.

You would expect economies of scale to kick in to some degree as revenue jumps, so the direction isn’t an issue. Where the dissonance creeps in is the scale of that change when set against the fact that, as a stock, Tesla is still very much a growth story. It trades at more than 200 times the consensus forecast for GAAP earnings, and revenue is forecast to grow at 25 percent a year, compounded, through 2021, according to figures compiled by Bloomberg. That sort of growth requires spending.

Yet, as I wrote here, besides keeping a tight lid on expenses, Tesla slashed its capex budget in 2018 from an original target of $3.4 billion to just $2.1 billion – almost exactly in line with cash flow from operations. Tesla has also announced two large rounds of job cuts within the past 12 months. Remarkably, despite the big jump in revenue and tight spending, several of Tesla’s liquidity ratios actually deteriorated further in 2018.

The debate about Tesla is characterized by extremes, with ardent fans hailing it as untouchable and committed critics panning it as untenable. The latter have clearly weighed on Musk at times; so much so that Tesla inserted a bizarre risk factor into the latest 10-K filing, warning that critics could harm perception of the brand and the stock price. Musk’s own Twitter itch handing critics ammunition that very same evening is about as Tesla as it gets.

But once you’ve stripped away all the emotion, there’s a simple question: Is Tesla growing quickly and sustainably enough to justify its sky-high valuation? Put another way, do the clashing signals around spending, turnover in the ranks, weak governance, and the balance sheet deserve any sort of risk premium as opposed to today’s apparent absence of one? As I write this, the stock still trades just north of $300. I guess it all depends on what you choose to hear.

Sales of regulatory credits amounted to $283.7 million in the second half of 2018. These can be treated as pure margin. Tesla's effective tax rate in the second half was about 7.7 percent. Adjusting for that, the impact on the bottom line from the credits would $262 million, or 58 percent of Tesla's net income for the period.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.