Tesla Suddenly Makes Sense (Sort Of)

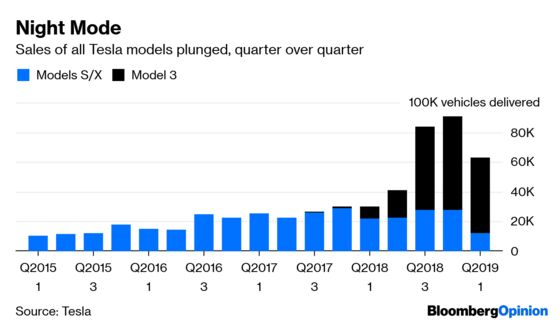

Tesla announced it sold about 91,000 vehicles in the fourth quarter of 2018, more than double the level of the second quarter.

(Bloomberg Opinion) -- Here’s a phrase you haven’t heard much about Tesla Inc. lately: It all makes sense now.

By “it,” I mean these events since Jan. 1:

- Tesla announced it sold about 91,000 vehicles in the fourth quarter of 2018, more than double the level of the second quarter. That included more than 63,000 Model 3s.

- The company said capital expenditure in 2019 would be about $2.5 billion, up slightly from last year but kept in check relative to growth expectations.

- Tesla issued guidance of 360,000 to 400,000 vehicle deliveries in 2019. Within hours, CEO Elon Musk raised that (verbally) to 350,000 to 500,000 Model 3s alone. Then he tweeted some stuff, walked it back within hours, and the Securities and Exchange Commission got involved.

- Tesla cut vehicle prices. Then it cut them again. Then again (though not as much as announced at first; see below).

- Tesla cut jobs. Then it said it would cut more jobs (though maybe not as many as it first thought; see below).

- The company lauded the benefits of its retail stores in its 10-K filing. About a week later, physical stores were deemed so-last-week compared to an online-only strategy. Then, almost two weeks after that, a swath of those doomed physical stores was pardoned (hence, some adjustments on the jobs and pricing fronts).

- Tesla surprised by launching a $35,000 version of the Model 3. Tesla surprised by teasing a Model-3 like Model Y (taking $2,500 “pre-order” payments now; deliveries scheduled to start Fall 2020).

- The company settled a maturing $920 million convertible bond with cash.

The key turning these particular tumblers into place came in the form of Tesla’s first-quarter production and delivery figures. These dropped Wednesday after the market closed — way after the market closed. Like, it would have been after the close even if the market had somehow decamped to Anchorage. This was the longest wait for a set of quarterly sales numbers from Tesla in three years:

And, to be fair, these were the sort of sales figures that could use some exquisite timing and low lighting:

Model 3 sales were up year-over-year, of course, given deliveries had barely gotten going in early 2018. But they were down by a fifth from the prior quarter. Even if one were to assume all of the 10,600 vehicles in-transit at quarter-end were Model 3s and include them, the figure would still be lower. Meanwhile, sales of the older Models S and X plunged by more than half compared with the prior quarter and almost half from a year earlier.

This is a shocking set of numbers. The Model 3 is Tesla’s supposed growth engine; the Models S and X are the higher-priced profit-margin pools. To have both shrink at once, and by this magnitude, should shake confidence in Tesla’s growth story even among committed bulls. This is especially true considering demand for higher-priced variants of the Model 3 were clearly pulled forward into the second half of 2018 — before federal tax credits began to wane — when Tesla managed to eke out two consecutive profitable quarters. Margins will clearly have been weak in the quarter just gone, but this also raises questions about subsequent quarters.

It also goes far in explaining the events summarized above. The various moves aimed at slashing costs and boosting sales volume make sense in the context of such a drop-off. Likewise the tight rein on capex, especially with that convertible bond payment factored in. On that front, Tesla pointed out Wednesday evening that, despite the inevitable hit to profits, “We ended the quarter with sufficient cash on hand.” That’s one of those phrases meant to reassure but somehow by their very utterance don’t quite hit the mark, like: “So-and-so has the total support of the president” or “I am no longer infected.”

Tesla reaffirmed sales guidance — the official guidance, that is — of 360,000 to 400,000 vehicles this year, as a means of shoring up confidence. But this implies deliveries must average 99,000 to 112,000 in each of the other three quarters. Model 3 production must improve a great deal; it averaged 4,842 a week in the first quarter, up just 4 percent from the prior quarter and representing an annualized rate of about 252,000.

Moreover, Tesla pointed out Europe and China posed challenges around deliveries. That may have been intended to show this was a temporary thing. But coming from a firm that has experienced both production and delivery “hell” in the past year or so, it rather raises the question as to how many hellish circles must be traversed.

The stock was off about 10 percent in pre-market trading Thursday morning. Then again, that merely takes it down to its traditional $260-$270 battle-zone (see this), or 67 times the consensus forecast for adjusted earnings in 2019 (it’s more than 5,000 times on a GAAP basis, no kidding). Meanwhile, later on Thursday, a lower Manhattan court will ponder whether CEO Elon Musk should be held in contempt over his tweets. Look, I didn’t say everything about Tesla makes sense.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.