(Bloomberg Opinion) -- Only in Tesla-land could a chart like this provoke a 10 percent slump in the stock at the open:

Tesla Inc. kicked off 2019 with a sales report boasting it had delivered almost as many vehicles in 2018 — 245,240 — than in all prior years combined. Roughly 91,000 found a home in the fourth quarter, triple what was sold in the first quarter. Even so, Tesla fell short of expectations (shares were down about 6 percent as of writing this).

Such is the risk when a stock trades at 130 times forward GAAP earnings heading into an update. Rather than the numbers, though, it was the stuff further down the report that might have spooked people.

First, Tesla went out of its way to say more than three quarters of orders for the Model 3 in the latest quarter came from new customers rather than reservation holders. Ostensibly, this should be a good thing, indicating widening interest. However, it also resurfaces one of the issues raised by Tesla’s blow-out third quarter results: Demand for Model 3s has been skewed toward higher-priced, higher-margin variants.

In October’s shareholder letter, Tesla said less than 20 percent of the 455,000 Model 3 reservations it had in August 2017 had canceled since then (Tesla’s disclosure on that reservation list can be somewhat oblique). Assume 19 percent went away. Assume also that, of the roughly 85,000 Model 3s sold through the end of September 2018, half went to reservation holders. We have no information on how many reservations were added in that period, though Tesla did say the net total remained above 450,000 at the end of last March. The implication is that the roughly 15,000 Model 3s sold to reservation holders in the fourth quarter represented, at best, about 5 percent of the roster.

This suggests that the vast majority of reservation holders are either waiting overseas, where Tesla says deliveries should start next month, or (and this is probably the bigger group) are waiting for cheaper variants such as the long-promised $35,000 version. That latter group poses a potential threat to Tesla’s profit margins in the quarters ahead, especially as Model 3 production remains below previous targets. Average weekly output rose by 15 percent in the fourth quarter versus the prior one. But at just under 4,700, it remained below the 5,000-per-week milestone Tesla hit briefly in July and well below the “beyond 6,000 per week” target outlined in August. (As for that earlier 10,000-a-week objective, the less said the better.)

Compounding this was Wednesday’s other announcement, namely that Tesla is chopping $2,000 from the sticker price of all its models in the U.S. to offset some of the $3,750 drop in the federal tax credit, which kicked in on New Year’s Day.

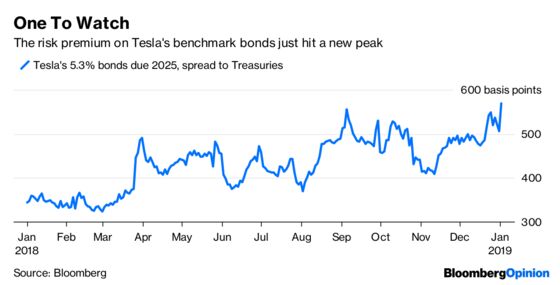

That’s Marketing 101, but it also tends to undercut the narrative of boundless demand. As the focus on higher-priced versions of the Model 3 gives way to meeting the demands of many reservation holders seeking cheaper versions, it also puts a question mark over how margins will be sustained from here. It is these, rather than sales figures, that ultimately pay the bills, including debts falling due and the capital expenditure needed to realize Tesla’s ambitious growth plans. With that in mind, this chart is worth keeping an eye on:

This assumes the net reservations figure wasn't way higher than 455,000 in October. This seems reasonable to assume since, if it was, Tesla might have highlighted that rather than simply saying cancellations since the previous August added up to less than 20 percent. Separately, even if I assumed all Model 3s sold up until September 2018 had gone to reservation holders, fourth-quarter sales to that group would still represent only about 5 percent of them, based on my math.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.