(Bloomberg Opinion) -- You’ve no doubt heard of the demand curve. But have you considered its close cousin, the desire curve? Elon Musk, CEO of Tesla Inc., shared some thoughts on this during Wednesday evening’s earnings call:

There's really two key dimensions for demand. There's live money and then there's affordability. Obviously, if somebody simply does not have enough money to have a car, it doesn't matter how much the value -- how good the value for money is. You can have infinite value for money, if somebody does not have the funds to buy the car, they simply can't get it … There's a tremendous amount of desire to buy our cars, but people, obviously, if they don't have enough money to buy them they cannot. So we have to make the cars more affordable.

Let’s agree that people without access to adequate funds cannot buy things costing more than those inadequate funds. Plus – and this is the real kick in the teeth – those same people still sometimes want those things. Musk was responding to a question about why, if Tesla suffers from supply constraints rather than constrained demand, it had cut prices. Much of his answer didn’t really address that. Words to the effect of “our product may have intrinsic value approaching infinity, but not everyone has infinite money, so we charge a market price of quite a bit less than infinity” add up to a boast about what a fabulous bargain that product is. Fair enough, but ultimately just sales patter.

Musk did hit the nail on the head with the last line: “So we have to make the cars more affordable.”

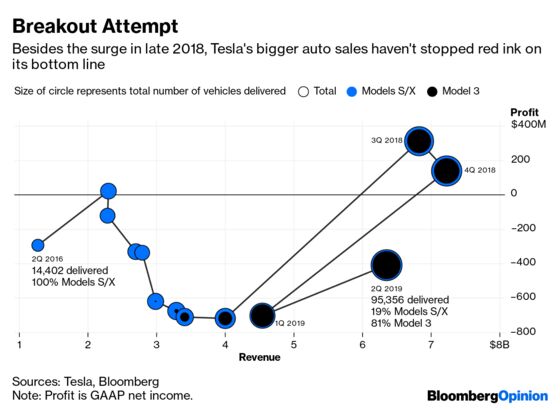

This could have been the slogan for Tesla’s second-quarter results. As I wrote here, the company delivered a record number of vehicles yet still lost more than $400 million at the bottom line. The contrast with the second half of 2018, when Tesla turned two consecutive quarterly profits for the first time ever, is jarring because Tesla sold fewer cars in each of those. The big difference is that it’s now selling more of its cheaper Model 3s and fewer premium S and X vehicles. Moreover, the Model 3s sold in late 2018 clearly skewed heavily toward higher-spec, higher-priced versions.

The chart below maps Tesla’s quarterly revenue and GAAP profits for the entire business (automotive sales constitute the vast majority of this) going back three years. You can see the growth in deliveries, the rise of the Model 3 in the mix – and how anomalous late 2018 looks:

There was clearly some positive operating leverage between the first and second quarters of this year – but then there ought to be when deliveries jump by 51%.

All signs point to Tesla having discounted in the second quarter to move inventory, especially on Model S and X vehicles. Tesla’s disclosure that Model 3s averaged about $50,000 apiece implies the premium models averaged roughly $73,000, by my math. This clearly played a role in Tesla’s loss. Extrapolating a little further, it also suggests a potential problem with top-line growth, too.

Having delivered about 158,000 vehicles in the first half, Tesla must sell another 222,000 in the second half to hit the mid-point of annual guidance (implying new records). Assume 2% of those are leased, the roughly 80/20 mix of Model 3s versus S and X holds, and average selling prices for the Model 3 stabilize around $50,000. Assume also that average pricing for the Models S and X normalizes to $85,000 (although this could also crimp demand – see above).

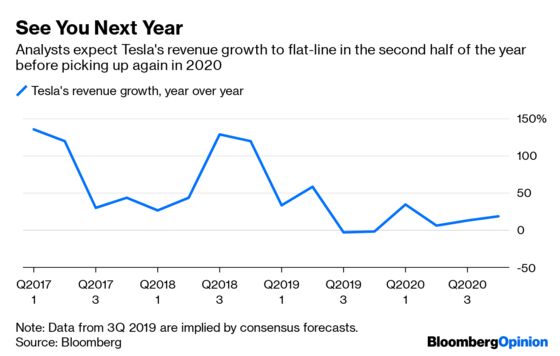

All else equal, that would imply automotive sales revenue (ex-leasing) of about $12.27 billion for the second half. That’s a hefty number, but it would represent year-over-year growth of less than 3%.

There are many caveats built in there, especially about Model S and X prices, and much could change. In particular, Tesla on Wednesday evening talked up the prospect of revenue recognition for its so-called “full self-driving” capabilities as they actually become available to use and, in theory, also become more popular. Given the technological and regulatory hurdles that need to be cleared, however, quantifying and scheduling such potential impacts is all but impossible. Musk has boasted of potentially having more than a million robo-taxis on the streets in 2020. But Tesla has also talked up its self-driving capabilities for years.

Even if that chart is just a contraption of assumptions, it fits with consensus estimates for Tesla’s overall revenue, which imply a slight drop in the second half of 2019, year over year. That would still mean 15% growth for 2019 as a whole. But when a stock trades at 190 times forward earnings – even after falling 13% Thursday morning – a flat line for six months is disconcerting:

Even as guidance for 2019 turned squishier, Musk talked up 2020, dangling the prospect that “Q3 and Q4 next year will be incredible.” Tesla’s continued underspending on its (reduced) capex budget sits at odds with the latest growth narratives of giant Chinese and European factories and new Model Ys hitting the road. As ever, though, Tesla bulls may see vast intrinsic value to all that and be willing to pay up for it. They best hope more customers adopt a similar attitude toward the cars if it is to pay off.

“Breakout Attempt” chart by Elaine He

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.