Time to Talk About Lebanese Debt Restructuring for Templeton

Templeton Says Voluntary Debt Restructuring Sensible for Lebanon

(Bloomberg) -- Lebanon should consider a voluntary debt restructuring to avert a financial crisis despite pledges of aid from Gulf benefactors, according to Franklin Templeton Investments, which manages $650 billion in assets worldwide.

A debt overhaul needs to be part of a reform program backed by lenders such as the International Monetary Fund, said Mohieddine Kronfol, the firm’s chief investment officer for global sukuk and Middle East and North Africa fixed income. Even better if that’s accompanied by a change in leadership at the Finance Ministry and the central bank, he said in an interview in Dubai.

“My biggest worry is that the runway is getting shorter,” Kronfol said. “The medium-term challenges and the need to create fiscal space through a voluntary debt restructuring or re-profiling remain, as does a multi-lateral backstop to provide credibility for an inevitable structural reform agenda.”

Read more: Templeton’s Bahrain Bet Pays Off After $10 Billion Aid Deal

Lebanon needed Qatar’s commitment to invest $500 million in its debt and a Saudi pledge to support the economy “all the way” to help its Eurobonds recover after the caretaker finance minister said he was mulling a plan to restructure debt. Top officials, including the minister himself, later denied that such a move was on the cards.

But Kronfol said it would be only “sensible” for authorities to consider a plan to buy short-dated debt and “re-issue discounted securities for longer tenors,” helping slash interest payments. The move should come as part of a comprehensive plan that addresses issues such as tackling the public-sector wage bill, overhauling the electricity sector and curbing corruption, he said.

Click here for Bloomberg’s Speaking of EM podcast on Lebanon

“When you think about the solution for the country, clearly you’re going to need some breathing room to address structural reform,” Kronfol said. “Key among this is to reduce the interest burden. So if Lebanon were to enter into some sort of an agreement with the IMF, or some multilateral institutions or a collection of countries -- that allows it to basically buy some time.”

Despite an unblemished record of bond repayment through war and political strife, Lebanon is coming to a reckoning with years of fiscal overreach. Still run by a caretaker government eight months after elections, the nation’s political discord has deepened with the crisis in neighboring Syria.

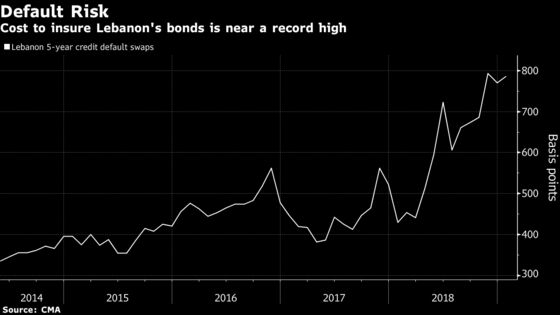

Government debt is projected to rise to near 180 percent by 2023, second only to Japan’s, according to IMF estimates. Lebanon’s debt risk, measured by credit default swaps, has risen the most in the world over the past year, apart from Zambia and Argentina, according to data compiled by Bloomberg.

Kronfol, who currently doesn’t have any Lebanese investments, said Gulf aid increases “the odds of containing the short-term stress -- to avert a crisis of confidence and stem outflows from the banking system.” It’s not enough to deal with the challenges further into the future, he said.

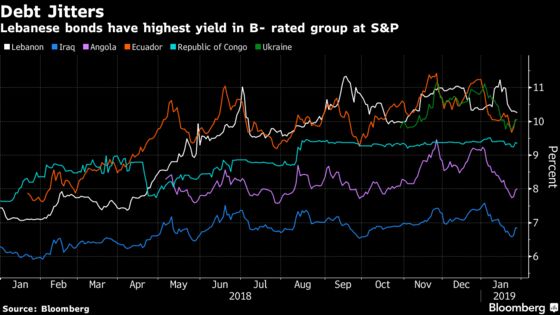

Lebanon’s dollar-denominated bonds due in 2028 are a case in point.

The securities rallied last week after the aid pledges. But the yield, at just above 10 percent, is still about 300 basis points higher than at the start of November 2017, when the surprise resignation of Prime Minister Saad al-Hariri triggered a political crisis.

Following Hariri’s brief resignation, local lenders raised interest rates to attract funds and have started to impose what Kronfol describes as “soft capital controls” to stem the outflow of deposits.

“This is not being disclosed but there are now numerous examples where people are finding it challenging to convert Lebanese pounds into dollars or to transfer dollars out of the country,” he said.

Central bank officials weren’t immediately available to comment.

In recent remarks carried by local media, Governor Riad Salameh said local banks have enough liquidity to cover demands by 80 percent of depositors to convert their money into U.S. dollars. The central bank is meeting lenders’ need for dollars, according to Salameh, a former Merrill Lynch banker who was appointed to the post in 1993.

The current predicament is one of the toughest tests facing the sectarian political system governing Lebanon since the end of the 1975-1990 civil war, which Kronfol says is unlikely to muster enough will to fight corruption and implement difficult measures required to avert a crisis.

The challenges are probably beyond what the existing political framework can address, Kronfol said. The central bank, regularly praised by investors for keeping the currency stable, is partly responsible, he said.

Still, Kronfol is careful not to call for an abrupt change that could destabilize the fragile system.

“I am not advocating things happening tomorrow,” he said. “But I am saying this should be on the cards.”

--With assistance from Marton Eder.

To contact the reporter on this story: Alaa Shahine in Dubai at asalha@bloomberg.net

To contact the editors responsible for this story: Alaa Shahine at asalha@bloomberg.net, Paul Abelsky, Alex Nicholson

©2019 Bloomberg L.P.