How Tata Can Keep Its Hold on Jaguar Land Rover

It’s time for the conglomerate’s holding company to go public. A $10 billion overseas IPO could kill many birds with one stone.

(Bloomberg Opinion) -- India’s Tata Group should treat the speed bump at Jaguar Land Rover as a timely memo: The $102 billion salt-to-software conglomerate can no longer put off listing its closely held parent.

U.K.-based Jaguar Land Rover Automotive Plc is burning cash on electric-vehicle technology just as the double whammy of a Chinese auto slowdown and Brexit threatens margins and sales. At average cash burn rates of 670 million pounds ($882 million) a quarter, the British carmaker may struggle to make it through another year, my colleague Anjani Trivedi wrote last month after it took an asset impairment charge of 3.1 billion pounds.

Had holding company Tata Sons Ltd. been a publicly traded firm, it could have raised equity relatively easily to help tide JLR over. Instead, Tata Motors Ltd., which acquired JLR in 2008, is exploring strategic options including a sale of a stake in the U.K. unit, Bloomberg News reported. Although Tata Motors says there’s “no truth to the rumors,” the bond market was a little relieved.

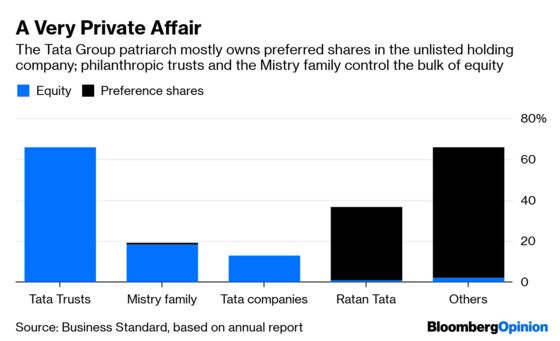

Investors’ concerns haven’t fully dissipated, and that shows the problem with the sprawling Tata Group’s structure. In the current scheme of things, the holding company and its 66-percent owners — who happen to be charitable trusts — depend on payouts from software services provider Tata Consultancy Services Ltd. as well as Jaguar Land Rover to keep the empire ticking.

The insufficiency of those dividends became a sore point in a 2016 boardroom battle between patriarch Ratan Tata and Chairman Cyrus Mistry, who was abruptly ousted after less than four years. Borrowing on the strength of operating companies’ cash flows has a limit. Next year will see a record $17.5 billion of debt mature, according to bonds and loans data compiled by Bloomberg. The conglomerate must step up investment in order to generate more free cash.

Last year’s $5 billion purchase of bankrupt Bhushan Steel Ltd., which supplies metal to auto and appliance makers, is a step in that direction. The move helps group boss Natarajan Chandrasekaran cut Tata Steel Ltd.’s reliance on a less-than-rewarding construction industry.

Still, it’s Jaguar Land Rover that should worry him. JLR has avoided investing in entry-level crossovers — which account for a quarter of sales at rivals BMW AG and Daimler AG’s Mercedes-Benz — because of its expensive focus on electric vehicles, as Deepesh Rathore, analyst at Emerging Markets Automotive Advisors, said in a Bloomberg Television interview.

Demand isn’t collapsing. Global auto sales have been growing very slowly for two years at least. Short-term volatility aside, that may not change unless income growth is disrupted, says Jonathan Wilmot, global strategist at Aletheia Capital. Even so, with potential buyers waiting for electric cars to mature, the opportunity to list JLR has been lost for the moment.

When I suggested a Jaguar Land Rover IPO in Hong Kong or London, Chandra, as he’s known, had just been named Tata Sons’ chairman. Two years on, however, it may be better to float the parent. In his recent book, Mukund Rajan, who formerly oversaw brands across the group, estimates the value of the Tata Sons assets owned by the philanthropic trusts at $80 billion to $90 billion. If the trustees sold $10 billion to the public, the offer would almost equal India’s three biggest IPOs combined. The market wouldn’t be able to digest it.

But Hong Kong could. The Securities and Exchange Board of India might have to tweak its rules and allow Tata Sons to go overseas. The trusts could then plow the proceeds back into Tata Sons as 20-year redeemable preference shares, which is what they used to do before they prematurely liquidated them over disagreements with ex-chairman Mistry’s dividend policy.

Preferred shares would give the charities assured dividends to carry on with their social mission; Tata Sons would get liquidity to pay down debt, especially at Jaguar Land Rover; the marquee British automaker would get time to shore up its product portfolio; and the Tata Group would have a stronger hold over the (tarnished) jewel in its crown. Meanwhile, a bitter legal battle with the Mistry family, which can’t freely sell its 18 percent stake, might end if Tata Sons bought back the shares at fair market value. And Hong Kong would snag its biggest IPO since insurer AIA Group Ltd.’s 2010 float.

It’s time Chandra put an IPO plan into top gear.

Citigroup Inc. did chalk out a plan to list Tata Sons a few years ago, but it went nowhere.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.