Take-Two Climbs as Conservative Views Good Enough for Street

Take-Two Analysts Say Conservative Forecast Good Enough for Now

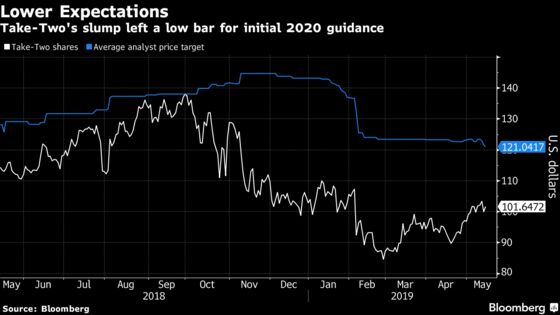

(Bloomberg) -- Take-Two Interactive Software Inc. analysts found silver linings in a weaker-than-expected forecast that caused shares to be volatile after the company’s earnings report.

The video-game maker sees fiscal 2020 adjusted earnings per share of $3.75 to $4 versus the average estimate of $4.84, according to data compiled by Bloomberg. The top end of that range “cleared investors’ recently falling hurdles,” according to Morgan Stanley, and many analysts noted that the company is typically conservative with its initial outlook for the year. Analysts still see significant growth opportunities from Red Dead Online.

Shares of Take-Two rose as much as 4.4% on Tuesday in New York, briefly touching their highest level in three months. Peer Electronic Arts Inc. gained as much as 1.8% and Activision Blizzard Inc. added as much as 1.7%.

Here’s what Wall Street is saying:

Jefferies, Timothy O’Shea

“Full-year guidance is soft as feared, but will probably be viewed as enough by investors,” partly due to Take-Two’s history of being conservative.

A primary reason to own the stock is recurrent consumer spending, which rose 20% in fiscal 2019. Take-Two looks best positioned for microtransaction growth among video-game stocks.

Slowdown in Red Dead Redemption unit sales could underscore the bear thesis that the game has lost momentum and the online version could struggle, but Jefferies sees reason to be optimistic given Rockstar’s success with GTA Online.

Rates buy, price target of $135 is close to the highest on the Street

Piper Jaffray, Michael Olson

The initial fiscal 2020 forecast was below analyst estimates “as expected (and typical)” but NBA 2K, GTA, Red Dead and Borderlands are expected to be primary contributors.

Piper expects Red Dead Redemption monetization to pick up in the coming year, and notes that Take-Two’s management indicated that Red Dead Online beta is ahead of where GTA Online beta was at this point in its development. Even so, some investors may wait to see how Red Dead Online does in the June quarter before growing confident that the franchise will be a multiyear revenue contributor.

Rates overweight, price target $114 from $119

Morgan Stanley, Brian Nowak

The top end of Take-Two’s earnings forecast for fiscal 2020 cleared a recently lowered bar, and the company historically is pragmatic with its guidance. As such, “the decks are clear” for the coming year and Morgan Stanley sees “multiple levers of growth,” including the Red Dead Online launch, Borderlands, NBA 2K strength and streaming distribution.

“Execution from here is key,” as it is with all video-game stocks. With poor investor sentiment around Red Dead Online, there’s an opportunity to “meaningfully improve the narrative” with positive results and the bar isn’t high.

Rates overweight, price target $120

Baird, Colin Sebastian

Take-Two’s forecast “looks prudently conservative” in light of the continued GTA slowdown as well as higher research and development spending and lower margins as it looks to refill its pipeline.

Maintains outperform rating, price target trimmed to $109 from $114

What Bloomberg Intelligence Says

“Expectations for Borderlands 3 and recurrent consumer spending appear prudent, yet beatable. While Take-Two didn’t include a possible PC release of Red Dead Redemption 2, this remains a likely future release, even with uncertain timing.”

--Matthew Kanterman, technology analyst

Click here for the research

To contact the reporter on this story: Catherine Larkin in Chicago at clarkin4@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Steven Fromm, Scott Schnipper

©2019 Bloomberg L.P.