Sycamore Gets $1 Billion In Deal That Amazed Street

Sycamore Pockets $1 Billion From Deal That Amazed Wall Street

(Bloomberg) -- Stefan Kaluzny has made a ton of money -- and drawn his share of critics -- buying down-on-the-heels retailers using lots of debt.

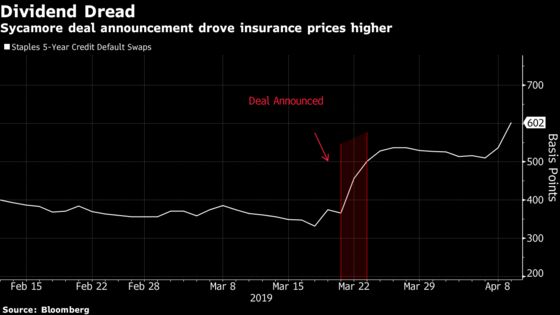

Now, Kaluzny’s Sycamore Partners is under scrutiny again, after completing a deal that left even seasoned leveraged-buyout experts agog. On Tuesday, Sycamore pulled off a $5.4 billion refinancing of Staples Inc., which it bought in 2017, that funded a staggering $1 billion dividend to the private equity firm.

The dividend is among the biggest in recent memory, even in a world where buyout firms routinely extract large sums for themselves after taking companies private. Combined with a payment it took in January, it means Sycamore has recovered -- in less than two years -- roughly 80 percent of the equity it originally put up as part of the deal. Private equity investors typically run their companies for five to seven years before taking profits and exiting the investment.

“Sycamore has constantly raised lenders’ eyebrows with their actions at Staples,” said John McClain, a portfolio manager at Diamond Hill Capital Management who bought some of the company’s buyout debt but declined to participate in the new offering. “This seems to be another credit agreement written on a cocktail napkin.”

A representative for Sycamore, which manages around $10 billion in assets, and Kaluzny, who co-founded the firm with Peter Morrow, declined to comment.

Aggressive Tactics

Little-known outside Wall Street, Kaluzny has focused his 8-year-old firm largely on the retail and consumer sectors, buying troubled companies with debt and betting that he can revive them with cost-cutting and new strategies. Successes included once-beaten-down chains such as Talbots and Zales. But Sycamore’s aggressive tactics have at times led to litigation and claims from creditors of hastening or exacerbating losses.

That kind of financial engineering had seemed to be the playbook after Sycamore bought Staples at a valuation of $6.9 billion, its biggest takeover ever. Sycamore contributed $1.6 billion of equity and raised $4 billion of debt for the company’s more promising wholesale division, which sells office supplies to large corporations, according to people familiar with the matter. At the same time it spun off the U.S. and Canadian retail operations into separate entities.

Sycamore took $300 million of that equity back in January as part of a complex deal to acquire Essendant Inc., another office supplies distributor, and then soon started pitching the dividend recapitalization that would pay them another $1 billion.

But that proposal, missing typical investor protections, so alarmed some creditors that, on the day investors were told about the deal, the cost to insure Staples debt against default for five years saw its biggest increase since 2012, according to data provider CMA.

“These terms give the issuer far more flexibility than a dividend deal usually merits,” said Scott Josefsberg, co-head of high yield at the credit research firm Covenant Review.

A team of banks led by Goldman Sachs Group Inc. and UBS Group AG persuaded investors to buy the debt anyway -- but Staples had to pay up. It will make annual coupon payments of almost 11 percent to buyers of the unsecured bonds, while the senior debt yields around 8 percent.

Altogether, the company now faces an additional $130 million annually in interest payments, according to people familiar with the matter. Sycamore told investors it boosted Staples earnings by $160 million since taking over the company, the people said.

Representatives for Goldman Sachs and UBS declined to comment.

Tweaking the Deal

The company also agreed to reduce the size of an unsecured debt tranche in favor of more secured debt and to close loopholes that could disadvantage creditors. Even after that, Sycamore had to go a step further to get the debt allocated: It agreed to buy $180 million of the unsecured notes, and hold them until at least September. Its varied accommodations notwithstanding, the debt traded down as soon as it hit the secondary market and credit default swaps spiked even more.

Private equity firms have been using dividend recapitalizations for years to book profits and take skin out of the game after they acquire companies. Sometimes they pay a portion of the dividend with free cash, but more often they do it by loading up the acquired company with debt.

The payments rarely exceed $1 billion, according to available market data. That’s partly due to investor skittishness at the concept of funding a cash payout with debt rather than revenue. One recent example occurred in 2017, when Tilman Fertitta issued debt as part of a recapitalization of Landry’s Inc. and Golden Nugget Inc. -- and took a $1.6 billion dividend to pay for his acquisition of the Houston Rockets.

Track Record

The retail industry in particular is filled with companies going bankrupt after being acquired in debt-heavy buyouts by private equity firms. One notable example was Toys ’R’ Us, which shuttered in 2018 when it couldn’t make interest payments, despite steady revenue.

Adding to investor concerns about the Staples deal was Sycamore’s track record. In the last few years, two of the firm’s portfolio companies have filed for Chapter 11 protection.

After Sycamore bought a stake in Aeropostale Inc. in 2013, the retailer accused Sycamore of driving Aeropostale into bankruptcy to facilitate an inexpensive takeover. Sycamore denied those claims and a judge ultimately dismissed them. Sycamore went on to bid on Aeropostale in bankruptcy, walking away in the face of a better price.

Investors again criticized Sycamore last year involving apparel company Nine West Holdings Inc., which filed for bankruptcy four years after Sycamore bought its parent. A group of creditors said the acquisition “left the surviving company deeply insolvent.” The group dropped its claims in February in return for a $120 million payment from Sycamore.

None of that, of course, ultimately deterred debt investors in the Staples deal, showing just how eager Wall Street is for double-digit yields.

“Bond investors are clearly thirsty and willing to swallow virtually all flavors of risk,” said Christian Hoffmann, a portfolio manager at Thornburg Investment Management in Santa Fe, New Mexico.

--With assistance from Sridhar Natarajan.

To contact the reporters on this story: Eliza Ronalds-Hannon in New York at eronaldshann@bloomberg.net;Davide Scigliuzzo in New York at dscigliuzzo2@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, ;David Gillen at dgillen3@bloomberg.net, Larry Reibstein

©2020 Bloomberg L.P.