Swap Your Month-End Plans for Tequila and Avocados: Taking Stock

Swap Your Month-End Plans for Tequila and Avocados: Taking Stock

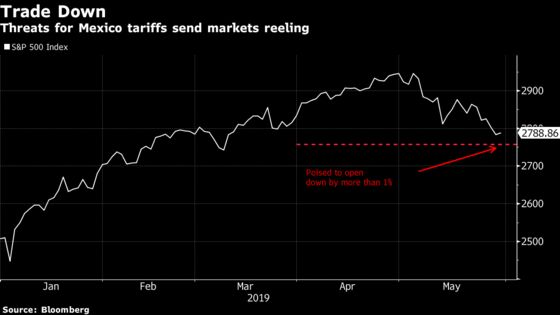

(Bloomberg) -- It’s month-end, a Friday, and the President is on the (trade) war path. This, as we’re poised to see the worst May since 2012. Godspeed.

Thursday had provided some consolation to the terrible performance we’d seen over the month (before brand new developments on the trade war -- more on that below) as the tape felt like it really wanted to stay positive -- a small sign at least that investors are finding bargains in some corners of the market. Strategists for their part had come out assuaging some concerns about how far to the downside we’ve come, trotting out figures not from current S&P 500 levels that were deemed “fair value.”

Fundstrat’s Tom Lee saw the potential of a “pessimism peak,” while Nomura strategists led by Masanari Takada wrote that the commodity trading advisors, or CTAs as they are known, are “all but done closing out their long positions,” a sign that some of the worst may be over, as the strategists saw no signs of panic selling among fundamental traders.

But some, like Canaccord’s Tony Dwyer, MKM’s Michael Darda and Stifel’s Barry Bannister write that the fear and downside for the market won’t be over until the Fed cuts rates -- or as Dwyer put it, corrects their “policy mistake.” Darda brought up what seemed to be a rhetorical question: how do policymakers achieve the greatest interest rate reduction before the next election? The answer, they found, was fiscal retardant policy (trade war) combined with that ’mistake’ made in December.

Those conclusions aren’t far from what this column has alluded to over the past few weeks -- mainly that Trump may have found a way for the FOMC to do his bidding after all and cut rates -- just ratchet up economic fears through trade threats (one day ahead of when Chinese tariffs on $60 billion worth of U.S. goods go into effect in retaliation).

And as the Trump administration announced even more tariffs overnight (5% on Mexico within the next two weeks, and up to 25% by Oct. 1) the first part of the equation is being pounded pretty hard. What’s sure to be frustrating for policymakers is that these new tariffs were in no way related to the actual trade relationship, in fact, officials just this week had made overtures to the fact that the so-called new NAFTA was to be signed shortly. Instead, the justification for tariffs was illegal migration.

The Fed’s preferred inflation gauge data is due out later this morning, and you can bet it will be closely watched for any figures that allow the FOMC to have "cover” should they want to lower rates in any upcoming meetings. It will be the only data point for some time that may help provide that impetus, as throughout this long drawn-out trade drama in May, we’ve been starved for new data points (outside some guidance revisions in tech related to Huawei and retailers citing a macroeconomic overhang) to indicate how the trade war is actually impacting the economy. It’s one thing for the yield curve to tell us a recession is coming, or for stocks to selloff hard -- it’s another when the economy tells us it is actually right to worry.

Rare Find

Looking through some of the winners and losers of what is sure to be one of the more memorable May months in recent history, it’s a bit of sweet serendipity that amid the bloodbath in equities, there were a few stocks that rose. Some would even call those names that rose this month, “rare.” My colleague Carolina Wilson explains:

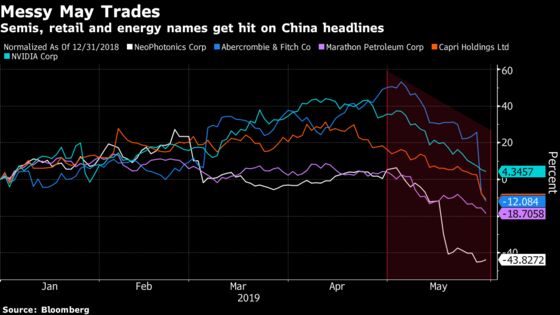

With all eleven sectors poised to be red for the month -- and one more trading day left in May -- let’s take a quick look at how China trade drama made its way into some of the worst and best stock picks. Semis felt the heat from Trump’s move to blacklist Huawei (which was compounded overnight as China announced it was setting up an “unreliable entity” list of companies that hurt or cut supplies to domestic firms) , triggering a sell-off in some key chip suppliers. The usual suspects like Nvidia and Qualcomm are both among the top 10 worst-performers for the S&P 500, both down more than 18% in May and getting worse this morning. But smaller players -- like NeoPhotonics -- were even more burnt, plunging about 47% as the company counts close to half its revenue from Huawei last quarter, according to Bloomberg supply-chain data.

Specialty retail and department stores have also felt some pain, with the likes of Capri and Foot Locker sinking. Abercrombie & Fitch has been in China’s cross hairs, after plunging by the most in almost two decades after disappointing quarterly sales. The CEO said the company is reducing the amount of merchandise it gets from China. And while Canada Goose is also in the red on missing estimates, China seems to be a tailwind for that luxury parka maker, as the CEO says expanding into the region will be a key source of growth.

The latest blow in the trade disputes adds to a month that has trimmed 12% from the 24-member S&P Supercomposite Automobiles and Components Index, shaving about $20 billion in market value in May through Thursday. It was on track to be the worst month for the sector since December’s 14% slump, although Friday’s declines could push the group beyond that.

And last, energy’s crude awakening. WTI is down more more than 11% this month, on pace for its worst monthly retreat since November, with all but one of the 29 members in the S&P Energy Index in the red for May. Marathon Petroleum Corp., Halliburton Co. and Apache Corp. are all leading losses there, with some basic metals miners also tanking as growth prospects in the world economy dim. A rare bright spot? Rare Earth metals. The group has grabbed headlines amid mounting speculation China, which accounts for 71% of global supply, will restrict shipments to the U.S. Those plans were incrementally firmed overnight as reports indicated Beijing now has a plan to restrict exports of rare earths should the trade war deepen. That could push prices higher and benefit producers, with the likes of Neo Performance Materials already getting a lift.

On Tap for Next Week

A ton of Fed speakers are on the docket next week, which is great timing for color on whether they see a tightening of financial conditions related to a trade war on multiple fronts. 13 speakers are planned, together with the Beige Book, which should provide some of the freshest contextual information on the economy’s inner workings. Who knows if they’ll need furious rewrites after the inflation data this morning and as the U.S. picks a fight with one of its largest trading partners, but the language will be telling.

Non-farm payrolls are due at week-end, which, given that it’s data for May, could provide at least some insight into whether employers froze their hiring plans at all in the face of concerning trade-related headlines.

On the company-specific front, Tiffany (with heavy Asian exposure) will report, together with Salesforce.com, while conferences pick up steam. REITweek begins, the massive healthcare conference ASCO is in full swing (Jefferies is also running its healthcare conference), BofAML will host its technology conference and UBS puts on its global industrials and transportation conference (with the likes of BA, GM and MMM).

Sectors in Focus

- Huawei-exposed companies (IPHI, NPTN, LITE, MU) as China readies a “unreliable entity” list. Details are scant but at first blush it appears to be aimed at companies that may have abided by the U.S. blacklisting of Huawei. That list will also include organizations and people, according to China National Radio

- Retailers will see volatility after Gap’s results are cratering their stock, Big Lots results are pushing shares up 12% pre-market (coming off its 6th straight down day, recording losses of 18% over the span), Williams-Sonoma shares soared on theirs

- U.S.- traded companies with operations exposed to Mexico and the possible tariffs. At first glance automotive firms appear to be taking the largest hit, though may make sense to watch CVGW, VNE, GM, F, CMG, ADNT, DAN, DLPH and STZ

- E&Ps as WTI crude continues its downdraft as trade worries continue; similarly, base metals with exposure to copper, like FCX may be under pressure on the worsening economic outlook

- Recent volatile IPO names (LYFT, SWAV, TW, AVTR) after Uber’s first results came in relatively solid. There’s a dearth of analyst commentary as the quiet period for the ride sharing company has yet to conclude (that happens next week). Lyft is higher, though other volatile names appear to be hurt as the market sells off on trade worries

Notes From the Sell Side

Kraft Heinz has had a rough 2019 – shares are down more than 40% from a February peak, and it closed at a record low on Thursday, in what was its sixth straight decline – but Piper Jaffray is seeing opportunity in the weakness. The firm upgraded Kraft to neutral, writing that while “many risks remain” for the food company, they now appeared priced into the current valuation. Analyst Michael Lavery is “cautious on the outlook for KHC and its ability to build or maintain brand equity in a way that can drive sustainable organic growth.” He added that while putting in a new CEO was the right move, “he needs incremental brand spending to rejuvenate KHC’s dusty brands,” which could prompt earnings estimates to fall.

CF Industries Holdings was put on a 90-day negative catalyst watch at Citi, which cited concerns about weak volumes. “Delayed corn planting has farmers just trying to get seed in the ground, likely delaying fertilizer applications,” the firm wrote, affirming its buy rating but trimming the price target by $2 to $48. Analyst P.J. Juvekar sees this as a temporary issue, writing that the price of corn “has sent a signal” with recent gains, which “bodes well for fall application acres next year.”

BofAML has a positive view on the semiconductor sector over the coming 12 months, expecting a trade deal between the U.S. and China in the second half of the year. Removing that overhang and uncertainty would not only benefit the group with a demand upturn, it wrote, “but also an inventory build in the supply chain.” BofA expects volatility to remain elevated until a deal is reached, though it recommends buying on weakness. Among specific names, it lifted STMicroelectronics NV to buy and cut Dialog Semiconductor PLC to underperform. “STM has lower customer concentration risks vs Dialog and has stronger exposure to the fast growing auto and industrial semi markets,” it wrote, adding that “content growth at Apple is likely to help STM overcome fluctuations in iPhone units better than Dialogue can.”

Tick-By-Tick Guide to Today’s Actionable Events

- CI investor day

- FDA Public Hearing to discuss potential regulation for cannabis products.

- ASCO kicks off

- 8:30am -- April Personal Income, Personal Spending

- 8:30am -- April PCE Deflator

- 9:45am -- May MNI Chicago PMI

- 1:16pm -- Tiger Woods, Bryson DeChambeau and Justin Rose tee off at the Memorial Tournament

--With assistance from Carolina Wilson and Ryan Vlastelica.

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.