Subprime Auto Bond Market Is Unmoved by Record Late Loan Payments

Subprime Auto Bond Market Is Unmoved by Record Late Loan Payments

(Bloomberg) -- While more Americans than ever are behind on car payments, investors in bonds backed by auto loans haven’t flinched.

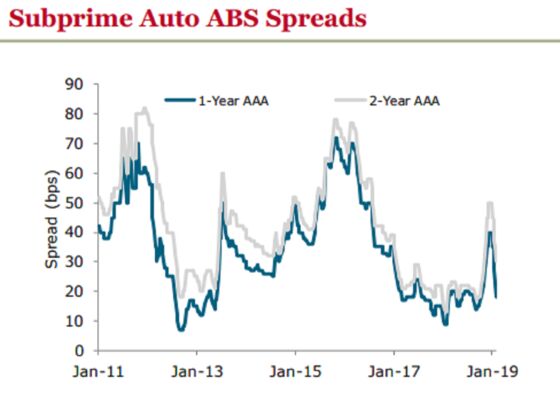

Prices of risky auto bonds have risen even as car loans that haven’t been paid in at least three months exceeded 7 million at the end of last year, the highest since the New York Federal Reserve began tracking the data two decades ago. As demand surged, the extra yield investors get to hold the highest-rated debt instead of what’s seen as a risk-free rate has shrunk over the past month.

The tighter bond spreads are a sign investors remain confident credit protections will continue to prevent losses in the subprime auto asset-backed securities market, as well as the fact that the rising late payments haven’t yet turned into a big increase in defaults.

Securitized debt makes up just a fraction of the overall auto credit market, while the majority is kept on finance companies’ balance sheets. Only about 10 percent of the $437 billion of low-rated car loans have been turned into ABS, according to Wells Fargo.

“ABS investors still feel pretty good on credit,” said Amy Sze, an analyst at JPMorgan Chase & Co. “Recent subprime auto new issues have priced well. Vintage loss data for 2018 is running just a touch under 2017, so it’s within expectations.”

The 60-day-plus delinquency rate for loans underlying subprime auto bonds has been steadily rising since 2011 -- and is currently higher than its peak in 2009 -- but those missed payments haven’t translated into heavy losses for investors. The default rate edged higher to 5.5 percent percent in 2018 from 5.2 percent a year earlier, according to S&P.

“The deterioration appears to be largely due to late payments trending higher on some deep-subprime issuers’ 2015-2017 securitizations,” S&P said in its latest monthly auto ABS report. However, performance of the bonds for deals issued between 2015 and 2018 “has been fairly stable,” the analysts said.

Despite the stability, observers are still wary of some trends in the market. Over the last three years, companies that offer loans to the riskiest borrowers tend to be the ones who use securitization the most. And at the same time, strong demand for higher yields has led to more lower-rated bonds in deals.

That’s a concern because there are fewer protections baked into the lower end of subprime ABS. So as a result, investors are starting to demand more robust credit protections than compared with a few years ago, eating away at already-thin profit margins at lenders struggling with deteriorating loan quality.

--With assistance from Gabrielle Coppola.

To contact the reporter on this story: Adam Tempkin in New York at atempkin2@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Randall Jensen, Brendan Walsh

©2019 Bloomberg L.P.