Corporate Earnings Shouldn’t Worry Markets Just Yet

Corporate Earnings Shouldn’t Worry Markets Just Yet

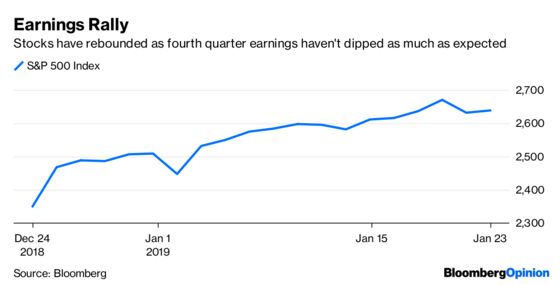

(Bloomberg Opinion) -- Fourth-quarter earnings haven’t been the bad news deluge that many expected. The question is whether the weather will hold out another quarter or more.

Of the companies that have reported results for the last three months of 2018, just over 70 percent have beaten expectations. While that’s actually on the low side — executives and analysts consistently lowball estimates, making them easier to top — market reaction to earnings surprises has been more ebullient than in recent quarters, which suggests genuine bar-beating. According to Bank of America, shares of companies that posted better-than-expected earnings have outperformed the market by nearly 2 percentage points in the following 24 hours. Oddly, even companies that reported worse-than-expected results have outperformed the rest of the market, though only slightly.

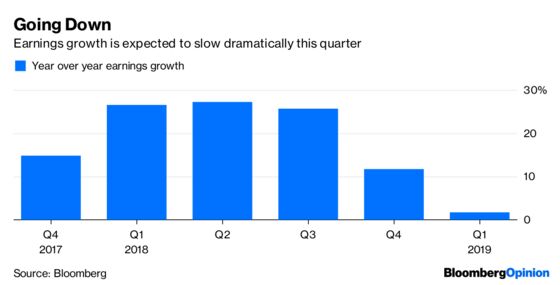

Overall, fourth-quarter earnings are expected to have risen almost 12 percent on average, a sunny performance by any measure. But that hasn’t stopped many people thinking that the next quarter will bring a squall. For the first quarter, analysts are predicting earnings will rise just 1.7 percent. And the horizon has been getting darker. Three weeks ago, the prediction was for a 4.3 percent gain. Interestingly, this growing gloom hasn’t spilled into analysts’ profit projections for the full year. They expect 2019 earnings to rise by a still strong pace of nearly 7 percent. That implies an expectation, perhaps unrealistic as some have pointed out, that the income of the companies in the S&P 500 will leap an average of nearly 11.5 percent in the last three months of this year.

How to explain this seeming disparity? Turns out, the cut in first-quarter earnings projections largely reflects sharply lowered expectations about one area of the economy, energy, following the recent tumble in oil prices. Just three weeks ago, earnings in the sector were predicted to rise by nearly 20 percent this quarter. Now, they’re forecast to fall 5 percent. Expectations for the profits of industrial companies, on the other hand, have held steady, with analysts projecting an increase for the group of about 5.5 percent in the first three months of the year. All of consumer discretionary is supposed to drop slightly, but again, that is mostly because of one sector, autos. Retailing profits are still expected to be up 12 percent.

Investors will eventually get caught without an umbrella in an upcoming earnings season. And if there is a vane pointing to bad weather ahead, it’s this: Revenue is expected to rise about twice as much as earnings this quarter, reflecting the belief that costs, like wages and possibly tariffs, will finally start catching up to Corporate America and bring about the erosion in profit margins that many have predicted for some time. But the downpour of disappointment is likely still more than a quarter away.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.