Stock ‘Bargains’ Hiding in Sight of the Highs: Taking Stock

Stock ‘Bargains’ Hiding in Sight of the Highs: Taking Stock

(Bloomberg) -- About those horses everyone owns.

The sure-to-be fateful comment earlier this week from Tesla CEO Musk that anyone who owns a car other than a Tesla in three years "will be like owning a horse," was tested in the span of 72 hours.

Though I’m not sure he meant a mustang. Ford shares soared post-market Thursday (currently up 8 percent in the pre-market), rising to levels not seen since August after beating analyst estimates for both earnings and revenue -- this, after a strategy shift in recent months that involved focusing more heavily on SUVs. Compare that with Tesla’s results just one day prior, which some analysts called a “debacle” as shares fell 5 percent, testing levels not seen since early 2017. Reports late Thursday that Citron Research’s Andrew Left was no longer "long" Tesla, throw in some investor demand for the ride-sharing service Uber’s IPO, and we have quite the imbroglio in the consumer transport segment. Uber just set its price range for the offering and Bloomberg reports estimate the valuation above the prior funding round, and that which is double the value of the electric carmaker.

The Future

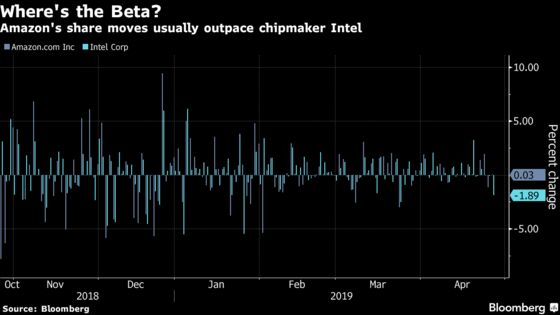

Two key companies that are seeking to shape the future of tech, communication and Cloud tech, reported widely varying outcomes last night, as Intel whiffed after a surprise cut in its forecast, while Amazon.com reported record high margins (though with record low e-commerce revenue growth).

What surprised the most in their respective reports was the volatility. Amazon almost always has something up its sleeve during earnings, usually remaining mum ahead of the report. Intel, on the other hand, is rather accessible and we’ve seen a variety of developments recently, including its exit from the 5G development after the Apple/Qualcomm settlement. China concerns were cited as a main weakness for the chipmaker, which also happened to have disappointed on its forecast in the prior quarter, when it cited difficulty in its main growth driver, the data center business. Intel shares are lower by nearly 8%, while Amazon’s shares are effectively unchanged (a rarity with its avg historical change around earnings at ~7% when compared to Intel’s 3.5%). The chip space is getting hit hard, with NVDA, MU, WDC all lower.

Crowded Room

The brief concern that existed early in Thursday’s session as industrials 3M Co. and UPS soured an otherwise celebratory tech mood (competitor FDX just got downgraded at UBS on likely persistent headwinds for margins) fell by the wayside as the S&P maintained a foothold around the 2,930 region for much of the afternoon. Given that there wasn’t an immediate selloff when we hit the all-time highs Tuesday, it pays to take a look at where some of the money has gone, and where it has not.

Just eight companies in the S&P 500 are in the "oversold" territory (as measured by the relative strength index below 30) as of midday Wednesday, as the market hovers near all time highs. And interestingly, there’s no sector rhyme or reason (such as, for example, the healthcare debacle we observed last week). 3M Co., as mentioned above, is one of those 8, and was nearing overbought territory just one day ago! Quite the about face. Walgreens Boots, Regeneron Pharmaceuticals, Newmont Goldcorp Corp. (how many corporations is it?), Iron Mountain, Newell Brands, Incyte and Waters Corp. round out the grouping, which mostly suffered amid poor quarterly results.

Of the above, Walgreens, Regeneron, Newell Brands and Incyte have yet to report. The last two also happen to involve heavy hedge fund ownership, with 12% of Newell Brands held, and Incyte near 7% (though Baker Bros Advisors, technically an investment advisor, owns 16% of shares outstanding) according to data compiled by Bloomberg. These could be names to watch ahead of their results.

And on the flip side, there are some "crowded" names, according to UBS in a note dated Tuesday, that have yet to report and warrant being on your radar. These names may show elevated activity during this earnings season and include Alphabet, Alibaba, Mastercard, Adobe and Salesforce.com. An "underowned" name, for what it’s worth, Exxon Mobil, is due to report shortly. These were categorized, according to the analysts, based on the dollar value holdings by active managers when compared to the equity index benchmark. Adobe just reported last month, but the others aren’t too far away, like Alphabet and Mastercard next week.

On Tap for Next Week

Also due next week is Central Bank decision time. It’s hard to call anything a "snoozer" these days, given that central banks are pretty much the only thing markets look to for direction at this point, but with fed fund futures estimating a whopping 2.6% change of a cut (no hikes are on the table through early 2020), it will be all about the language and growth signals learned since the dovish tilt seen at the March 20 meeting. A variety of Fed members will be on hand at a the Hoover Policy Institute conference at the end of the week.

Earnings season doesn’t slow down, and if GM is anything like Ford was last night, we’re in for a ride early in the week. Auto sales will come shortly thereafter with fresh data on April. The health of the smartphone (and consumers’ discretionary income broadly) will also be on display with Apple and Samsung’s results as well. There’s also a category of earnings due next week that I’m deeming the "ifys" -- Spotify and Shopify -- which have each developed a sort of cult following (new tech trends in music and a platform with a touch of marijuana).

Lastly, on the macro front, trade talks with U.S. and China representatives ratchet back up, with reports indicating that the goals are for a conclusion of a deal some time in early May. Who knows, maybe that could mean May 3, to coincide with nonfarm payrolls data that is always a spectacle.

Sectors in Focus Today

- Cybersecurity names after Proofpoint shares shrugged off some forecasts that missed estimates. Analysts are broadly positive on the name, citing “solid execution” and management’s “bullish commentary” on the demand environment. Shares had fallen nearly 10% post-market before paring some of the losses. Shares are still indicated to open a touch lower

- Ride-sharing names and recent IPOS (LYFT, ZM, PINS) after Uber priced its IPO above its prior funding round valuation

- Animal health names (FRPT, ZTS, KIN, IDXX, PETS) after Elanco entered agreement to acquire Aratana Therapeutics at a near 40% premium to last close

- Semiconductor names as Intel cut its forecast (watch components of the SOXX; NVDA, AMD, MU, WDC), and some suppliers, like FORM, SNPS, VSM, AMAT

- Homebuilders after the weakness seen in DR Horton and Tri Pointe results Thursday

Notes From the Sell Side

A day after UPS reported first-quarter results that missed expectations, UBS downgraded peer package shipper FedEx to sell, writing that the results “provided evidence of the mixed macro backdrop including soft total revenue growth." Beyond that, analyst Thomas Wadewitz cited concerns about FedEx’s Ground and Express divisions, saying challenges in them “may last longer than expected.” The margins pressure at Ground, along with a “lack of momentum” for Express in Europe, are both “headwinds that are likely to persist.” He added that 2020 earnings expectations were too high, and that “muted free cash flow and long term concerns about Amazon are likely to continue weighing on FDX’s valuation."

In another example of one company’s results resulting in a downgrade for another, Western Digital was cut twice at Baird – to underperform from outperform – which pointed to “continued deterioration in NAND flash fundamentals,” a diagnosis it reached in part because of Intel’s print last night. The deterioration in NAND memory chips is "characterized by an expected continuation of double digit price declines this quarter and very high inventories," analyst Tristan Gerra wrote, adding that this was “amplified by a weak macro environment," and that "a second-half seasonal improvement in NAND does not mean a cycle bottom."

On the upside, Goldman Sachs lifted its view on Medicines Co. to buy from neutral. The firm also more than doubled its price target, lifting it from $23 to $55, a level that implies upside of about 85% from the company’s Thursday close. "With the ORION Phase 3 topline results expected in 3Q19, our comfort level with inclisiran’s benefit/risk profile has increased," analyst Paul Choi wrote, adding that a successful launch for inclisiran "should also increase MDCO’s potential appeal to partner(s) or strategic buyer(s)."

Tick-By-Tick to Today’s Actionable Events

- 7:30am -- ABBV earnings

- 8:00am -- FCX earnings

- 8:30am -- CMCSA, UPS, DHI earnings call; Fed holds first public meeting on BB&T/SunTrust deal in Charlotte

- 8:30am -- March Prelim. Durable Goods Orders

- 8:30am -- Weekly Initial Jobless Claims, Continuing Claims

- 8:30am -- March Prelim. Cap Goods Orders

- 9:00am -- ABBV, MO earnings call

- 9:15am -- F earnings

- 9:45am -- Weekly Bloomberg Consumer Comfort

- 10:00am -- FCX earnings call

- 10:30am -- BMY earnings call

- 11:00am -- April Kansas City Fed Mfg Activity

- 12:30pm -- LUV earnings call

- 4:01pm -- AMZN earnings

- 4:05pm -- INTC, MAT, SBUX earnings

- 5:00pm -- AEM CN earnings; INTC, MAT, SBUX earnings call

- 5:30pm -- F, AMZN earnings call

--With assistance from Ryan Vlastelica.

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.