Stitch Fix Plunges After Growth Story Endangered by Forecast Cut

Stitch Fix Plunges After Growth Story Endangered by Forecast Cut

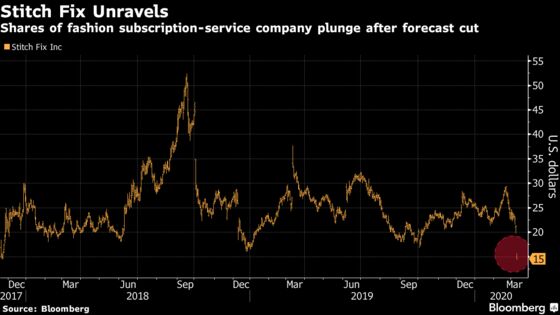

(Bloomberg) -- Stitch Fix Inc. plunged to a record low after the fashion subscription company cut its revenue and Ebitda outlook for the rest of year, leading analysts to slash their 12-month price targets.

The outlook disappointed investors and analysts, with the blame being placed on a lower average order value (AOV), a slower-than-expected ramp of its business in the U.K. as a result of Brexit, an investment in talent and business segments, and a worsening macro environment. Furthermore, management said that while the coronavirus hasn’t had a “material impact” on its business just yet, “it’s reasonable to expect we’ll see some impact.” The company also offers direct buying services.

Price targets were slashed by most sell-side analysts who issued a report after the results. “A growth story with lofty valuations can expect to be punished for moderating its top-line outlook,” Telsey Advisory analyst Dana Telsey wrote. She maintained her outperform rating, but reduced her price target to $20 a share from $33. The average target for analysts now sits at about $20 compared with $31 a week ago, according to projections compiled by Bloomberg. What hasn’t changed, however, is analysts’ ratings distribution, with nine buy ratings and seven holds. No analysts recommend selling.

The shares plummeted as much as 33% to $14.28, below the record low intraday price of $14.48 in November 2017. The company went public on Nov. 16 of that year with shares priced at $15 apiece. The stock reached a record high of $52.44 in September 2018, but hasn’t traded close to that in more than a year.

Here’s more of what analysts had to say after the results:

RBC Capital Markets, Mark Mahaney

For the second-quarter report, “the shorts were right and we were wrong, and as Covid uncertainty spreads, buying a consumer discretionary name like SFIX isn’t for the faint of heart.” Even so, Mahaney said the post-market drop Monday of 39% was “excessive.”

Risk-reward now “looks highly encouraging” with the shares trading at 0.5 times calendar 2020 Enterprise Value/Sales and 10 times EV/Ebitda for 15%-20% revenue growth and “30%ish” Ebitda growth.

Stitch Fix continues to be a “good economics business,” with 12 straight quarters of at least 20% year-over-year organic revenue growth, “consistently rising mid-40s% gross margin,” the fifth consecutive year of positive Ebitda and free cash flow, and more than $300 million in cash.

Maintains outperform, price target to $24 from $38.

Needham, Rick Patel

“It’s unclear how much of the guidance cut is related to coronavirus or how much demand has been hurt” quarter to date.

Patel’s neutral view on the stock has been based on “low conviction” around the company’s initial second-half plan, which previously implied an acceleration compared with the first half of the year.

“While guidance and expectations have now come down, macro uncertainty is elevated and it remains difficult to have confidence in when or how much SFIX’s sales will accelerate.”

Stitch Fix is “controlling what’s controllable,” but visibility is low, he said. Rates hold. There is no price target on the stock.

William Blair, Ralph Schackart

“While the second-quarter results were relatively in line with expectations, the company’s steep reduction in fiscal year 2020 sales and adjusted Ebitda guidance reinforces fears around its ability to monetize clients while maintaining stable profit margins.”

With the post-market decline, the stock currently trades at 59 times Schackart’s revised 2021 Ebitda estimate. “However, we note our estimate embeds a notable snapback in margins predicated on continued marketing expense control and lapping of heavier investment spending, where we have less visibility.”

He sees potential downside to both sales and margin from any continued pressure on lower order value and customer acquisition costs inflation. Strong competitive pressures and wider impact from the coronavirus are other possible risks.

Rates market perform. The firm does not have a price target on shares.

To contact the reporter on this story: Janet Freund in New York at jfreund11@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Lisa Wolfson

©2020 Bloomberg L.P.