State of the S&P 500 Exposes Bearish Amnesiacs: Taking Stock

State of the S&P 500 Exposes Bearish Amnesiacs: Taking Stock

(Bloomberg) -- S&P futures are looking through some cautious earnings reports overnight after a series of positive data figures out of Europe (including Euro area PMIs). Memory maker Seagate and Alphabet dragged on the QQQs post-market, but avoided any major blow ups that could substantively change the narrative. Most of major tech has reported, and this week will ultimately be focused on media names (read: streaming, streaming, streaming).

Viacom, Disney and to a lesser extent cult-name Snap results (post market) will keep investors occupied today as the latter faces difficulty following a "ghoulish" 2018. The social media giant is staring at the fewest bullish analysts in its history now, with about 10% sticking with an equivalent of a buy rating. For the two other media giants, streaming will be the focus -- Disney on its rollout of a Netflix competitor-style service, and Viacom on its strategy to reduce its reliance on cable channels. Viacom just hit the tape with mixed results.

But the focus today will be on Trump (again) as reports circulate his planned speech -- aides are floating the idea that "unity" will be a main focal point. Critics say they’ll believe it when they see it.

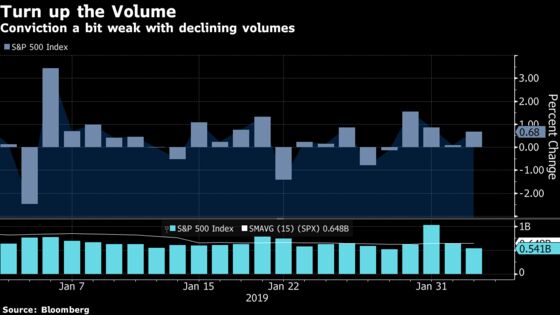

State of the Market

U.S. President Trump’s State of the Union is widely expected to touch on a variety of topics, and ignore others (see my colleague Felice Maranz’s preview here), but U.S. equities are sending their own message on the state of play, albeit conflicted in some cases.

The bears have faced a drumbeat of positive up days, led by growth and risk names in tech (Alphabet was among the biggest gainers Monday ahead of its results, though cost numbers are weighing on shares, down 2.4% pre-market).

It’s easy to forget the bearish and defensive tone that beset the market (remember when Utilities and Healthcare led at year end?) But its not just the FAANG names that are pushing upwards. Breadth was solid Monday (though volume left the bulls with something to be desired), and the selloff on the Durable Goods data was immediately bought. The S&P 500 now sits at levels seen in mid 2018 and is approaching its 200-DMA (while the Dow Jones Industrial average already blew past its respective moving average in the past week).

In addition to blowing past technical levels, allaying bearish fears of a growth slowdown in its wake, the S&P is also leaving more and more strategists’ forecasts behind. Among those tracked by Bloomberg, just one forecast a contraction in the S&P for 2019 as of Jan. 10. In just the past 3 weeks, two more forecasts have, by default, become forecasts of contraction in the main gauge. Even in Europe the idea holds, as Goldman Sachs strategists led by Sharon Bell earlier wrote that those who didn’t profit from the January rally likely missed out on most returns for the year.

For all the positive signals one can take from the recovery, there is some caution. Technicians at MKM led by JC O’Hara now see "fatigue" as a possible risk. They write that in the latest march higher from the Dec. 24 lows, it appears as though "a lot of muscle was used."

Other strategists aren’t ready to leave the cautious growth story alone. Canaccord quantitative analysts, in their February summary write that the recently cut IMF forecasts remain "too high," citing "unrealistic" U.S. forecasts given a decline in the leading economic indicator index. They have company in Credit Suisse, whose analysts expect growth trends to decelerate further in 2019.

The bottom line though is that 2019 hasn’t just been about the bottom line. A major part of the story this year is M&A. Just Monday (and over the weekend) an $8 billion dollar software developer entered a deal to be bought, Tesla became acquisitive, activist Starboard Value got involved in two separate transactions (PZZA, and the mega pharma deal BMY/CELG) and a mortgage originator was purported to be seeking a sale. And that follows nearly $187 billion worth of North American deals in January, the best start to a year since 2000, according to Bloomberg’s Nabila Ahmed and Michael Hytha.

Its hard to argue that volume of transactions would take place if there was a lack of confidence in the future outlook (though that reference year, 2000, should serve as some warning) from Private Equity firms and strategic buyers (depressed valuations notwithstanding). And to be sure, executives in earnings calls have been upbeat, according to Bloomberg Intelligence strategists, though there has been a fair amount of industry specificity (machinery and healthcare executives were among the most optimistic).

Sectors in Focus Today

- FAANGs after GOOGL finalized the group’s earnings with some concerns over rising costs (similar to Facebook’s issues, though GOOGL shares are paring some losses)

- Video game makers after Glu Mobile disappointed (EA reports post market while TTWO is due Wednesday pre-market)

- Managed care names Centene (raised its outlook), Wellcare after results and contract wins announced Monday

- Food service and hospitality names after ARMK raised its outlook and beat on the top and bottom line; following SYY’s beat of expectations Monday (watch WBT, MIDD)

- Memory names WDC, NTAP after Seagate disappointed

- Media after Viacom and MSGN report; DIS reports post market

- Optical names after Fabrinet’s results were solid (though had a large run-up) and Lumentum expected shortly

- Semiconductor and solar names after AEIS (AMAT, LRCX as top customers) reported together with Infineon and AMS in Europe issuing cautious growth outlooks

Notes From the Sell Side

Cloud player Box Inc. was rated a new buy by Goldman Sachs analysts who set their price target with assumed upside of 43% ($31). Analysts led by Ted Lin call Box called "one of the best positioned vendors in cloud content management," with attractive growth while its on track to re-accelerate its bookings in FY19 and revenue in 2020.

Equifax is indicated lower after Deutsche Bank moves the stock to hold as expectations for improving mortgage originations have prompted the stock to outperform the market year to date. Analyst Ashish Sabadra notes an economic slowdown in the U.S. could weigh on the results and the risk/reward is now balanced. Expects the credit bureau to possibly guide its first quarter results below estimates.

Tick-by-Tick Guide to Today’s Actionable Events

- XRX investor day

- SAAStr Conference

- 8:30am -- VIAB earnings call

- 9:45am -- Jan. Markit PMI

- 10:00am -- Jan. ISM Non-manufacturing index

- 4:01pm -- EA, VRTX earnings

- 4:05pm -- DIS earnings

- 4:10pm -- SNAP earnings, APC earnings

- 4:30pm -- DIS, VRTX earnings call

- 5:00pm -- EA, SNAP earnings call

- 9:00pm -- State of the Union Address

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.