(Bloomberg Opinion) -- Standard Chartered Plc is taking a knife to its bloated structure. One cheer for that, even if the cost-cutting plan doesn’t go far enough. The bigger issue now for CEO Bill Winters is where to find growth.

StanChart will cut $700 million in costs in the next three years and restructure – though not exit – low-return operations in India, Indonesia, South Korea and the United Arab Emirates, the London-based lender said after reporting 2018 earnings that missed consensus estimates. Underlying pretax profit rose 28 percent from a year earlier to $3.86 billion.

The emerging markets-focused bank remains a flabby institution. It had 85,000 staffers at the end of last year, down just 1,000 from 2017. The cost-to-income ratio rose to 69.9 percent, from 67 percent in the first half, and was only a smidgen below 70.8 percent a year earlier. Revenue per employee is well under half that of Singapore’s DBS Group Holdings Ltd.

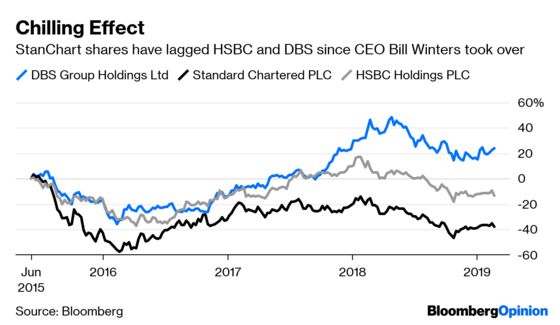

The slow pace of Winters’ turnaround has been a source of frustration for Temasek Holdings Pte, the Singapore state investment company that’s the largest investor in StanChart and DBS, the Financial Times reported last month. While the CEO has cleaned up the bad-loan morass he inherited in June 2015, a lack of growth prospects persists.

StanChart shares have dropped almost 40 percent under the former JPMorgan Chase & Co. banker’s tenure, lagging DBS and HSBC Holdings Plc. The lender’s Hong Kong-traded stock rose as much as 2.9 percent after Tuesday’s results. A higher dividend will have helped, even if a hoped-for share buyback didn’t materialize.

A successful move into digital banking has helped to buoy DBS, and that points the way forward for its Temasek stablemate. StanChart is setting up a virtual bank in Hong Kong, and has also launched two blockchain payment services with Alibaba Group Holding Ltd. affiliate Ant Financial. One serves Filipinos remitting money home from the British colony and the other is aimed at Pakistanis working in Malaysia.

StanChart suffers from a lack of scale in retail banking and is a minnow in wealth management, an area that punished even heavyweights such as UBS Group AG last year. The firm’s private banking unit reported an underlying pretax loss of $14 million in 2018, compared with a loss of $1 million the previous year. Meanwhile, StanChart’s (sensible) decision to exit stock underwriting, trading and research in 2015 means it’s not the go-to bank for Chinese small and medium-sized enterprises.

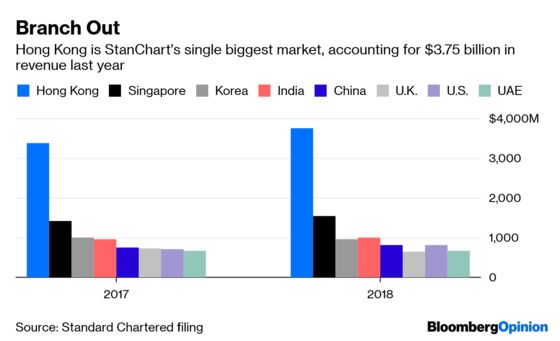

Like HSBC, StanChart remains over-focused on China and Hong Kong. Citigroup Inc., the other bank with a big Asian trade franchise, posted a 5 percent increase in revenue from the region last year and shows the value of geographic diversification: It’s in 17 Asian markets, none of which accounts for more than 14 percent of revenue. Hong Kong makes up 25 percent of operating income for StanChart and 31 percent of HSBC’s global revenue. That exposes both to the risk of an extended U.S.-China trade dispute.

StanChart’s lack of scale has seen it frequently cited as a potential takeover target. Perhaps it’s time to flip the conversation. To gain the size and balance it needs, the bank could also turn acquirer. The question is whether that’s a job Winters is equipped to handle.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.