Euro Area May Kick Joint-Debt Can Down the Road Amid Resistance

Euro Area May Kick Joint-Debt Can Down the Road Amid Resistance

(Bloomberg) -- A push by Southern European countries and France to agree on a form of debt mutualization in the euro area was met with stiff resistance by Germany and Austria, complicating efforts to reach a deal this week to cushion the economic blow of the pandemic.

“I consider the debate about euro bonds as a not so serious one, because everybody knows that you would have to change the fundamental contract of the EU,” Austrian Finance Minister Gernot Bluemel told Bloomberg TV on Monday. “We have enough measures to help each other if needed.”

His comments came as European diplomats worked on a mutually acceptable statement due to be issued following a call between the bloc’s finance ministers on Tuesday. While they’re likely to agree on the use of existing instruments, such as the euro area’s bailout fund, to help finance the recovery efforts, a group of countries led by France seeks to include the prospect of more radical measures to share the burden of the spending required to rebuild.

“This crisis will do considerable damage so we must all be able to restart at the same speed,” French Finance Minister Bruno Le Maire said on Monday on France 2 television. “Nothing would be worse for Europe than some countries being able to recover faster because they are richer,” he said, as he called for the creation of an instrument to put “put several hundreds of billions of euros into stimulating investment after the crisis.”

Such persistent demands have so far failed to sway German Finance Minister Olaf Scholz. In an op-ed for publications in Italy, Spain, France, Portugal and Greece, Scholz held the line on Germany’s stance, saying the European Stability Mechanism rescue fund “already now offers the possibility for euro countries to raise capital jointly with the same advantageous terms for all.”

Another proposal is to set up a European fund that would guarantee European Investment Bank loans to small business, he said. Post-crisis reconstruction will be a matter for the European Union’s seven-year budget, Scholz said, effectively dismissing the French proposal for a separate instrument.

Solidarity Appeal

The comments add to signs that an appeal for more European solidarity by Spanish Prime Minister Pedro Sanchez, who took his case to Germany over the weekend and found some encouragement at the top of the European Central Bank, are likely to fall on deaf ears.

Sanchez, in a piece published in Germany’s Frankfurter Allgemeine Zeitung on Sunday, urged the EU to show “rigorous solidarity” in the fight against the coronavirus outbreak with a new Marshall Plan of public spending to drive the economic recovery. He said the program should be funded by jointly issued debt.

That has been a red line for Germany, but its representative on the ECB Executive Board, Isabel Schnabel, told Greek newspaper To Vima it’s clear that countries worst hit by the virus will need financial support from the EU level and that so-called coronabonds would be one possibility. ECB President Christine Lagarde has been one of the most strident advocates of joint debt issuance as the EU tries to mitigate the economic damage from the virus.

Economic Collapse

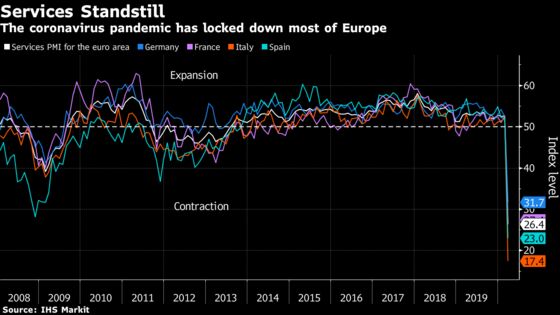

The fury of the pandemic may be starting to abate in Spain and Italy where the death toll has slowed in recent days, but European leaders have seen their economies collapse due to the severe restrictions imposed on movement. A gauge of services and manufacturing activity released Friday pointed to an annualized contraction of about 10% with worse still to come.

Over their call on Tuesday, European finance ministers are likely to agree on a framework for delivering financial support to the countries worst hit by the pandemic. EU leaders could sign off on the plan later in the week if there’s progress.

There’s broad agreement that the ESM should be mobilized to offer credit lines worth as much as 2% of euro-area GDP and ministers are approaching a deal on minimizing the conditions attached. Tapping in to the ESM’s 410 billion-euro ($440 billion) war chest could also pave the way for the ECB to buy vast amounts of sovereign bonds through its Outright Monetary Transactions program.

There’s much more dispute over how to finance the reconstruction of the European economy once the virus has passed, with Germany, Austria and the Netherlands opposing a call by countries led by France, Italy and Spain for jointly issuing coronabonds to spread the financial stress of the rebuilding.

Scholz said Germany’s proposal is for a joint emergency response that provides “enough liquidity for all European Union states so the preservation of jobs doesn’t depend on the whims of speculators.” Tapping the ESM would provide 39 billion euros ($42 billion) for Italy and 28 billion euros for Spain to shore up their economies, he said.

Behind the debate about how to deal with the virus crisis is a long-running concern about the future of Italy and how far the currency bloc should integrate its finances. The EU’s third-largest economy already had the weakest outlook and the most perilous public finances before the pandemic and is now dependent on support from the ECB to contain its borrowing costs.

©2020 Bloomberg L.P.