South Africa Banks Gather Their Defenses to Ride Out Virus Storm

South African Banks Prepare for the Worst, Hope It Doesn’t Come

South African banks have made their rainy-day provisions. Now, they must wait and see whether the funds set aside will be enough to manage a potential torrent of bad debt and ease pressure on their earnings in coming months.

The country’s so-called “Big Four” experienced a profit slump deeper than that seen during the global financial crisis in the six months ended June after a spike in credit impairment charges as they grappled with the effects of the coronavirus pandemic and a nationwide lockdown. Their return on equity fell to 9.2% from 15.4% a year earlier, according to South African Reserve Bank data.

A report by PwC, covering results at Standard Bank Group Ltd., FirstRand Ltd., Absa Group Ltd. and Nedbank Group Ltd., estimates their charges soared by a combined 130% in the first half of 2020 from a year earlier, while profits before provisions grew 4.4%.

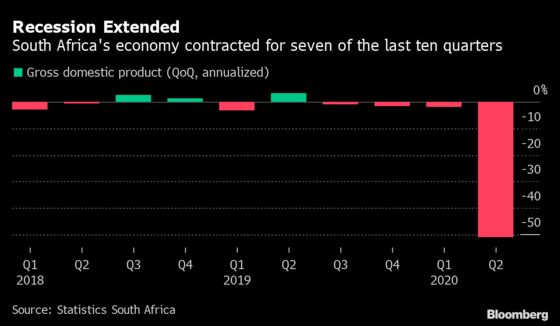

Front-loading credit impairments should help banks produce a better result in the next six months as they navigate through further fallout from Covid-19. The lenders must contend with an economy in its longest recession since 1992, leaving customers more vulnerable to joblessness. Unemployment probably surged to 35% in the second quarter, according to a Bloomberg survey of economists.

An index of South African bank stocks dropped 0.8% as of 10:20 a.m. in Johannesburg, declining for the fourth time in fifth days.

Here are the views of some investors and analysts on the outlook for the sector:

Neelash Hansjee, portfolio manager at Old Mutual Investment Group:

- Despite their raised provisions, banks “are still making a profit, they still have strong capital levels, they still have lots of liquidity.”

- “If you look at recent activity post lockdown, there is an improving trend.”

- Write-offs in private-equity investments reflect a tough economy “on the ground.”

- Profit before provisions at Absa “certainly surprised the most and showed management have been on the right path,” while Nedbank reflected a challenging period.

Nolwandle Mthombeni, analyst at Mergence Investment Managers:

- Getting return-on-equity ratios back to decent levels will be key to driving valuations in the sector. To lift ROEs, banks must make sure that the outcome in coming months is “better than the worst-case scenarios they have factored into their models.”

- “They have put provisions away for a rainy day. If the rainy day doesn’t come, then all those provisions will be released and that will make a huge difference and a huge swing in earnings.”

Jan Meintjes, portfolio manager at Denker Capital:

- The major banks have approached provisioning differently, but none of the methods are wrong. Those that front-loaded provisions more aggressively, such as Absa and FirstRand, are likely to show lower credit costs ahead.

- “The banks once again showed how well capitalized they are. All of them showed through different stress scenarios that it is highly unlikely that any of them would need to raise capital to overcome the impact of the pandemic.”

Renier de Bruyn, analyst at Sanlam Private Wealth:

- Banks have navigated the market dislocation from the virus crisis well, supported by South Africa’s central bank, with “liquidity in the system having normalized and no material counter-party default occurring in the trading operations.”

- Lenders are coming to terms with the impact of restrictions to contain the spread of the coronavirus on credit losses.

- The effect has arguably been delayed by relief programs offered by the banks. “The next six months will provide more clarity on how relief customers have recommenced payment.” This has “generally started well, while lower interest rates are also helping customers.”

- “The industry should remain profitable over 2020, while the suspension of dividends and slower loan growth should further assist in sustaining capital ratios.”

©2020 Bloomberg L.P.