Sony’s Spinoff Snub Shows Activist Investor Loeb Was Right

(Bloomberg Opinion) -- Now that they’ve snubbed activist investor Dan Loeb’s spinoff proposal, the onus is on Sony Corp.’s management to turn their imaging and sensing solutions business into something meaningful.

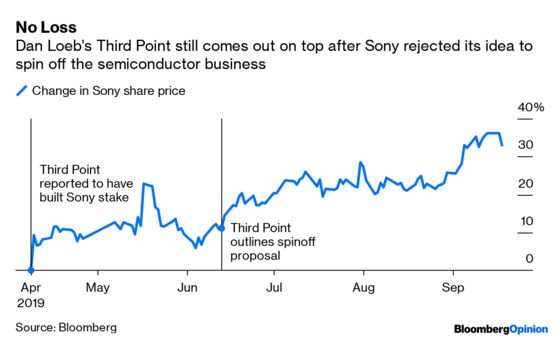

Loeb’s Third Point LLC challenged Sony in a June 13 letter to split the company in two: A new Sony focused on entertainment; and Sony Technologies, which would comprise the image sensors which are used in most of the world’s smartphones. Doing so would unlock the potential of this semiconductor business, which has been underappreciated both at Sony and among investors.

In Third Point’s view, Sony suffers from the common phenomenon of conglomerate discount. The complexity of its portfolio of businesses makes it difficult for investors to forecast and model numerous and sometimes unrelated earnings drivers. Third Point summarized the unit’s status succinctly:

“Contributing only 18% of Sony’s consolidated earnings, this division is often treated by investors as an afterthought”

As a standalone company, it argued, Sony Technologies would no longer be a buried, “uncut rough stone.’’ A spinoff would be able to attract investors with specific interest in semiconductor companies who might better appreciate its technological edge.

Sony’s response this week in a letter to shareholders essentially says, Yes, you’re right. Our sensor business is awesome and has great potential. But we’re keeping it.

Sony hasn’t been shy to dump units. In the past few years, it sold off the iconic Vaio computer business, overhauled its television division and retreated from a losing battle for market share in mobile phones. All of which have helped improve margins.

Yet management justified holding onto the sensor business by explaining that a spinoff would create “meaningful sources of dis-synergy” if it was separated from Sony. It cited the example of how technology for its CMOS image sensors, which combine photo diodes (that convert light into current) with logic circuits (that process it), came about because the team accumulated such expertise when it developed systems for the PlayStation 3 games console.

That’s a compelling argument. Except that the PS3 was released 13 years ago.

Having Sony itself as a key Sony semiconductors client might strengthen the case for working side-by-side. But, inter-segment revenue for this unit was just 1.4% last year. This suggests that the parent is not a key customer for its semiconductor unit, or that the core business isn’t adequately compensating this division for the work it provides. Either scenario only strengthens Third Point’s thesis that the division isn’t afforded the value it deserves by investors, nor by Sony itself.

This also suggests that most of the division’s customers are external and it would deal with them at arm’s length anyway.

Further making the case that the division isn’t being fully leveraged are its financials. Sony has done a good job of improving profitability at this unit, from 0.2% operating margin in fiscal 2013 to 12.5% last year. But a 12.5% operating margin for a business that has a 70% share of the smartphone image sensor market is underwhelming.

Rival Tower Semiconductor Ltd. has achieved figures as high as 16.1% and reported 11.9% operating margin last year. To be clear, image sensors are only one of Tower’s offerings, but the fact that Sony has few peers in this product segment tells you that profitability ought to be pretty high if only because clients have few other choices.

Even though Sony has decided to reject Loeb’s advice while talking up the image sensor business, Third Point won’t be losing. Sony’s stock is up 32% since Reuters reported this latest stake-building in April, and 19% from when the New York-based hedge fund published its letter on Sony.

Instead, if Sony management can’t live up to its promise to turn this technological edge into fatter profits, then even non-activist investors will punish them.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.